In my previous post Counterparty Risk: Some Way to Go for Derivatives, I concluded that uncleared OTC counterparty risk is bigger than the 80% cleared traded notional volumes might imply. Of all counterparty risk about two thirds (65%) or more is uncleared and about half (49%) or more is linear delta. A lot is riding on participants’ response to the uncleared margin rules (UMR) which start to catch the larger buy-side players as roll out completes in September 2020 and portfolios transition afterwards.

Here I look at which products contain the most uncleared risk and whether conventional clearing can solve the problem of reducing uncleared risk to make uncleared margin manageable.

Summary

- In the first few years of the UMR roll out, we see only a small shift in outstanding notional from uncleared to cleared (BIS figures).

- While some uncleared risk has been taken off.

- A surprisingly large part of the residual uncleared outstanding notional is exempt from UMR (deliverable FX derivatives) and has not budged.

- New and complementary market solutions have emerged which like clearing reduce counterparty risk without affecting market risk.

What can we learn from the BIS uncleared notional figures?

At lest two things: cleared vs uncleared trends and uncleared product breakdown.

Cleared vs Uncleared Trend

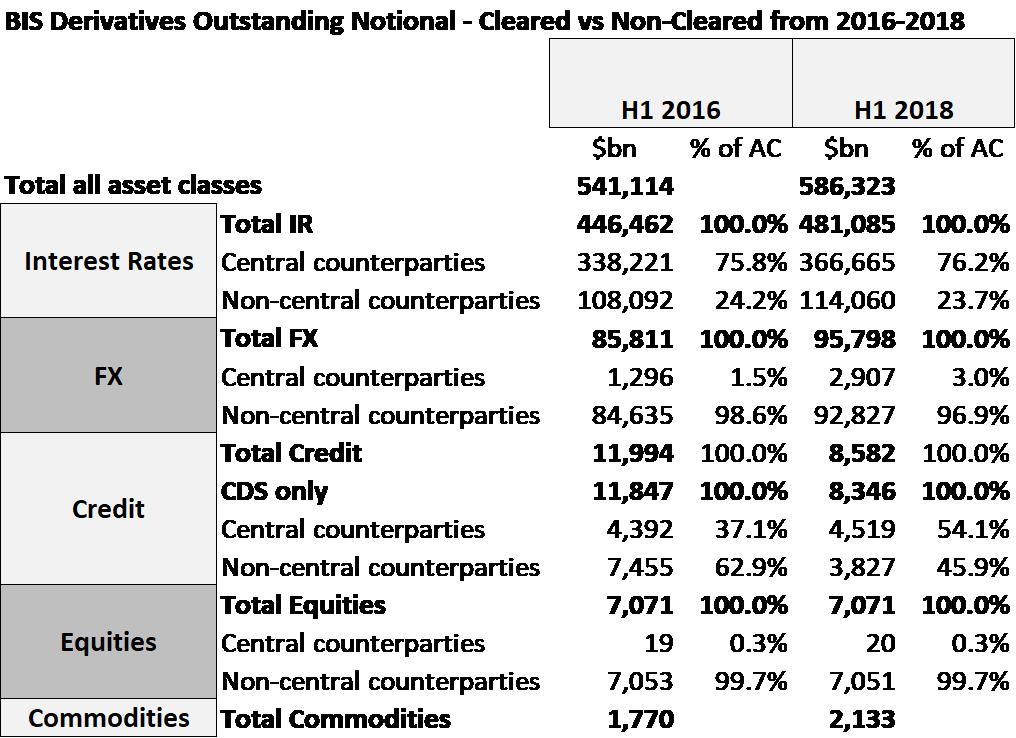

Let’s take a look at the trend over time. With a bit of transcription of numbers from BIS reports, and pulling out central counterparties from the others in a spreadsheet and comparing H1 2016 (before the first UMR date in September 2016) with the most recent figures, we can see the following:

Source: BIS OTC Derivatives Outstanding H1 2018 and H1 2016

- IR: a small percentage 0.4% shift toward clearing.

- FX: a small percentage shift 1.5% toward clearing, likely due to increased NDF clearing.

- CRD: a larger shift (17%) toward clearing mainly due to a $3tn reduction in notional in dealer to dealer portfolios rather than an increase in clearing per se.

- Equities: no change. There is no CCP offering to clear equity total return swaps which are the bulk of the problem here. Not being clearable another solution is required. There were times during 2018 when equity risk was the greatest SIMM IM contributor. I suspect but would like to confirm, that this is because of the one-way cash principal on the product.

Current Uncleared Product Breakdown

Next let’s take a look at the uncleared notional by product to get a sense of what is still to be tackled.

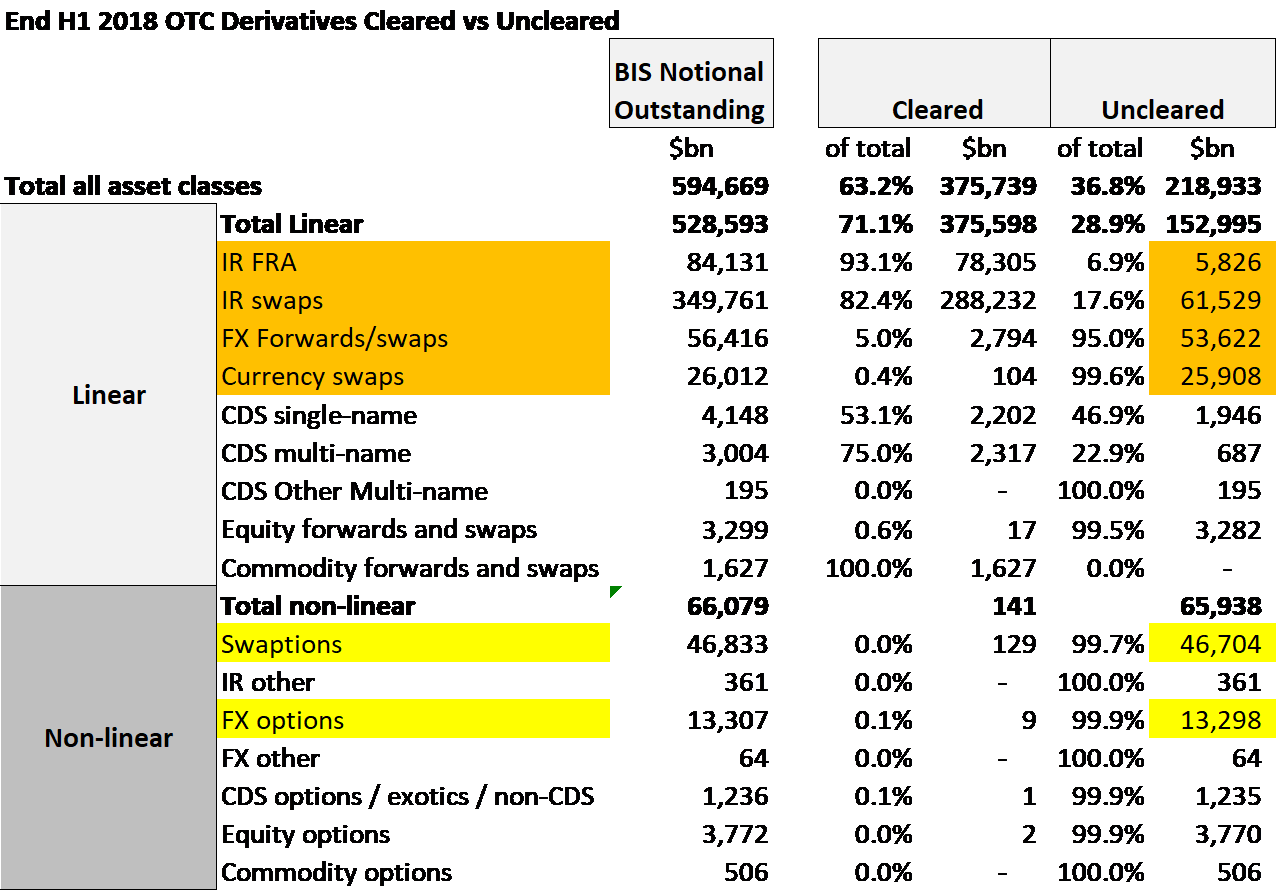

I re-organized the latest end-June 2018 BIS notional outstanding numbers by Linear vs Non-Linear product instead of asset class. I also brought in the BIS’s own cleared and uncleared split figures for IR, FX and Equity derivatives from detailed sub-analyses. These are not available for Credit and Commodities so I made some guesstimates for them to complete the picture.

Source: BIS OTC Derivatives Outstanding H1 2018

I have highlighted the big chunks of uncleared notional highlighted in orange and yellow. All are interest rate or FX products.

Before analyzing it’s worth noting a key point on relative riskiness – FX volatility is much higher than Rates volatility. Anecdotally, FX VAR is approximately 10:1 with IR VAR in a typical cross-currency swap which is a product which comprises both an FX swap and an IR swap.

Ignoring non-linear risk for a moment, the notionals highlighted break out $114tn IR vs $93tn FX. In terms of UMR caught products we have $114tn IR vs $13tn FX. This shows that the FX delta contained in linear FX deliverable swaps (forwards, swaps, cross-currency swaps principal exchanges) is probably the largest component of uncleared risk and is exempt UMR.

This also may explain why anecdotally FX risk is the largest component of SIMM IM even though this is only driven by FX options.

IR and FX linear swaps further clearing potential

Reviewing the products with large uncleared notional (highlighted orange above):

- Rates linear swaps (FRA/IRS) haven’t shifted much more to clearing since Sep 2016. There has been progress with some smaller notional products which are not mandated but incentivized by UMR and where clearing infrastructure is already in place in banks. Examples are inflation swaps, non-deliverable IRS for both of which D2D trading moved decisively to trading cleared soon after Sep 2016. This contributed to a decline in D2D uncleared notional from $43.5tn at end H2 2016 to $40.7tn at end H1 2018 even as total notional outstanding rose from $385tn to $481tn. I expect there’ll be some shift of the $62tn uncleared to clearing as UMR 4 and 5 kick in and clearing becomes the cheaper rather than more expensive approach for buy side firms.

- FX linear deliverable swaps (forwards / swaps / cross-currency principal exchanges) are not clearing mandated or caught by UMR leaving bank leverage and ccRWA as the only incentive to reduce risk. Clearing is available (e.g. ForexClear, HKEx) but with no new incentive there has been no shift. Perhaps Basel III incentives will reach the senior management pain point in banks?

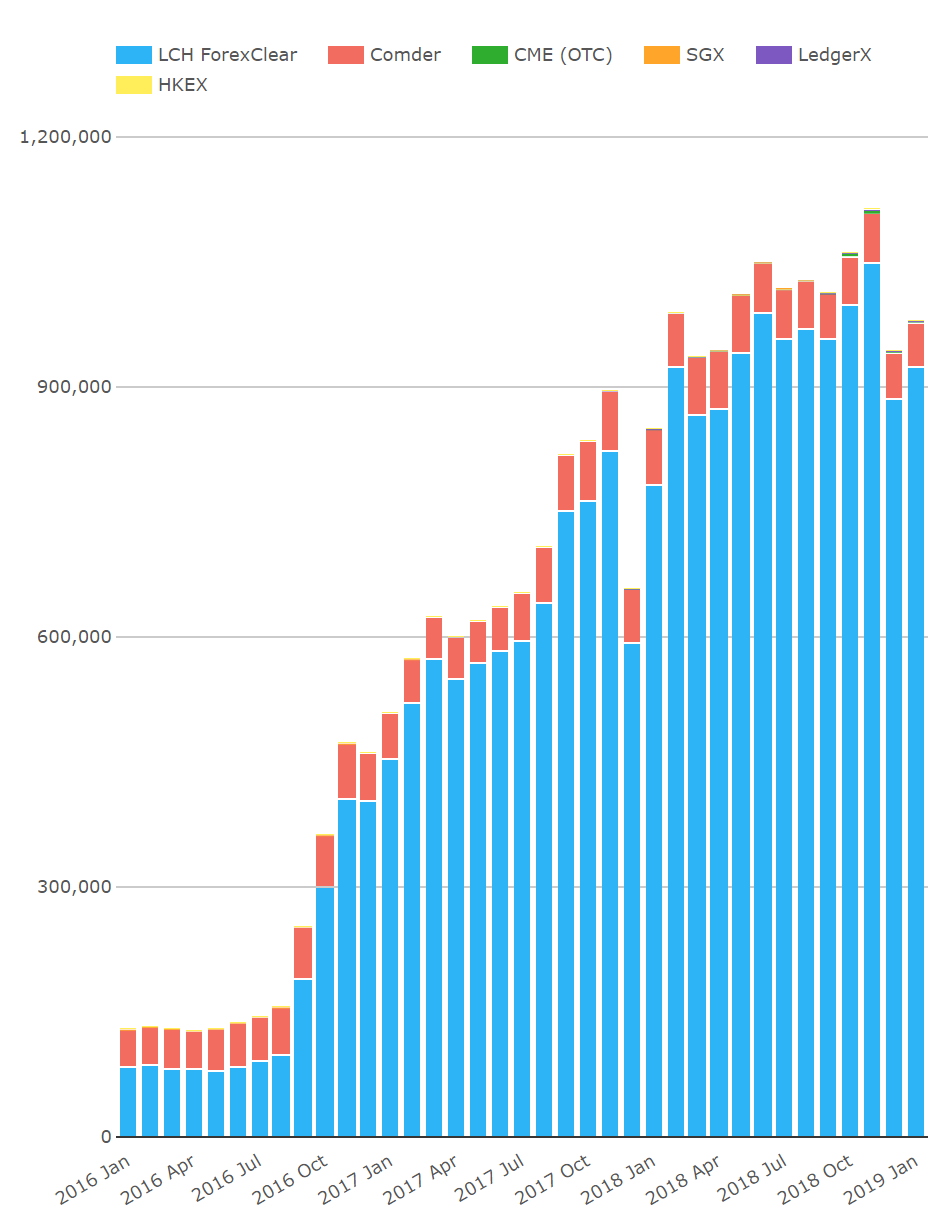

- FX linear non-deliverable swaps (NDFs) are caught by UMR but not clearing mandated. NDFs in non-deliverable currencies have shifted to clearing but are small scale compared with G10 deliverable forwards, cleared notional outstanding is up to $1 trillion with vast majority at LCH ForexClear.

Cleared FX Derivatives Monthly Notional Outstanding by CCP ($m)

In summary, moderate further elective clearing shifts are likely in IR swaps, possible in single name CDS and likely in FX NDFs as UMR 4 and 5 happen. This will lead to FX deliverables becoming a greater and more singular blot on the landscape of uncleared counterparty risk.

Options potential for clearing

When we look at non-linear OTC derivatives, the clearing profile changed in 2018.

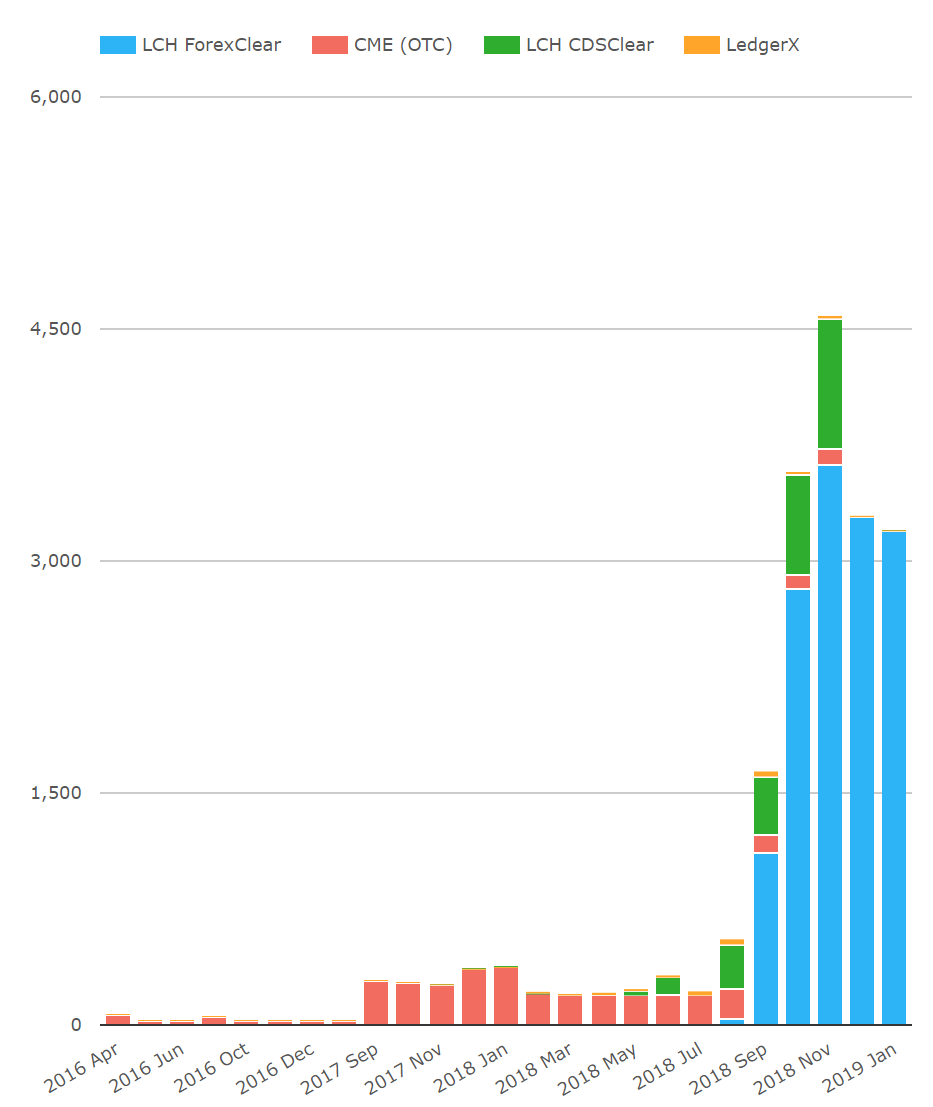

Cleared OTC options (Monthly notional outstanding $m)

Source: ClarusFT CCPView

- USD Swaptions at CME after low volumes over several months, as of Dec 6th have zero outstanding notional and the even the peak of less than $1bn cleared notional outstanding looks like proof of concept volumes given that almost $1tn G4 IR swaptions traded per month in the US person market alone.

- iTraxx Swaptions at LCH CDSClear after some volume in 4Q 2018, also now have zero outstanding notional and the peak of less than $1bn cleared notional outstanding is far from the $100bn USD CDX swaptions traded per month in the US person market alone.

- ICE plans to start clearing CDX swaptions – once it has replaced it’s stress-based IM with Monte-Carlo SIMM based IM to allow cross margining between swaptions and swaps.

- FX options at ForexClear are the only option product with meaninfgul outstanding cleared notional at end 2018 (at ~ $3bn cleared notional outstanding and cleared traded notional also $3bn per month). This is a start but still proof of concept volumes compared with $13tn uncleared outstanding notional at end June 2018 and US person traded notional alone at $1tn per month.

Options clearing pitfalls – It’s worth noting some potential option specific pitfalls which can lead us to doubt the feasibility of clearing dominating OTC options volume:

- Products may have less participants which limits counterparty netting benefit

- Products may be illiquid leading to concern for reliability of bids in a default auction

- Products may have fat tail effects leading to more conservative MPOR or liquidity add-ons in the CCP IM model – muting the funding benefit vs uncleared

In summary, whilst the first chart looks dramatic the scale of OTC options clearing remains tiny in context of the total OTC options outstanding notional. Sustainable OTC options clearing has not yet been established.

Let’s see whether ramping up and new initiatives combined can get OTC options to say $1tn of cleared outstanding notional.

Complementary market solutions

In parallel with the long range clearing dynamic, some complementary solutions have emerged partly by initiative directly between counterparties and partly through third party vendors.

For now, I list the terms I use and will elaborate more in my next post. The solutions include:

- “uncleared delta hedging”

- “risk compression”

- “delta clearing”

- “product substitution”

- “market risk off”.

All of these happen today at some scale, though the actual volumes are hard to gauge given that these are not disclosed and are difficult to isolate in public reporting.

A few unique features of these solutions:

- Some reduce actual counterparty risk by adding new uncleared trades (increasing uncleared notionals, rendering BIS notionals less useful to measure uncleared risk, adding bank leverage).

- Some require partnering with utilities (e.g. SEFs) to make them practical / operationally efficient.

- Some require ingenuity to avoid being unintentionally blocked by the clearing mandates.

Conclusion

Clearing has delivered a lot of counterparty risk netting so far. Time will tell how much more it has to offer for clearable products and whether further products will clear successfully.

It feels like the new complementary market solutions have a bigger part to play in this wave of uncleared risk reduction.

Watch out for my next post where I will elaborate these further.