- We run through activity in RUB Rates, CDS and FX markets.

- Data shows that CDS markets are continuing to trade, with 25-30 cleared trades every day.

- Risk is reducing, with Notional Outstanding in CDS reducing most days.

- RUB NDFs have seen Notional Outstanding reduce by 60% recently.

RUB IRS Markets

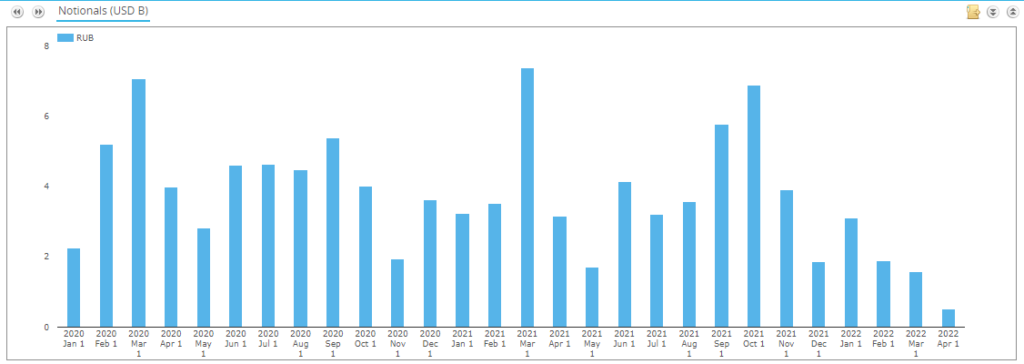

To start with, I will take a quick look at volumes in Rates markets. What does US transparency data show us about activity in RUB IRS recently?

This makes interesting reading!

- RUB IRS trading has slowed, but it has by no means ground to a halt in the US data.

- January saw over $3bn notional equivalent traded. February and March were lower, at $1.5-1.9bn each.

- However, these amounts are similar to previous dips in activity. December 2021 saw just $1.87bn trade, and May last year just $1.69bn.

Unfortunately (or maybe fortunately for the CCPs!), RUB IRS are not cleared anywhere. This means we do not have any data on Notional Outstanding for RUB IRS. Therefore, we do not know whether the IRS activity we are witnessing above is risk reducing or not. The CFTC do provide data on Notional Outstanding for Uncleared markets via the CFTC Weekly Swaps Report, but it does not break this down to include RUB:

RUB CDS Markets

As we noted previously, ICE provides commendable transparency into CDS trading versus the Russian Federation. Let’s see what has happened to both activity and notional outstanding in these important CDS contracts.

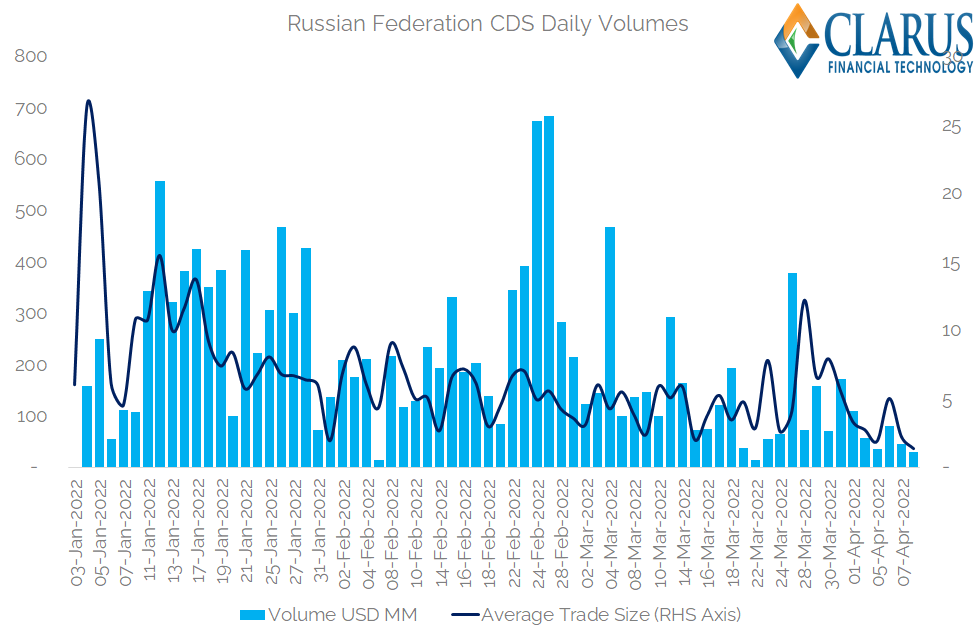

First up, Daily Volumes in 2022:

Showing;

- Daily volumes of CDS cleared at ICE Clear Credit referencing the Russian Federation.

- This is only the cleared portion of the market. SBSDR data also provides data for uncleared trades, but only for the US Persons portion of the market.

- ICE data covers the entire global cleared market.

- The cleared CDS market referencing the Russian Federation has seen a reduction in the average trade size, but ICE still sees 20-30 trades being cleared every single day. Impressive!

- Average Trade Size in April so far has been ~$2.7m. This was $5.1m as recently as February and as high as $8.6m in December and January.

- But the CDS is still trading, which I think should be the key take-away from this chart.

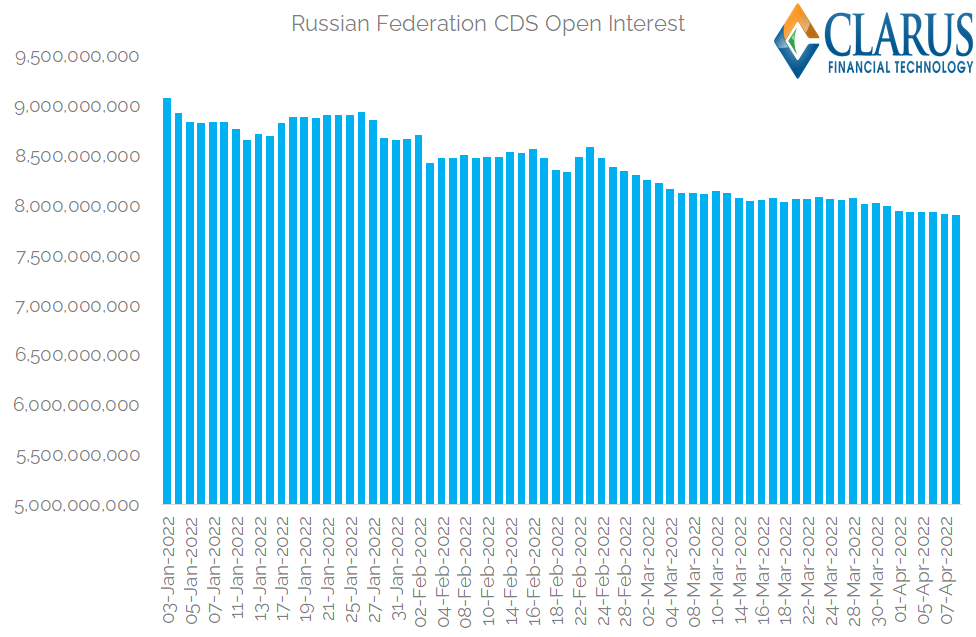

As well as monitoring on-going trading activity, we can also see the daily evolution of Open Interest in Russian Federation Open Interest at ICE. How much of this continuing activity is actually risk reducing?

Showing;

- Open Interest in Russian Federation CDS has gradually reduced all year, from $9bn to $7.9bn now.

- That suggests that Open Interest is reducing by about $16m per day in 2021.

- With Average Daily Volumes of about $180m per day in 2021 (previous chart), not all activity is directly risk reducing.

- It is worth noting that Open Interest has reduced on 72% of the trading days since the invasion on February 24th. So whilst gross notional traded is much larger than the reduction in Open Interest we see each day, risk reduction activity is really the theme here.

- From the data, it suggests the market is functioning well.

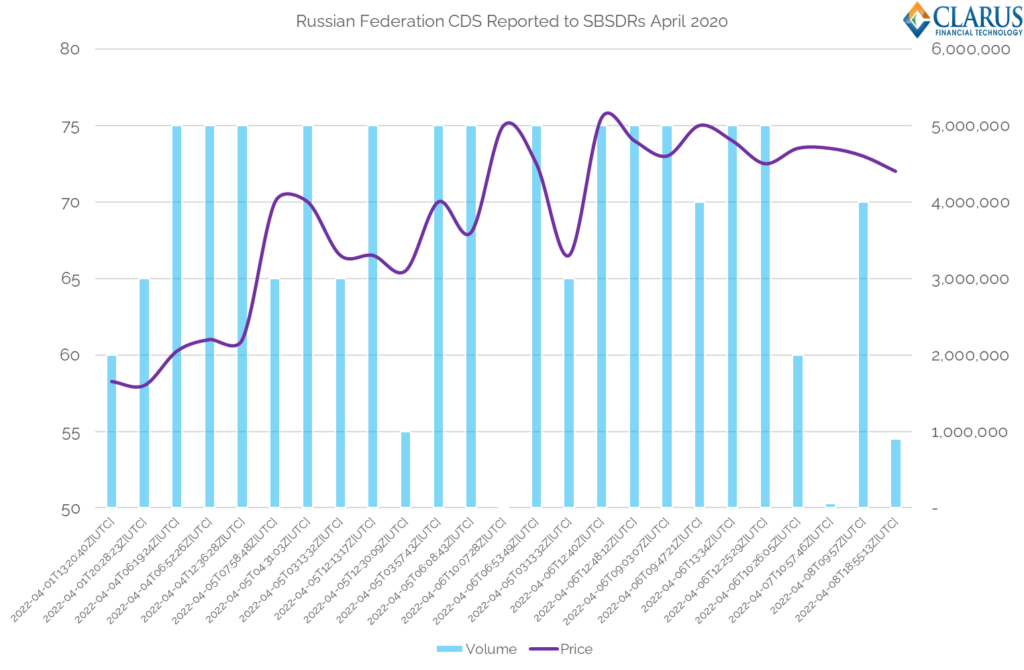

We can also turn to our new SBSDRView data product to look into prices of Russian Federation CDS. With everything trading in April as Upfront Points, we can see how prices have evolved. The 5Y Tenor is the most reported product, with 25 trades so far in April:

Showing;

- 25 trades so far in April (up to the 12th)

- Most trade sizes are above the cap notional reporting threshold of $5m, so take the notional with a pinch of salt.

- Prices are trending higher.

- We started the month at 58 Upfront Points to insure against Russian Federation default.

- This has gradually trended higher, to sit as high as 72-75 points now.

Will trading continue as default approaches? It will be fascinating to follow the data to find out.

RUB NDFs

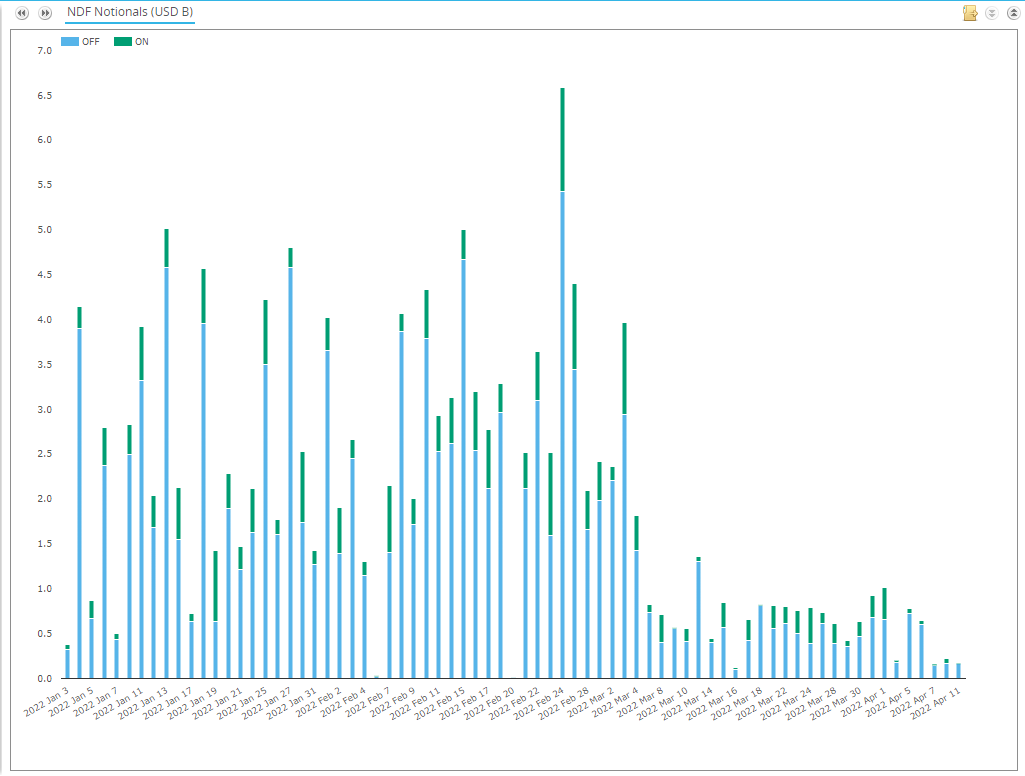

Elsewhere, following up on Amir’s rundown of RUB NDF trading, we continue to see a waning of trading activity in SDRView:

Showing;

- USDRUB NDF activity reported by US Persons to US SDRs.

- As Amir highlighted, activity peaked at nearly $7bn on 24th February.

- Most activity is traded off-SEF.

- Volumes have gradually slowed to a relative trickle, with just $0.2-0.7bn trading daily in April.

This is just a portion of the global market, but is likely representative of decreasing activity. This is significant in terms of the backdrop of prices in USDRUB NDFs, which has seen the RUB rebound significantly since March.

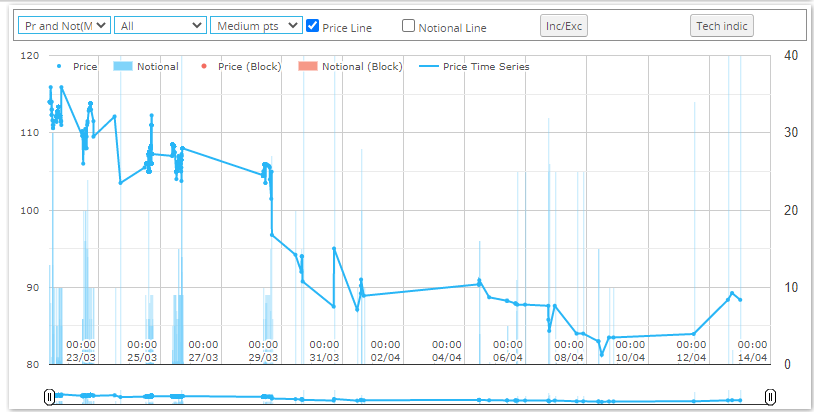

Showing;

- USDRUB NDFs maturing on the Jun22 IMM (15th June 2022), which has been the most traded recently.

- We saw prices as high as 114 RUB per USD on 21st March.

- The RUB has rallied significantly since, hitting values between 81.25 – 84.

- As the SDRView volume data shows, the RUB strengthening has happened against a backdrop of significantly reduced activity.

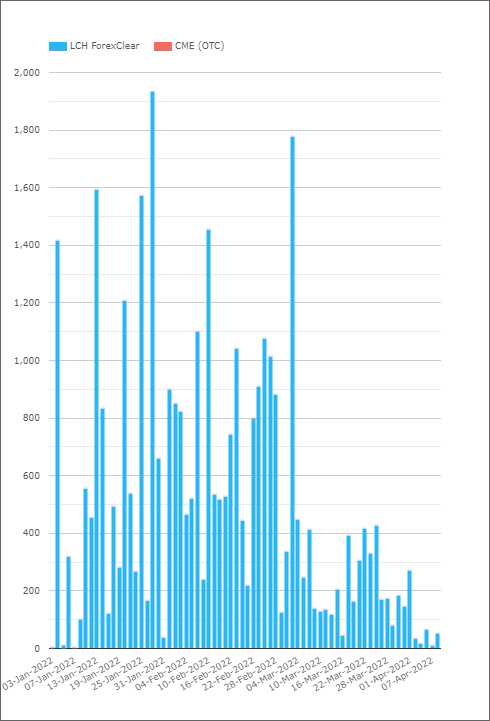

It is therefore with much intrigue that we look into the cleared market for USDRUB NDFs, to see what activity has been like and where Notional Outstanding/Open Interest now lies. First up, cleared volumes:

Showing;

- Much as with SDR reported volumes (which are mainly marked as uncleared remember), there has been a substantial reduction in daily volumes since March 2022.

- Daily cleared volumes are smaller than reported volumes to SDRs, peaking at under $2bn per day, and recently clearing as little as $20m-50m per day.

As we noted in CDS, this volume activity does not tell us whether the trades are risk reducing or not. However, because this is a cleared market we can look at Notional Outstanding to see what has happened to the overall risk outstanding. Recall that Amir looked at this in his blog as recently as March 9th (one month ago) and outstanding notional had hardly moved. What a difference a month makes!

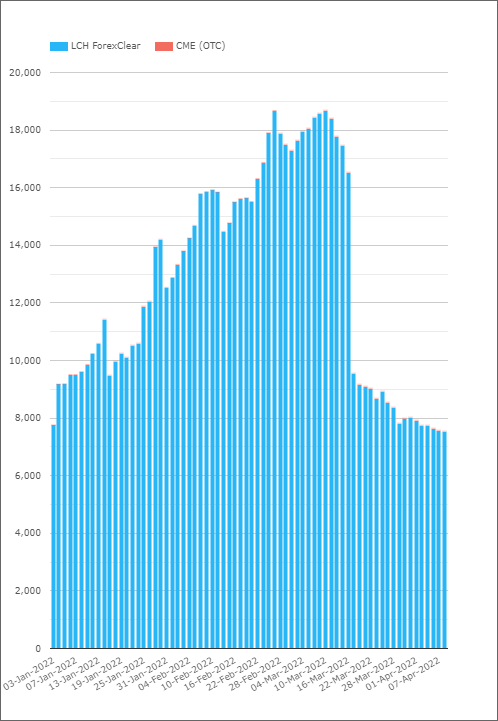

Showing;

- Notional Outstanding in cleared USDRUB NDFs.

- On 16th March 2022, the most recent IMM date, there was a substantial reduction in notional outstanding.

- This is likely as a result of IMM positions not being rolled, and being allowed to expire.

- The total Notional Outstanding has decreased from a high of ~$18.7bn on 25th February to $7.6bn now.

- That is a 60% reduction in Open Interest, most of which happened over the IMM roll.

- Notional Outstanding declined from $16.5bn to $9.5bn, a 43% reduction on the IMM date.

It will be interesting to monitor how Notional Outstanding evolves from here. Will we see another reduction over month-ends or the June IMM? Will CCPs increase margins further? The data will help us monitor these important events.

I think it is a positive sign for the market overall that risk has decreased in the system, and that a healthy amount of risk can be removed in such a short period of time.

In Summary

- Activity across Rates, Credit and FX RUB derivatives is continuing, but at much reduced levels of activity.

- Clearing brings valuable transparency to stressed markets, allowing us to monitor Outstanding Notional in RUB Credit and FX derivatives.

- Russian Federation CDS markets continue to trade even as prices increase and default approaches.

- Notional Outstanding has decreased in Russian Federation CDS by about 13% this year, and average trade sizes have reduced.

- The largest change we see is in cleared USDRUB NDFs.

- Notional Outstanding in NDFs has reduced by a huge 60% since the end of February, mainly across the March IMM roll.