I thought it was very interesting this week that Commissioner Giancarlo mentioned the potential emergence of HFT in the swaps trading landscape. From a quick read of his remarks, it sounds like he is not a great supporter of continuous CLOB trading as the only mode of swap execution. But what if enabling HFT in the swaps market could be shown to reduce the costs of trading? When we look at the specifics of Initial Margin for cleared swaps, we can see that this tends to be the case. We analyse the economics of three different scenarios with the aim of putting a dollar-value on intermediation (HFT) in the swaps market.

Last Time on Clarus…

Starting from the top, let’s recap my previous blog on IM. Any cleared swap has an Initial Margin associated with it, which is calculated on a portfolio basis. This “Initial” Margin amount will change throughout the life of the trade. Even in the event that swap rates never move again, it will still change as the remaining life of the swap reduces. From a pure pricing perspective of a centrally cleared swap, this poses a very interesting puzzle….

What is the cost of holding the IM for this swap?

Do we include the price of holding the IM for the entire life of the swap? Or for the average life of the swap? Or do we need to define a holding period for the swap?

Profile Pictures

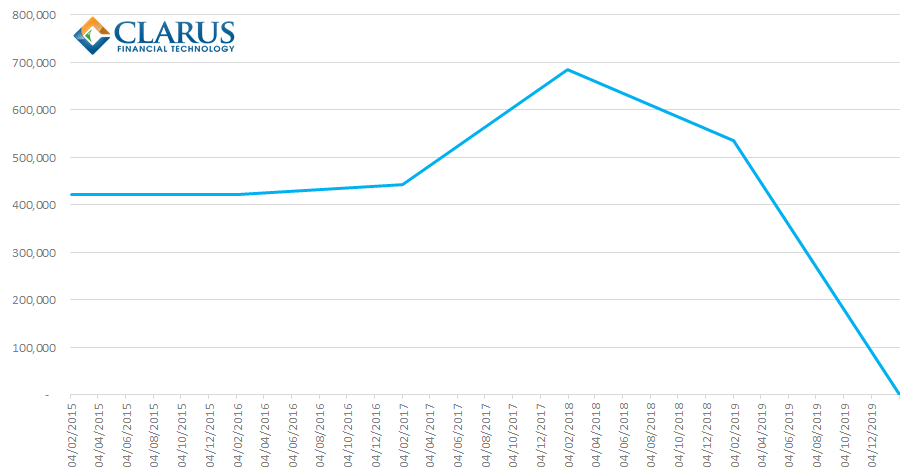

I’ll use CHARM to look at these three scenarios in turn. What CHARM allows us to do is produce a funding profile of the IM – like the below:

This is based on a forward-analysis and allows us to create an expectation of how the IM will evolve for the entire life of the swaps we are looking at. Let me spell out the key concept here:

The cost of funding is the area under this curve.

Therefore the holding period of a swap now becomes an important variable in pricing. It is this variable that differs between our three scenarios below.

From First Principles…

Our calculations under each scenario follow the same principles as we used last time for calculating the funding costs of IM. To save having to reference back, remember that the headline numbers were a cost of funding based on a financials CDS level, and a swaps delta of $10k. This allows us to quickly illustrate the pricing impact on the swaps.

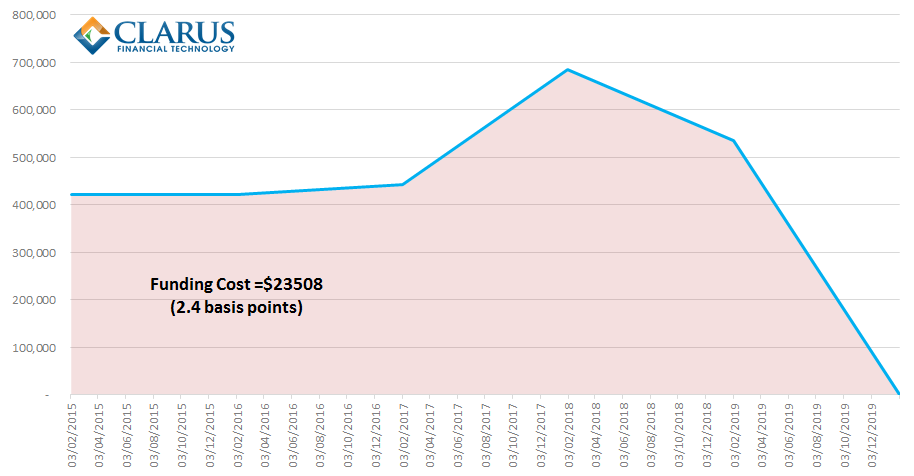

Scenario One: IM For Life!

As a trader, I am the guardian of my firm’s capital. Shareholders have entrusted me with their life savings and I must never forget that. I only deploy this capital when I am confident I can achieve the maximum return for a given level of risk. I do not make any trading decision until I have sufficient information to enable me to think “if this were to be the last trade I ever place, it will be the right trade”.

The other way of putting this approach is a little bit morbid and depressing. I assume that, immediately after I place my trade, my firm goes bust. The trading portfolio is therefore frozen at this point in time, and in order to know that I was putting my shareholder’s capital to work fairly, I must know that every trade was placed at the correct price. I therefore have to assume I hold every position until maturity.

In the case of Initial Margin, I therefore have to know the exact funding profile for the life of the trade and calculate the full funding charge. This is the minimum economic hurdle I must surpass before the trade is even profitable. In this case, that equates to 2.4bp on the swaps, or $24k in hard-cash terms – as shown in the profile below:

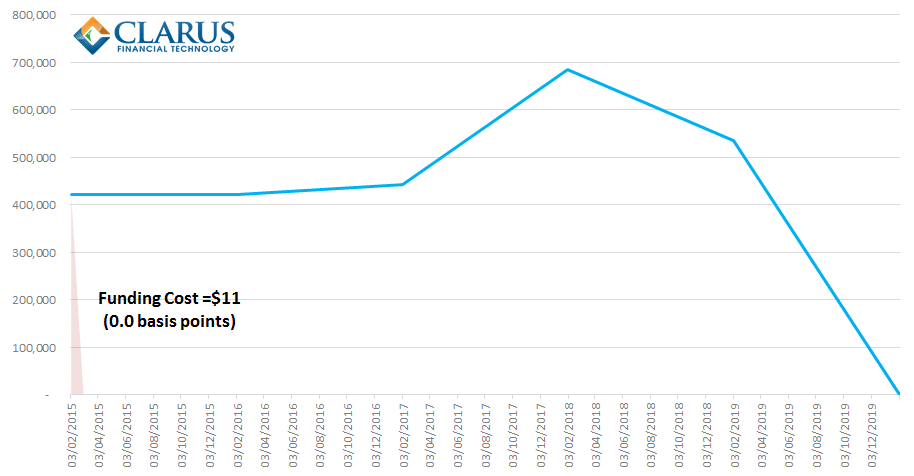

I(M) Is for Irrelevant

Flow is King! As a High Frequency Trader, market share is all I care about, and I have algorithms galore that can pick out market behaviour and glean information regarding positions of my competitors from every trade I make. I want to be the “inside price” on every SEF.

But at the end of every day, I slip on my sensible shoes and look at my swaps inventory that I’ve built up during the trading session. I figure out the minimum number of trades possible to flatten my delta, reduce my curve exposure and in-so-doing, reduce my IM requirements. I’m effectively reducing the problem of funding IM from the lifetime of the trade to the holding period of a position – which is likely to be intraday. I therefore don’t care about funding my IM – it is a drag on returns if it gets out of hand, it reduces the leverage in my overnight positions, but it doesn’t stop me locking in the bid/offer turn on the majority of my trades. As a result, with an HFT strategy, I see no significant pricing impact related to IM funding for any of my trades:

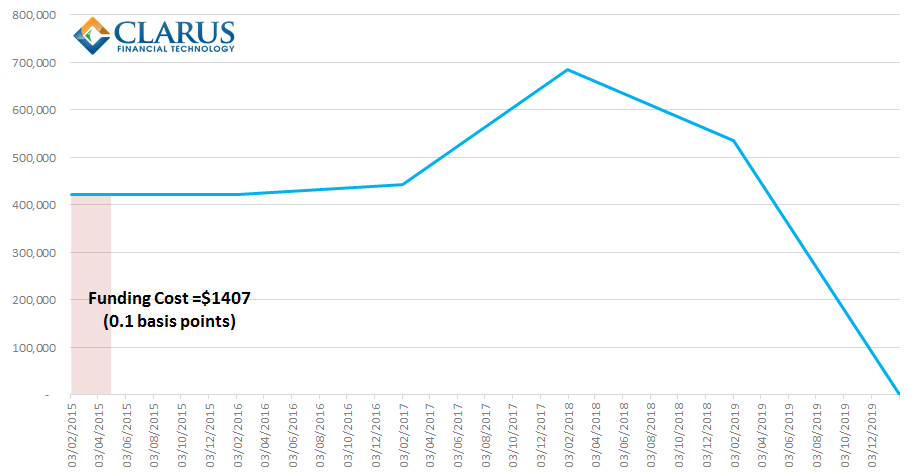

IM – what a drag!

I am a relative value investor. IM is a real drag on my returns – and reduces my leverage. I therefore need to think very carefully about what is my cheapest and most efficient way of trading. What rate of return may I earn on my IM? And most importantly – how long do I expect to keep the position? If I am intent on setting take-profit and stop-loss levels, then this must now be accompanied by a holding period. It is no good being right after 5 years – I have a rebalancing meeting every month, I have monthly targets to hit, and every day I hold the position, my effective annual return on capital is reducing. It’s good to be right, it’s best to be right quickly. I need that capital back ASAP to reinvest if the position isn’t working for me.

I therefore don’t want to hold this for more than 3 months. With that in mind, I can see that my cost of capital will be around 0.1bp for the IM:

The Vexing Questions of Convexity and CVA

To be clear, we are not talking about convexity here either. Stephen Aikin’s Convexity article highlights this. Convexity is concerned with Variation Margin (VM) when calculating pricing impacts, here we are looking solely at Initial Margin.

We can also relate this back to credit-charges in the bilateral world. Historically, you would have a credit-charge (CVA) on the way into a swap – priced as if holding it to maturity – and would receive the benefit of this CVA reduction when you come to tear it up. Does the same apply to the cost of IM-funding adjustment in the cleared (and potentially anonymous) world? I’m not so sure it does. Afterall, you cannot stop your dealer’s trading activity between trade initiation and trade tear-up. CVA is based upon single counterparty credit exposures, therefore is within your control – you know which dealers facing you are in-the-money versus out-of-the-money. With IM, it is out of your control. Come tear-up time, you have to hope that a dealer with an offsetting IM position sees your RFQ, and prices it fairly.

All-in-all, surely you would prefer to face an HFT liquidity provider at all times? These HFT intermediaries have no costs of holding IM because they trade frequently, and manage inventory intelligently. They allow IM management to become a post-trade, not a pre-trade, concern.

The Bankers…

Of course, most liquidity in the swaps market is still provided by banks. Which approach do they follow? Well, that will vary on a deal-by-deal basis and will depend heavily on the exact swap being traded – the more customised a swap, the less likely it is to be offset in a given period of time. And of course, banks value their relationships. But do they value these relationships over and above market share and the inherent economic worth of a swap? Like, $24k worth? And how will they value relationships in a world of anonymity?

About that Dollar value…

As with many of our blogs, these concepts aim to highlight how technological innovation can extract value from the changes in the swap markets. In the case of these swaps, that value could be as much as $24k, depending on your perspective.

Whatever your perspective, the point remains that given the right tools, the evolving market structures can be beneficial to everyone in the swaps market.