I last looked in detail at IR Futures volume in February 2021, so in this blog I will update the Average Daily Volume (ADV) and Open Interest (OI) of the major IR futures:

- Money Market and Bond Futures

- AUD, BRL, CAD, CHF, EUR, GBP, JPY and USD

- Relative size by ADV and OI on a comparable dollar notional basis

- Trends and market share in SOFR and SONIA Futures

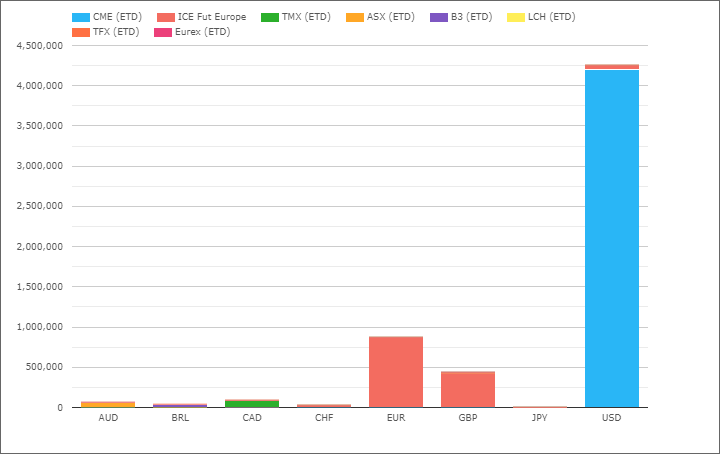

MM Futures in major ccys

In CCPView we can select MM Futures in the six major derivative currencies plus BRL and CHF.

- USD at CME the largest with $4.2 trillion ADV from Eurodollar, FedFunds and SOFR

- EUR at ICE, the next largest with $870 billion ADV from Euribor

- GBP at ICE with $430 billion

- CAD at TMX with $85 billion

- AUD at ASX with $60 billion

- BRL at B3 with $30 billion

- CHF at ICE with $20 billion

- JPY at TFX with $600 million

USD ADV higher than the $3.6 trillion in Feb-21, while EUR and GBP lower than the $1 trillion and $950 billion respectively in Feb-21.

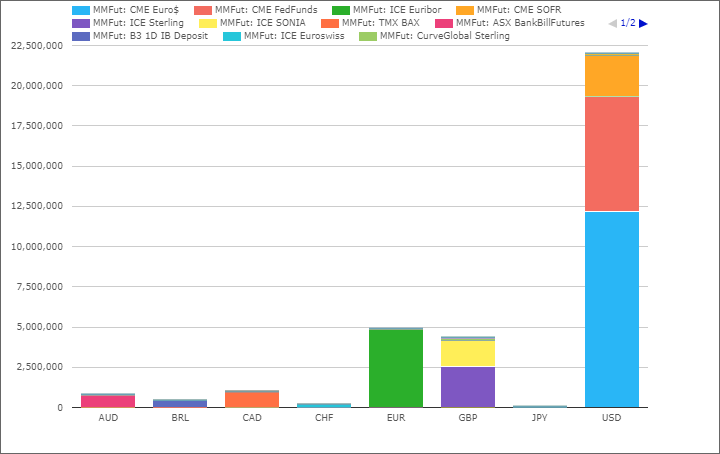

Next changing to Open Interest and by futures contract within currency.

Ranking each of the 20 contracts by OI:

- CME Eurodollar the largest with $12.4 trillion

- CME FedFunds next with $7.1 trillion

- ICE Euribor $4.9 trillion

- CME SOFR with $2.5 trillion

- ICE Short Sterling $2.5 trillion

- ICE Sonia with $1.6 trillion

- TMX BAX $970 billion

- ASX Bank Bill Futures $750 billion

- B3 1D IB Deposit $435 billion

- ICE EuroSwiss $220 billion

- LCH CurveGlobal Sterling with $120 billion

- ICE SOFR with $107 billion

- ASX Cash Future with $80 billion

- LCH CurveGlobal Sonia with $68 billion

- TFX Euroyen $64 billion

- LCH CurveGlobal Euribor with $51 billion

- CME Sonia with $15.7 billion

- CME BSBY with $12 billion

- Eurex Euribor with $5.5 billion

- TMX CRA with $1.8 billion

Noteworthy changes from our Feb-21 list are:

- CME SOFR has moved above ICE Short Sterling (from 5th to 4th)

- ICE Sonia is now 6th, up from 9th

- ICE SOFR up to 12th

- CME BSBY, a new contract on the Bloomberg Short-term Yield Index, makes an appearance

- TMX CRA, a newish contract on CAD CORRA in 20th

- LCH CurveGlobal is shutting down in Jan 2022

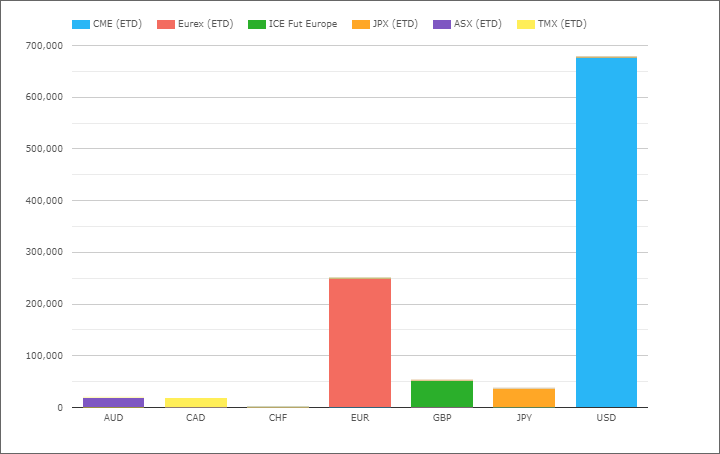

Bond Futures in major ccys

Next in CCPView we select bond futures in these currencies.

- USD at CME, by far the largest with $680 billion ADV in Nov-21

- EUR at EUREX, the next largest with $250 billion ADV

- GBP at ICE with $52 billion

- JPY at JPX with $37 billion

- AUD at ASX with $20 billion

- CAD at TMX with $19 billion

- CHF at EUREX with $7 million

USD ADV is lower than the $790 billion in Feb-21, as are EUR, GBP, JPY and AUD from $300 billion, $63 billion, $53 billion and £36 billion respectively.

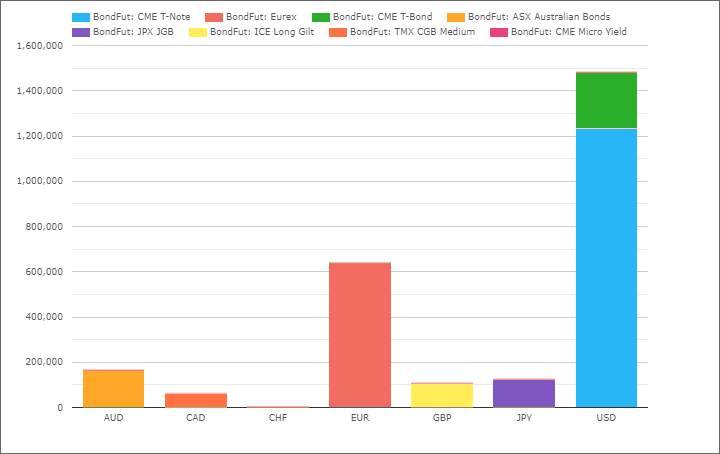

Next changing to Open Interest on November 30, 2021 and by contract.

- CME T-Note with $1.2 trillion

- Eurex Bond Futures with $640 billion

- CME T-Bond with $250 billion

- ASX Australian Bonds with $160 billion

- JPX JGB with $120 billion

- ICE Long Gilt with $105 billion

- TMX CGB with $62 billion

Th exact same ranking as is in our Feb-2021 list and smallish changes in OI, most noteworthy are ASX and JPX down from $200 billion and $160 billion in Feb 2021 respectively and ICE up from $80 billion.

Let’s next turn to Risk Free Rates, SOFR and SONIA.

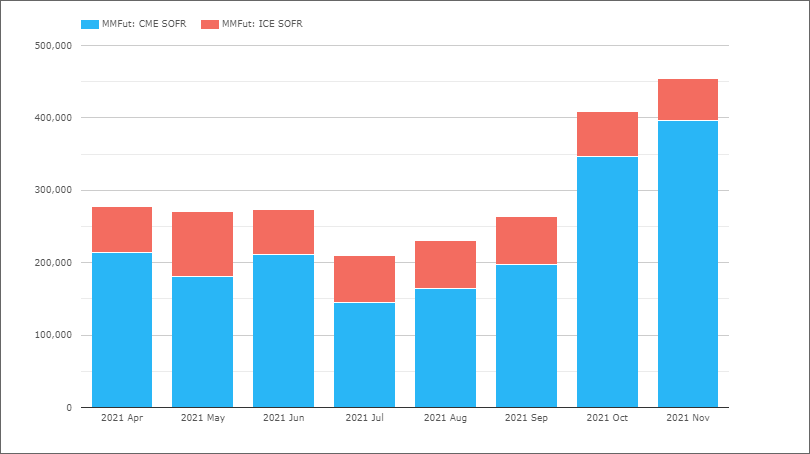

SOFR Futures

- Flat at $270 billion in Apr, May, Jun

- Summer drop in July

- Rising trend from Aug to Nov

- Nov with a record ADV of $455 billion

- CME SOFR with $396 billion ADV

- ICE SOFR with $58 billion ADV

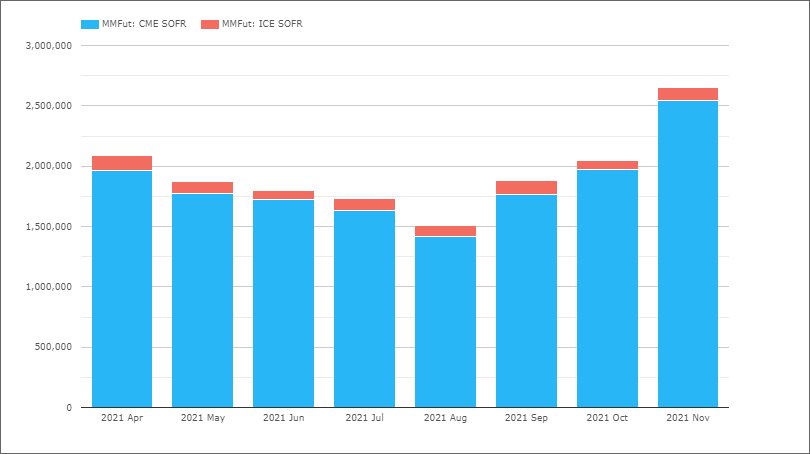

Switching to OI by month.

- April to August decline from $2.1 trillion to $1.5 trillion

- Strong upward trend since with $1.88 trillion in Sep, $2.05 trillion in Oct and $2.65 trillion in Nov

- CME SOFR with OI of $2.54 trillion at end November and ICE SOFR with $107 billion

Only an 18 month period now to June 30, 2023, for CME Eurodollar exposure beyond that date to automatically convert to SOFR Futures with a spread adjustment.

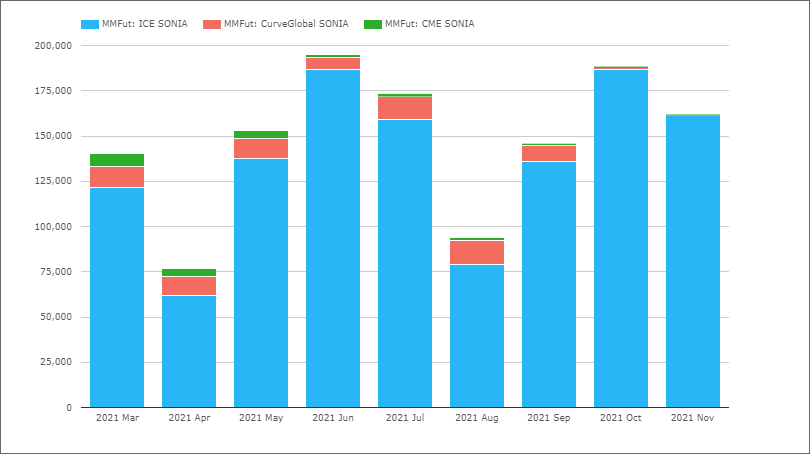

SONIA Futures

- A messy chart, with no real trend

- CurveGlobal shutting down announcement in late Sep, rapidly leading to a collapse in ADV

- ICE SONIA with £135b ADV in Sep, £187b in Oct and £161b in Nov

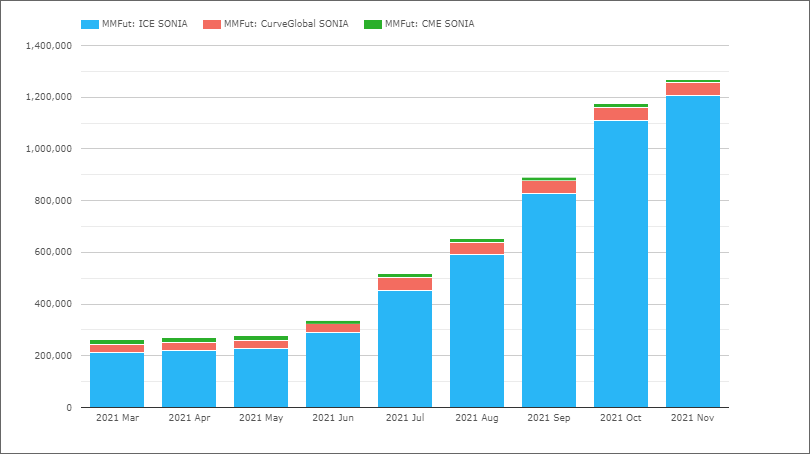

Switching to OI by month, we do see a nice trend.

- Rising nicely, month on month

- £280 billion in May, £650 billion in Aug and £1.27 trillion in Nov

- ICE with OI of £1.2 trillion

- CurveGlobal still with £50 billion

- CME with £11.5 billion

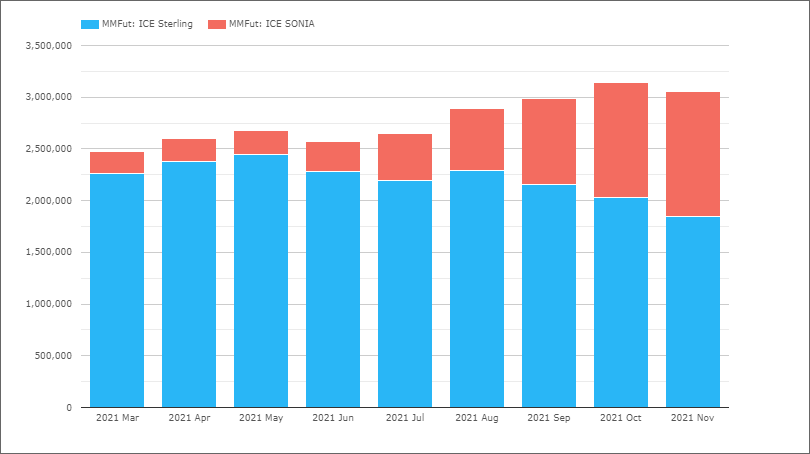

ICE Sterling and Sonia

Finally, for our last chart, let’s look at OI for ICE Short Sterling and Sonia.

A decrease in Sterling (the Libor contract) and increase in Sonia, as we would expect given the demise of Libor on December 31, 2021.

However perhaps not as much a transition to Sonia Futures as would have been expected by now.

Of-course we know that ICE plans to convert OI in Short Sterling to Sonia following the close of business on 17 December, which is also when LCH SwapClear converts GBP Libor Swaps to Sonia.

A lot of important post-trade conversion work to be done between now and Christmas.

Good luck to all involved for a smooth transition in GBP and CHF.

That’s It for today

CCPView has data on all major IR Futures.

Daily Volumes, Open Interest and ADVs.

To compare volume trends and market share trends.

In number of contracts, currency or dollar terms.

If you are interested in this data, please contact us

While option volumes and interest rate volatility have been increasing, so has the attention that the regulators are giving non-linear option products based on LIBOR. With November 8 passed, dealers are now focused on moving from LIBOR-based swaptions to SOFR-based swaptions. Indeed, with the March 2021 inclusion of SOFR-based fallbacks in the Eurodollar futures rulebook, contracts with an underlying greater than June 2023 are effectively SOFR-linked contracts.