Will today be Day One of the LIBOR end game?

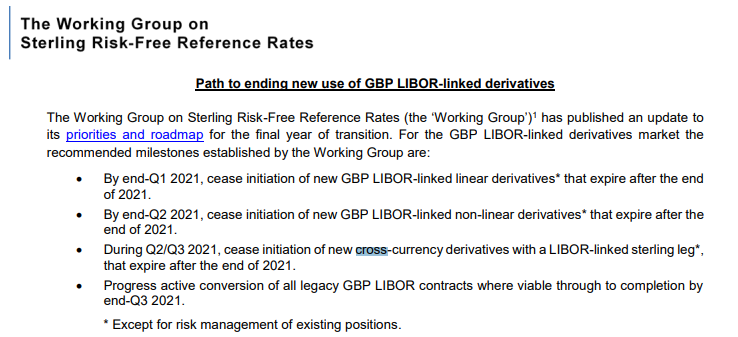

It should be, according to the latest “Dear CEO” letter from David Bailey, Sarah Breeden and the FCA: ‘Transition from LIBOR to Risk Free Rates’. The end of Q1 2021 is meant to have signaled the last day for business as usual linear GBP derivatives trading.

Today we will be looking through the data to see if this has come to fruition. Is GBP LIBOR still trading in linear derivatives markets?

April So Far in Clearing

Thanks to the Easter weekend, we are already on the 6th day of the quarter! Have we seen any GBP LIBOR trades already reported?

Looking at CCPView, with data up to the end of last week, we can already see some GBP LIBOR cleared activity.

Over £21bn of GBP-LIBOR linked FRAs and IRS have already been reported. Look at that split of activity though!

- 79% of GBP-LIBOR linked activity at CCPs in April has been due to Client activity!

- This increases to 86% client-activity if we exclude FRAs.

Do we think all of that activity was really tied to legacy or transition business?

This data does not include this week’s data, which is the first “real” trading week of the quarter. Let’s look at some fresh data.

April 1st-5th

Turning to SDRView Pro shows the following:

- £6.4bn in GBP LIBOR linked IRS was reported to SDRs from 1st to 5th April.

- Even vanilla 10Y IRS traded 49 times, totaling £920m.

- There were 182 trades in total.

- This drops to 132 trades if we exclude “backstarting” trades, which can at least firmly be recognised as legacy positions!

Hmmmm, 132 trades already….Let’s compare this to reported SONIA activity for the 1st-5th April period:

- SONIA saw 253 trades.

- A huge £28.7bn in notional.

- A ratio of 4.5x SONIA to LIBOR activity.

- Pretty good signs from a transition perspective.

April 6th 11:00 London

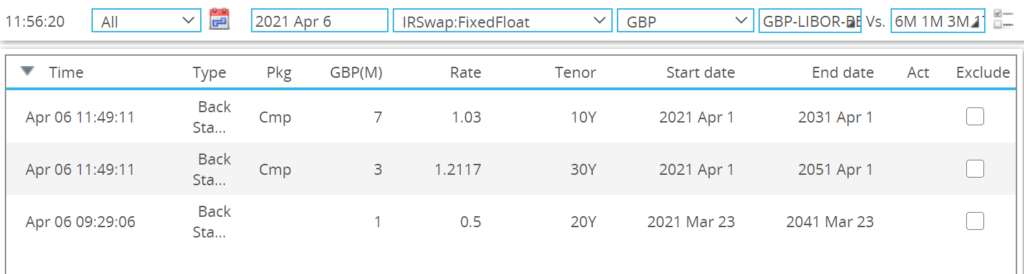

Turning our attention to today, we can still see some GBP LIBOR-linked activity being reported:

Showing;

- There have been 28 GBP LIBOR trades already today.

- £1.7bn in notional.

- Only three of these were legacy trades:

So whilst it is disappointing that GBP LIBOR activity continues to drip through, we must put it in perspective.

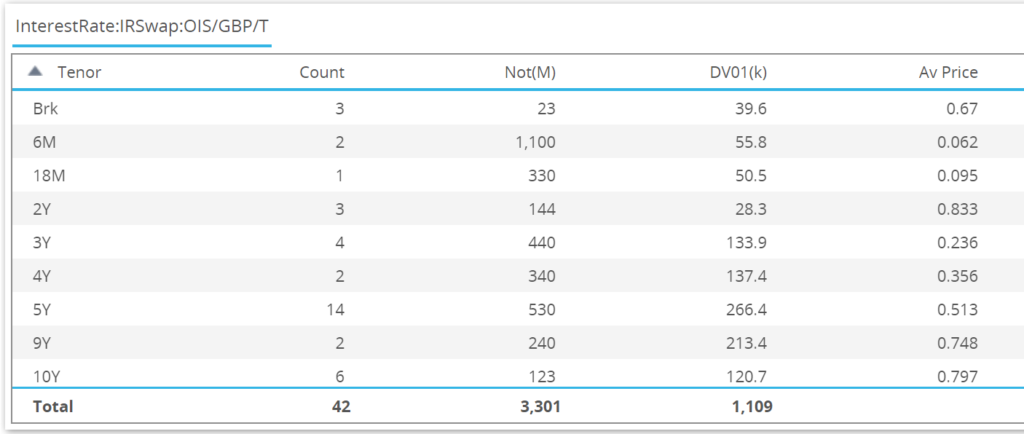

Therefore, we note how active SONIA markets have been already today:

Showing;

- 42 trades in total

- £3.3bn in notional

- Importantly, a whole load of activity across the entirety of the curve. This is no longer a short-dated market only.

- Plenty of activity in benchmark tenors such as 5Y and 10Y.

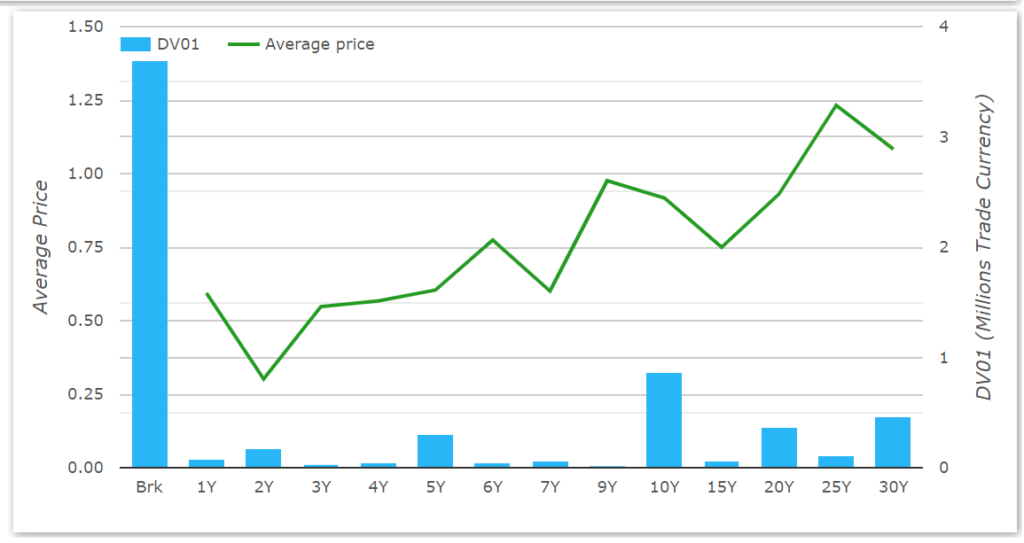

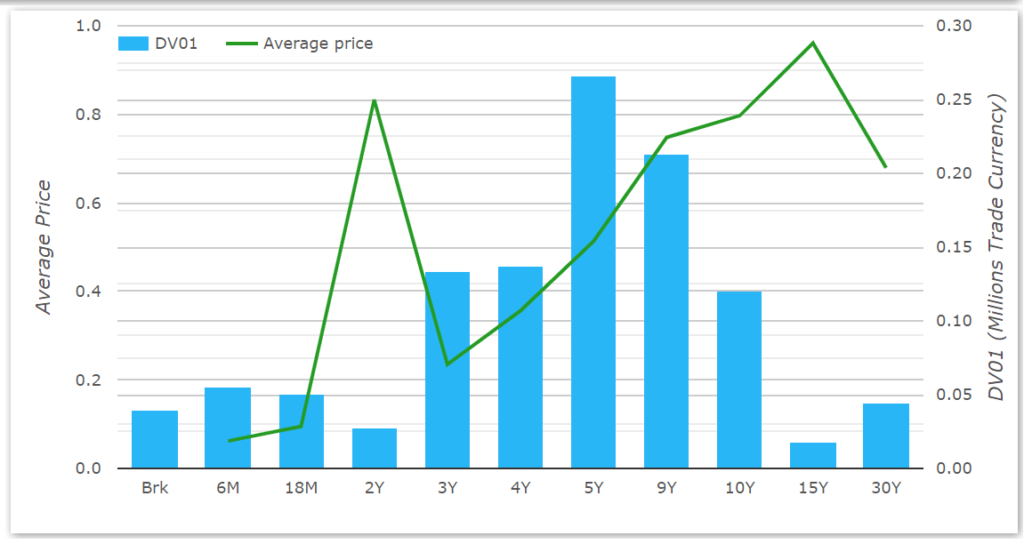

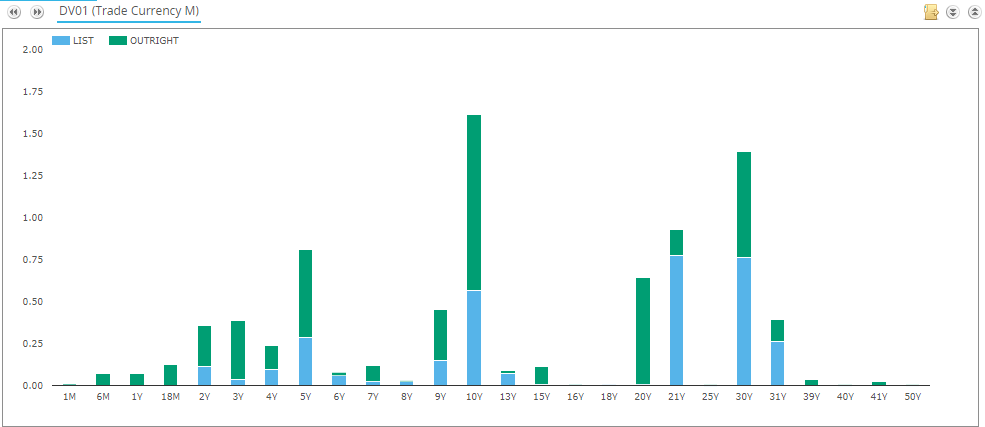

On a DV01 basis you can see that 5Y was the most active tenor:

So far there has been around 1.6 times as much activity in SONIA than LIBOR in GBP markets today. Not bad. Where will it end up today? Stay tuned for some near-live updates today.

April 6th 14:30 London

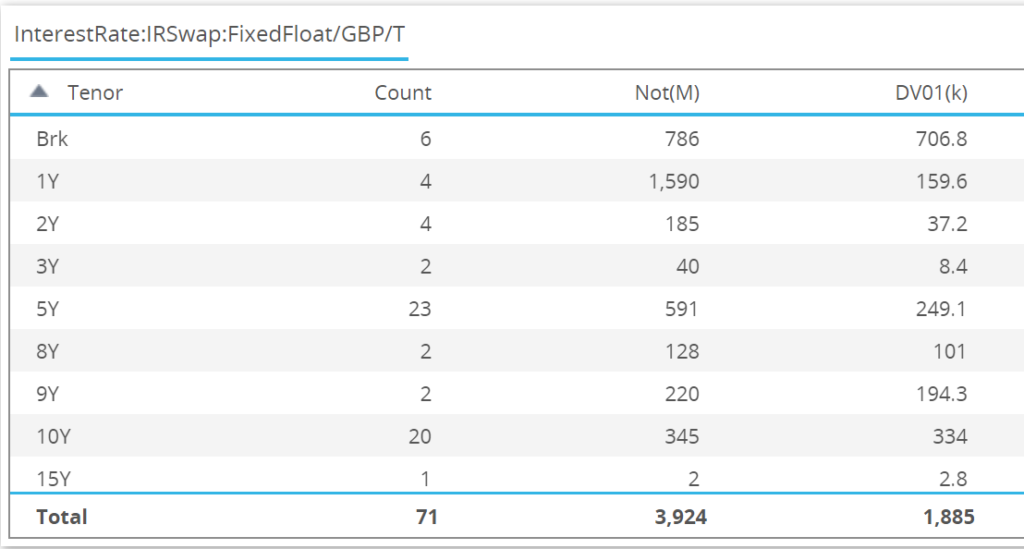

Scores on the doors halfway through the trading day. First up, the “naughty” LIBOR trades:

- 71 trades totaling £4bn.

- By my reckoning, every single trade has a LIBOR reset after the end of 2021.

- 5Y and 10Y continue to be the most active tenors. That type of pattern doesn’t fit with all of these being transition trades, surely?

However, to be fair to the GBP market, SONIA activity is continuing at a much higher rate.

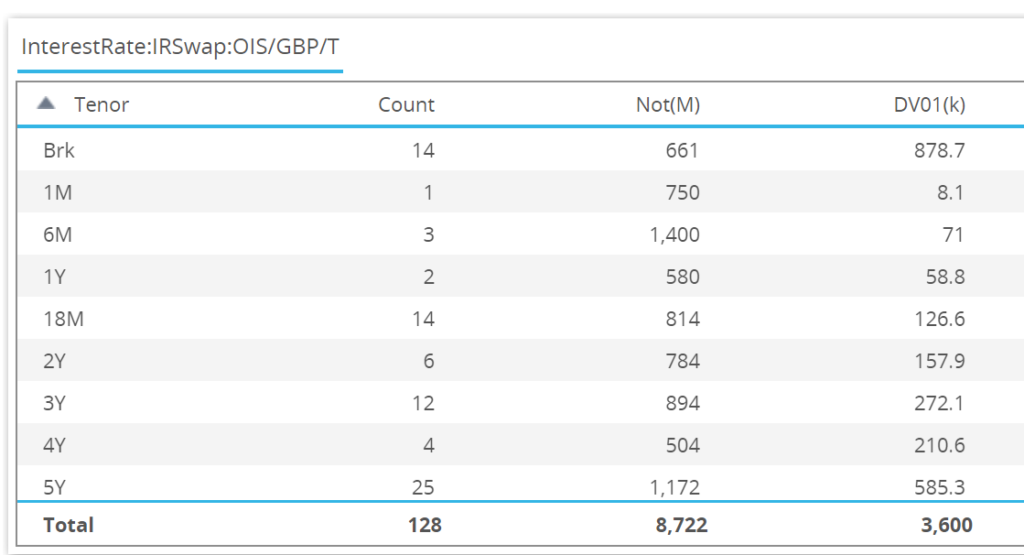

- 128 trades for £8.7bn in notional. Or £6.6bn excluding the short-dated stuff.

- £3.6m DV01 traded in SONIA, 1.91 times the amount of risk traded versus LIBOR indices.

And again, let’s take the chance to highlight that the GBP SONIA activity is across the whole curve, with 5Y and 10Y the “benchmark” tenors:

April 6th 15:30 London

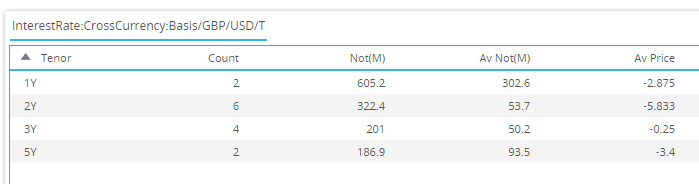

Aside from simple derivatives, we still see GBP LIBOR-based cross currency swaps and swaptions being reported to SDRs.

Today has seen £1.3bn in cable (GBP vs USD) XCCY for example:

Whilst I would consider XCCY as a largely linear derivative product, they are subject to a different timeline according to the UK RFR-working group. I guess this is due to the presence of the USD LIBOR leg as well ¯\_(ツ)_/¯?

So given the typical pace of transition, I guess we will be looking for GBP LIBOR to largely disappear from XCCY swaps on 1st October 2021.

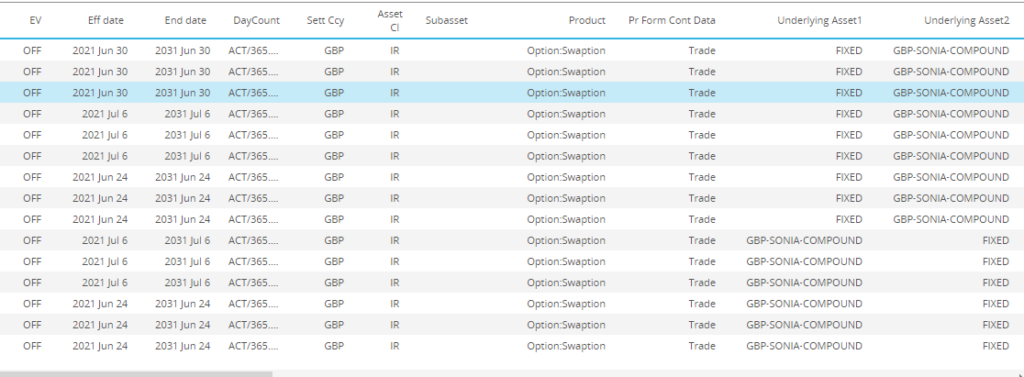

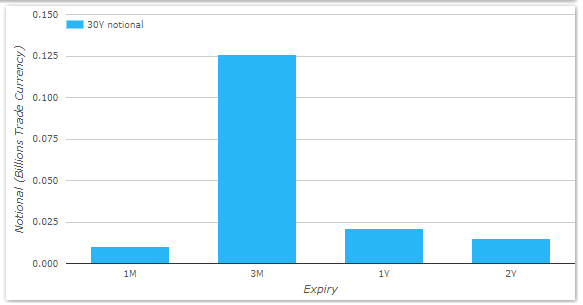

For Swaptions, we’ve at least seen a decent chunk of SONIA activity in 3m10Y Swaptions today:

But we have seen more variety in LIBOR-linked swaptions:

April 6th Recap End of Day

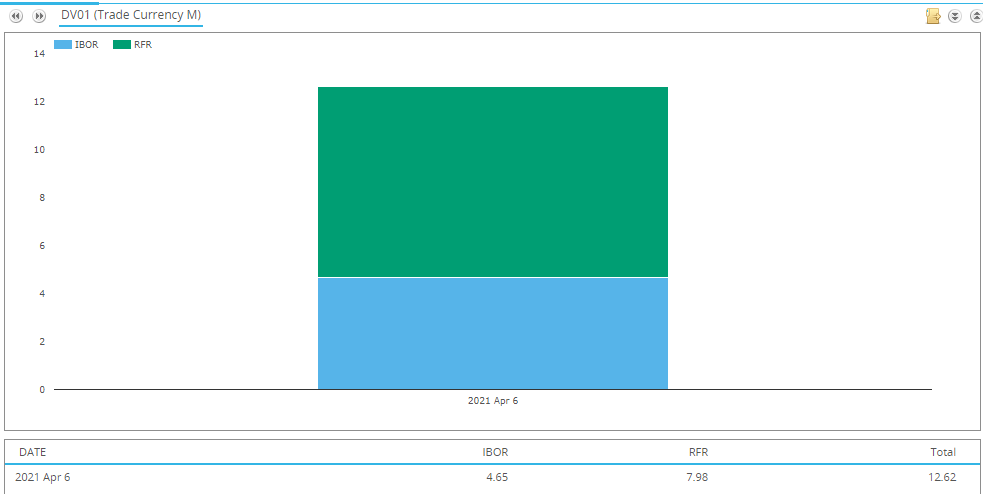

SDRView Res provides a succinct overview of trading activity in GBP markets for April 6th:

- SONIA markets saw ~£8m DV01 of activity yesterday.

- GBP LIBOR markets saw £4.65m DV01.

- 63% of activity was therefore in SONIA instruments.

The ratio of SONIA to LIBOR activity therefore tailed off a little bit during the day, ending at 1.7x as much SONIA as LIBOR activity.

So no, GBP LIBOR activity did not die completely yesterday.

What Traded in GBP LIBOR?

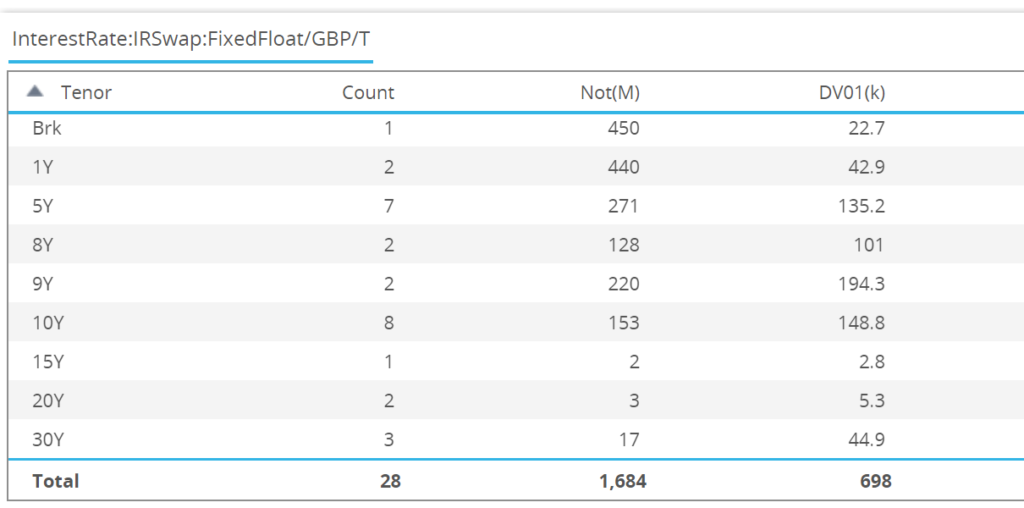

There were 117 GBP LIBOR linked trades:

- 37 of these were back-starting or compression-linked, therefore consistent with “legacy” activity.

- There were 29 vanilla, spot starting trades. 17 of these were spot starting 10Y LIBOR trades. This is the type of activity that really should get marginalised over the coming trading sessions to be consistent with the stated goals of the regulators.

It must be complicated from a compliance/record-keeping perspective to continually justify this LIBOR-linked activity. Do regulators actually ask why a particular spot-starting 10Y GBP LIBOR swap was transacted on April 6th 2021? I don’t rate their chances in getting any sensible answers if they wait more than a couple of days to ask!

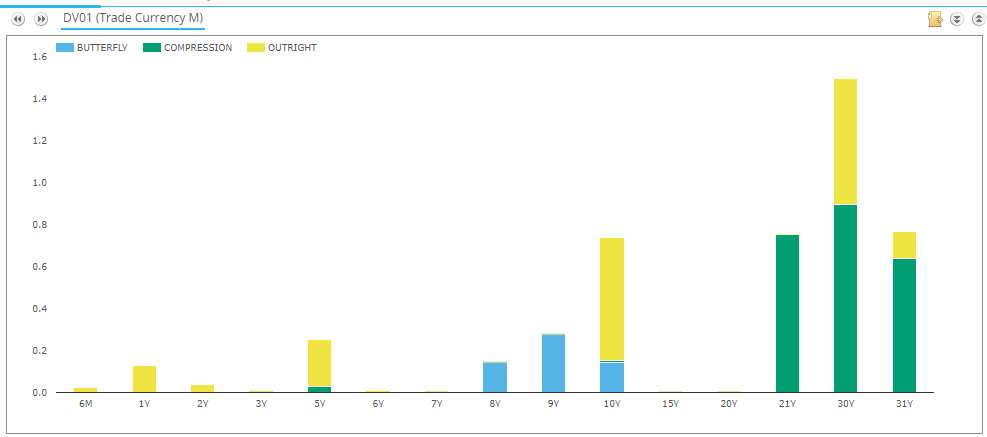

Looking at the tenor and type of GBP LIBOR activity:

- Most compression was long-dated, 20Y and 30Y tenors.

- Outrights were in the benchmark tenors of 5Y, 10Y and 30Y. There is plenty of liquidity in SONIA to trade the RFR instead in these tenors….just saying.

- There were a couple of butterfly trades in 8y9y10y. Such “microflies” could be considered risk management of legacy positions I guess.

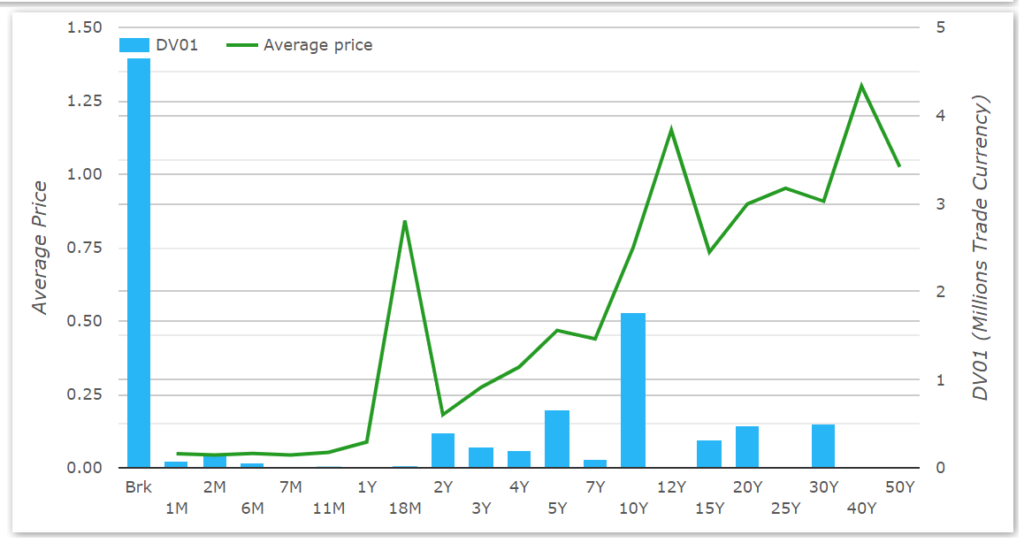

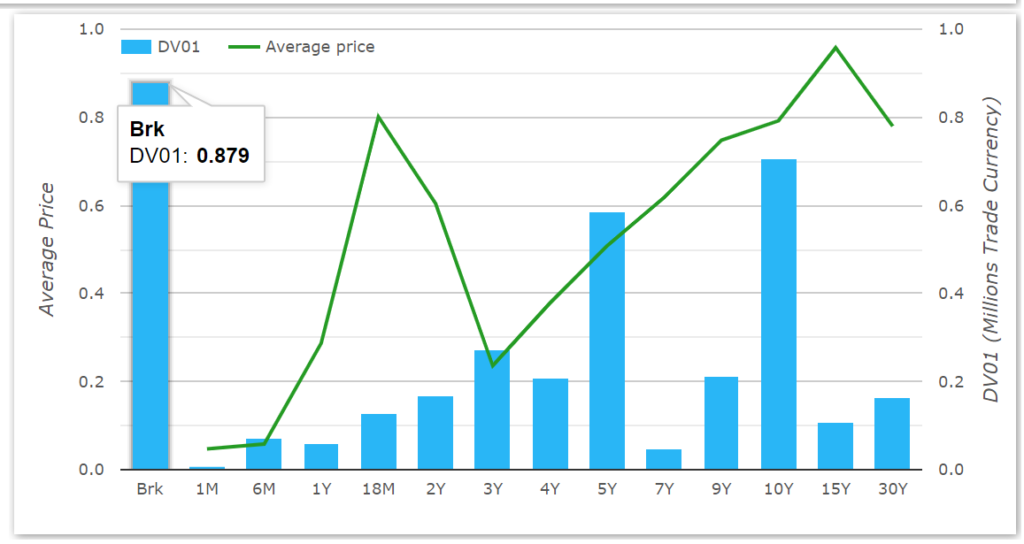

If we show the April 6th activity for SONIA by tenor instead, we see a very healthy picture:

- Activity right across the curve, from 1M to 50Y tenors.

- The activity is expressed in DV01, and shows that most risk transfer activity takes place in benchmark maturities 5Y, 10Y and 30Y.

- The 20Y area of the curve was also very active yesterday.

- List trading is in evidence, showing that end-users are also increasingly managing their risk in RFR space.

Did Anything Change?

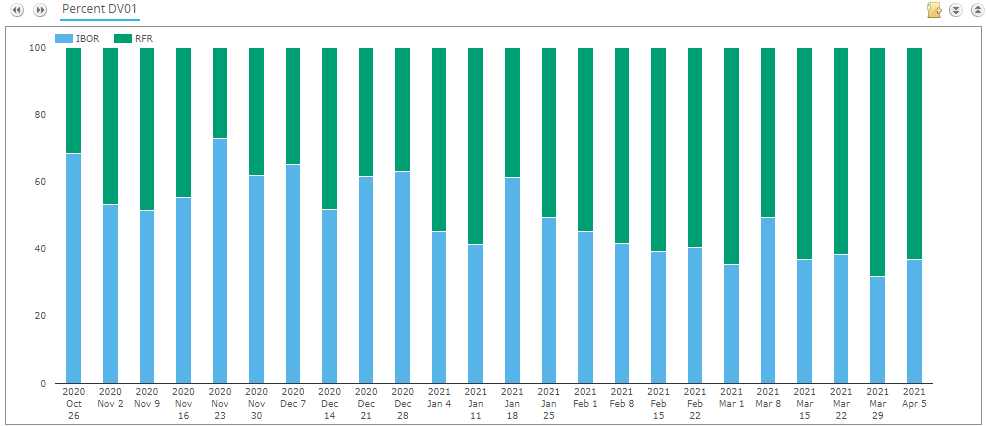

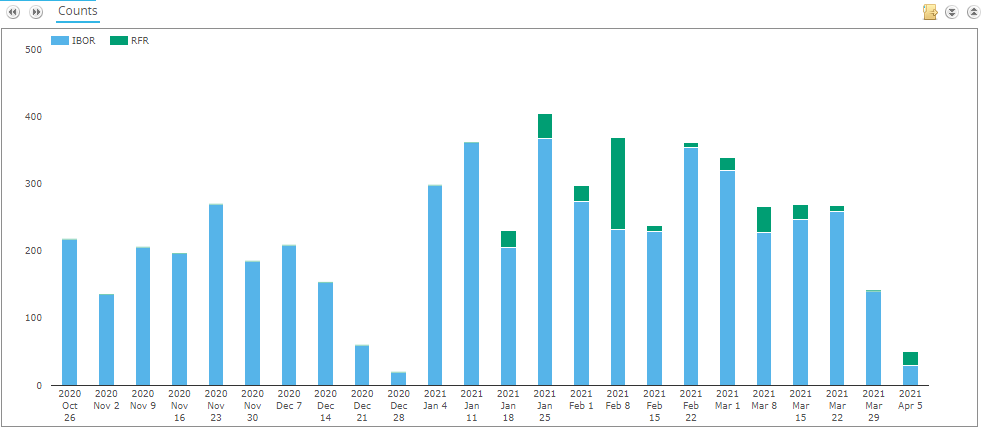

Finally, let’s put April 6th trading in perspective. We last had a “live” blog on SONIA day 2, October 26th. This was when interbank markets were encouraged to adopt SONIA as the standard quoting convention.

How has the proportion of SONIA to LIBOR risk evolved since? Looking on a weekly basis:

- 68% was LIBOR based in the week of October 26th across GBP FRAs, IRS and OIS. This is measured in DV01 terms.

- 68% was SONIA based risk in the most recent full week of March 29th!

- 63% was SONIA based risk yesterday, April 6th.

In summary, the regulatory announcement to stop initiating new LIBOR-based exposures did not have an immediate market impact on the first full day of trading. SONIA-based activity yesterday was pretty much in line with the most recent four weeks.

On the plus side, market forces have clearly been in force since October to adopt the SONIA standard. What is clear from the October announcement is that these things take time.

The only thing we can do for now is continue to monitor the data. The transition story still has a long way to go.

Non-Linear Products

The transition efforts are clearly taking effect in these most vanilla of derivatives markets. How is this impacting other markets? Looking at just Swaptions and Cross Currency swaps for example:

Back in October, we saw no SONIA-linked XCCY or Swaptions being reported to SDRs. Yesterday alone, we saw 19 SONIA swaptions and 1 SONIA vs SOFR XCCY swap! This is surely a very positive sign, albeit with quite some distance to go.

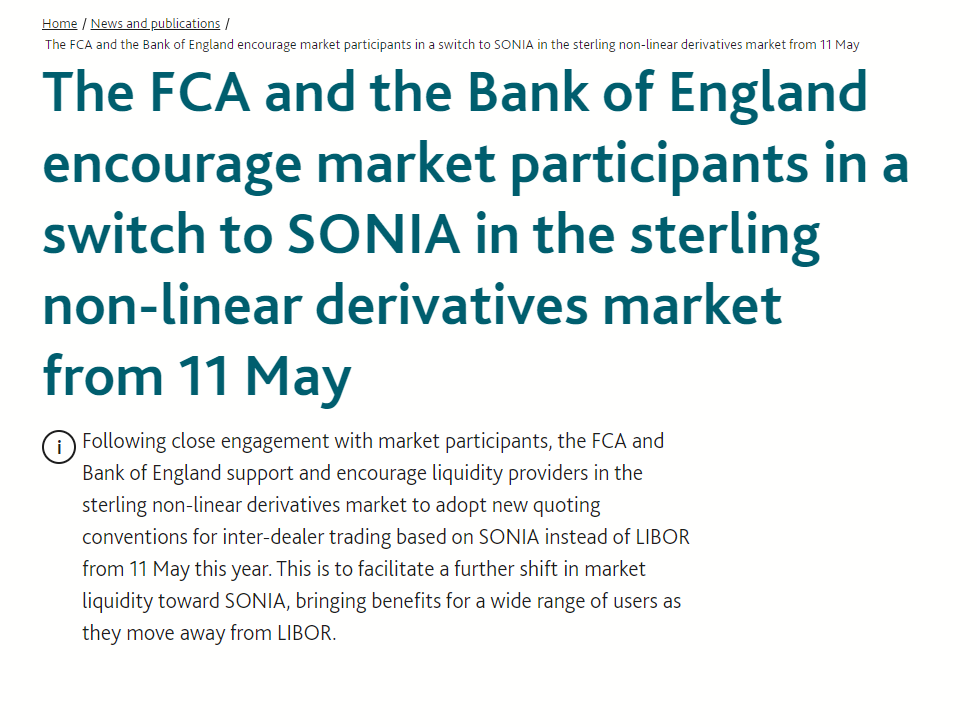

In light of which it is worth highlighting that May 11th 2021 will now be another “SONIA” day. This time for Swaptions:

What more can we say? Just that it looks like keeping an eye on the data will be more important than ever.