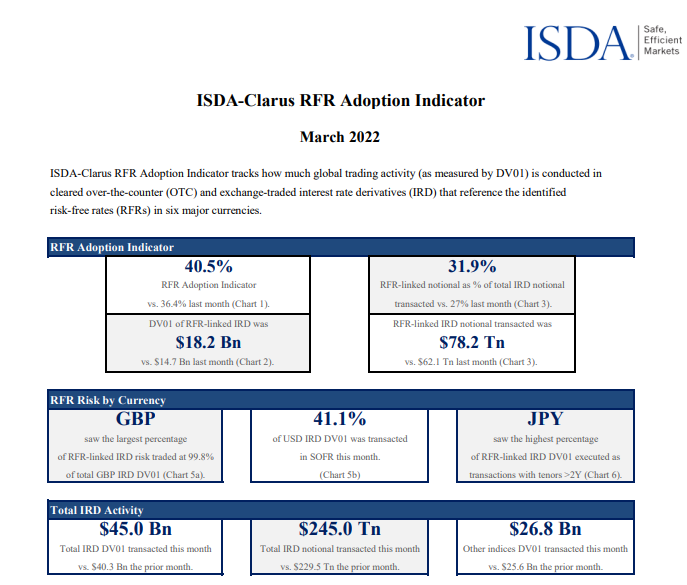

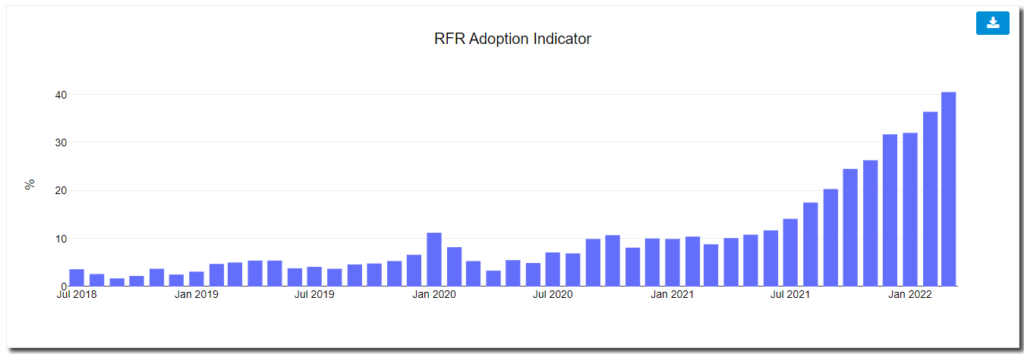

- The ISDA-Clarus RFR Adoption Indicator jumped to a new all-time high of 40.5% in March 2022.

- This has been driven by increased SOFR adoption, hitting a new high of 41.1%.

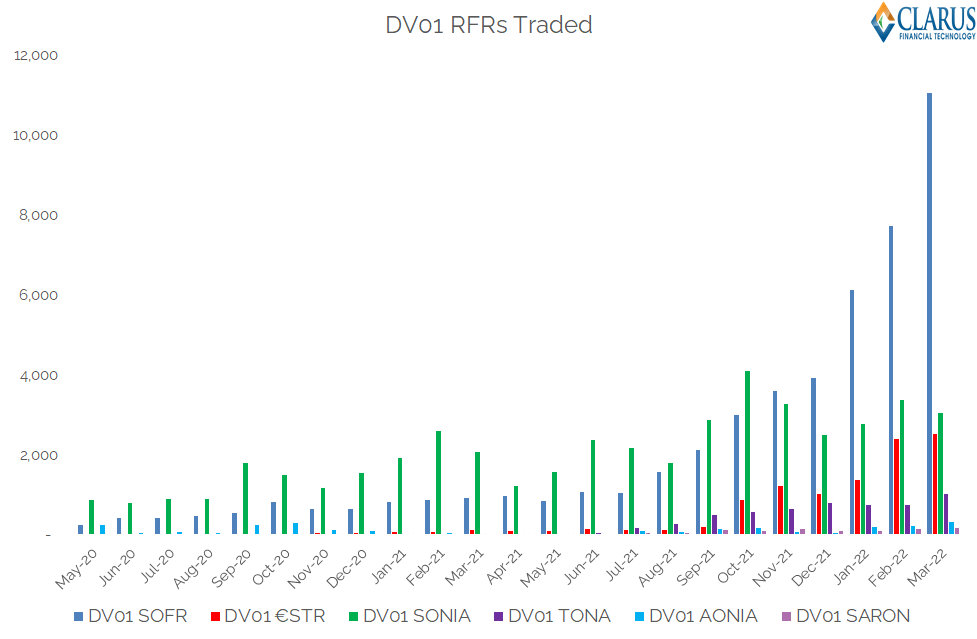

- SOFR is now comfortably the largest RFR market. More SOFR risk trades ($11bn DV01) per month than all other RFRs combined.

- 20.2% of EUR risk traded versus €STR, very similar to last month.

The ISDA-Clarus RFR Adoption Indicator for March 2022 has now been published.

Showing;

- A new all-time high of 40.5% for the overall RFR Adoption Indicator.

- March 2022 was the thirteenth consecutive monthly increase in RFR adoption, dating back to March 2021.

- SOFR adoption increased to 41.1%.

- SOFR adoption has now more than doubled since November, when it was at 19.2%.

- Virtually 100% of trading is now in RFRs for CHF, JPY and GBP. There is little reason to expect this to change in the future.

- $18.2bn of RFR DV01 was traded, 24% higher than last month and another new high for RFR risk.

RFR Adoption was very strong last month. The charts really highlight it:

Drill-Down on SOFR

There is a risk that this blog just reiterates last month’s analysis. Therefore, if you haven’t already, please take a look at SOFR Adoption from February 2022 before reading on:

Our previous blog looked to answer the following questions:

- How does SOFR trading compare between Futures (ETD) and Swaps (OTC)?

- What is happening to LIBOR risk traded in Futures and Swaps markets?

This month, the data is really about how impressive SOFR trading has been in March 2022. I don’t recall any RFR market adding so much risk in such a small period of time before.

Showing;

- The absolute amount of DV01 traded in each RFR per month since May 2020, when the overall Adoption Indicator was at just 5%.

- In May 2020, only 1.9% of total USD risk was traded versus SOFR!

- This data is not reported on rfr.clarusft.com – we show only the percentages rather than the absolutes in the free monthly data.

- However, I thought the data so significant this month that we should expose the underlying calculations.

- As stated previously, USD SOFR accounted for 41.1% of all USD Risk traded.

- It is easy to be blasé about such a number when CHF, JPY and GBP are all at 100%.

- However, this view discounts just how large the USD Rates market is compared to everything else.

- $11bn of DV01 traded in SOFR alone. How big is that number?

- SONIA traded $3bn in DV01 during the same month. The most amount of SONIA ever traded in a month was $4.1bn in October 21.

- $11bn DV01 was double the size of the entire markets in GBP, CHF, JPY and AUD combined in March 2022!

- $11bn DV01 was larger than the entire EUR market in December 2021. Total EUR risk traded was “only” $12.5bn in March 2022.

- SOFR risk traded increased by $3.3bn DV01 in the month. That increase is larger than the entire GBP market, three times larger than the entire JPY market and also 3 times larger than the entire AUD market!

Importantly, outside of ceased LIBOR indices, SOFR is now the largest RFR market both in terms of absolute risk traded and the relative size of the RFR risk versus other indices. It is safe to say that Fed Funds have never seen this much risk trade in a single month.

Elsewhere

Regular readers may have noticed a small revision higher (by <0.1%) to the 2022 readings of the RFR Adoption Indicator. This is due to updates we made to Clarus data following a deep-dive into SARON futures. You can read the analysis in the blog link below;

Remember to subscribe to keep updated with the latest on RFR trading and our frequent analysis.