Roughly 3 months ago I wrote an article on MAC contracts where I gave a brief history of these standardized derivatives, preached all of the wonderful benefits of them, and discussed why the buyside should be flocking to them. I then proceeded to present data that concluded that these products just haven’t taken off.

So, has anything changed?

DATA

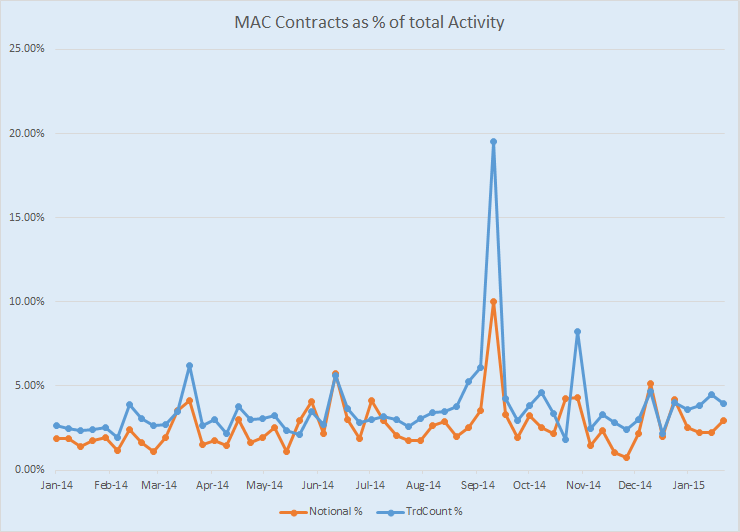

Taking the universe of USD Fixed/Float swaps, lets update the graphic showing the percent of OTC swaps that are MAC. The orange line is the percent of traded notional as MAC, the blue line the percent of trades which are MAC.

Remembering that most of the large blips are due to the quarterly roll of MAC swaps, we can see that the trend is quite flat.

In a separate context, I heard the comment today that “Flat is the new Up”. I thought that was a good way to describe quite a lot in OTC derivatives these days. Seems perhaps applicable to MAC as well. Lots of potential, but flat.

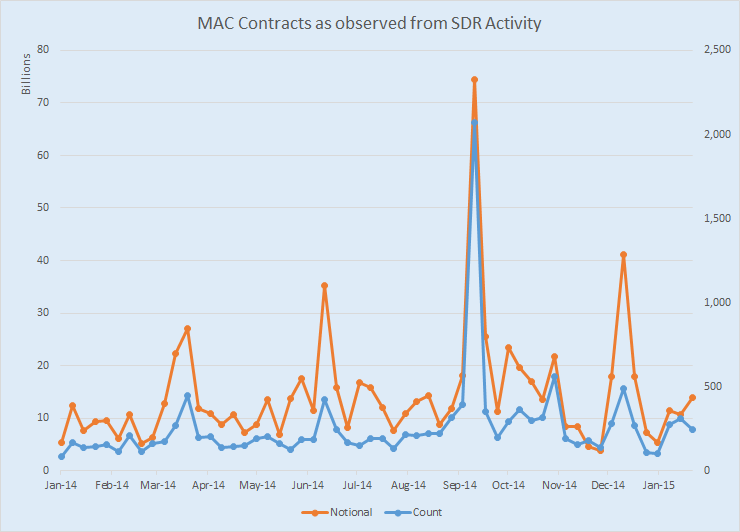

How about in notional terms:

This chart begs for a trend-line. But you can make it out – if you remove the roll periods, and look at the min and max, its flat. Of course we have the holiday period towards the end.

SEF Activity

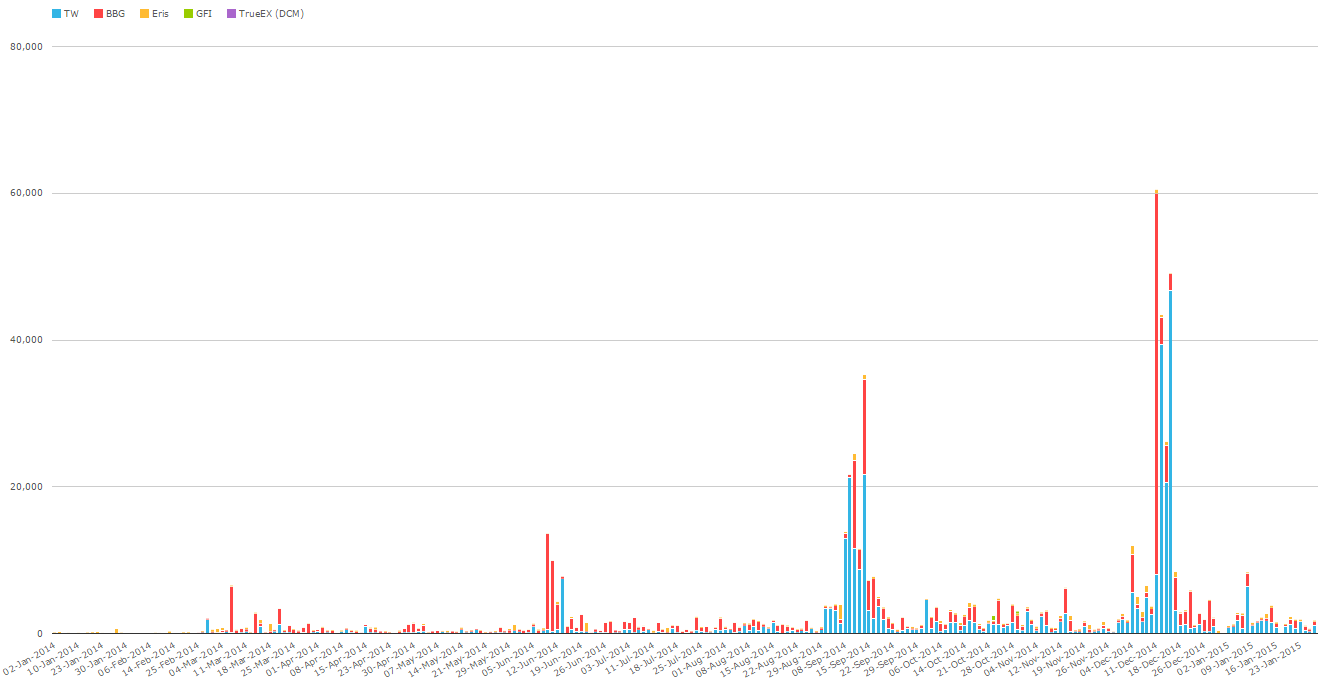

So lets see what we can see on SEFView for On-SEF MAC activity.

Slight word of caution here. This analysis varies from the SDRView analysis above in that:

- This is of course only On-SEF

- Notionals are not capped (as some MAC trades are over the cap threshold, as reported by the SDR)

- This SEF analysis includes USD (like the SDR analysis above) as well as EUR and GBP, for completeness

- I’ve chosen to include Eris Standards (MAC lookalikes) which are of course exchange traded. These are the yellow portions of the chart.

What is interesting here, is that while we have seen MAC activity generally flat, On-SEF MAC activity seems to be in growth mode, particularly the quarterly rolls.

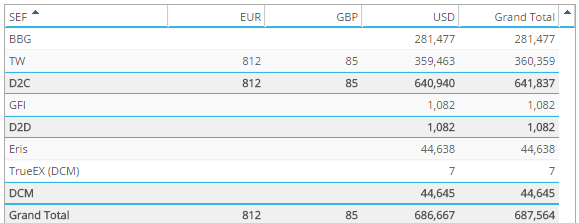

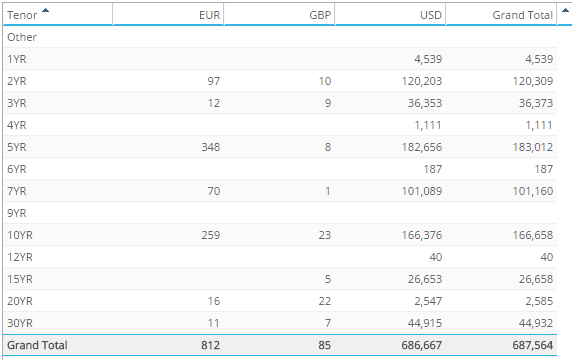

So to see which SEF’s are most active, and the significance of non-USD MAC swaps traded On-SEF, I offer you the following table:

Quite easy to conclude that USD makes up the lions share, and really only Tradeweb handling anything non-USD. We discussed GFI’s order book as upcoming in the last article, which formally launched in November, and is now in its nascent phase. Likewise TrueEX has made a showing.

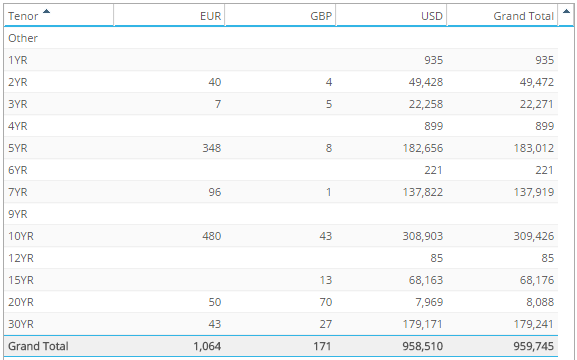

Which “contracts” are most active on SEF? I pulled the following from SEFView:

Quite a mix. What caught my eye was the 6YR. For those of you scrutinizing every number, yes, there is no such thing as a 6YR MAC swap. I quickly drilled into that one, and found a single Eris standard product, traded in October. So if anyone ever asks if all Eris standards are like MAC swaps, you can say no, Eris has an additional 6 year contract.

If we want a cleaner perspective, its best to normalize this activity around USD 5YR equivalents to get a perception of risk traded:

Here we can see risk focused on the 5, 7, 10, and 30 year. As you’d expect really.

CHANGING RATES

Given the large drop in long-dated rates over the past year, the MAC Committee earlier this week confirmed changes to the March contracts, and a similar proposal is outstanding for June contracts. If I understand the proposal correctly, for USD, it represents 100 basis point reduction in the 15 year (to 2.25%) and 125 basis points in the 20 year (also to 2.25%).

So if you’ve been trading the 3.25% flavor for the past couple months, do you now switch to the 2.25% version? I suppose the clearing house will do some coupon blending if you do? Or do you just roll out of one and into the other?

GROWTH IN 2015?

Hard to say whats next. I am still a believer.