John Maynard Keynes said in the 1930s;

The market can stay irrational a lot longer than you can stay solvent.

Keynes

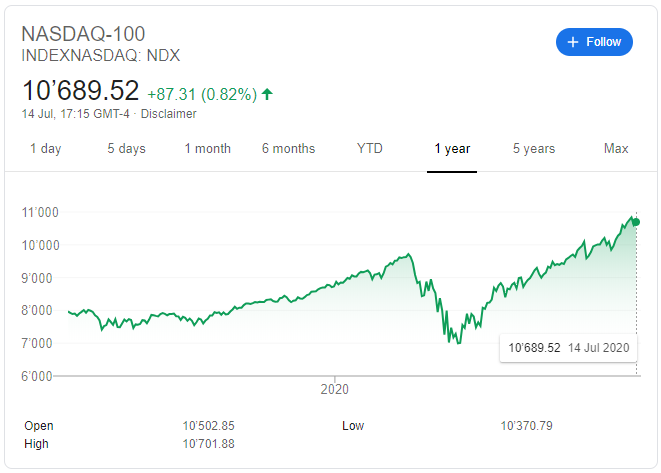

Since March 2020, the bounce-back in almost all “risky” assets since the nadir of the crisis has been breathtakingly sharp:

Motivated by Amir’s blog last week on Initial Margin, I got to wondering how solvent you would have to have been to survive the COVID-19 volatility?

Variation Margin

As Amir also covered last week, we have data on the maximum amount of Variation Margin that CCPs call during a quarter. All of this Variation Margin is in cash, therefore it is a true measure of just how solvent you would have to be to survive the crash!

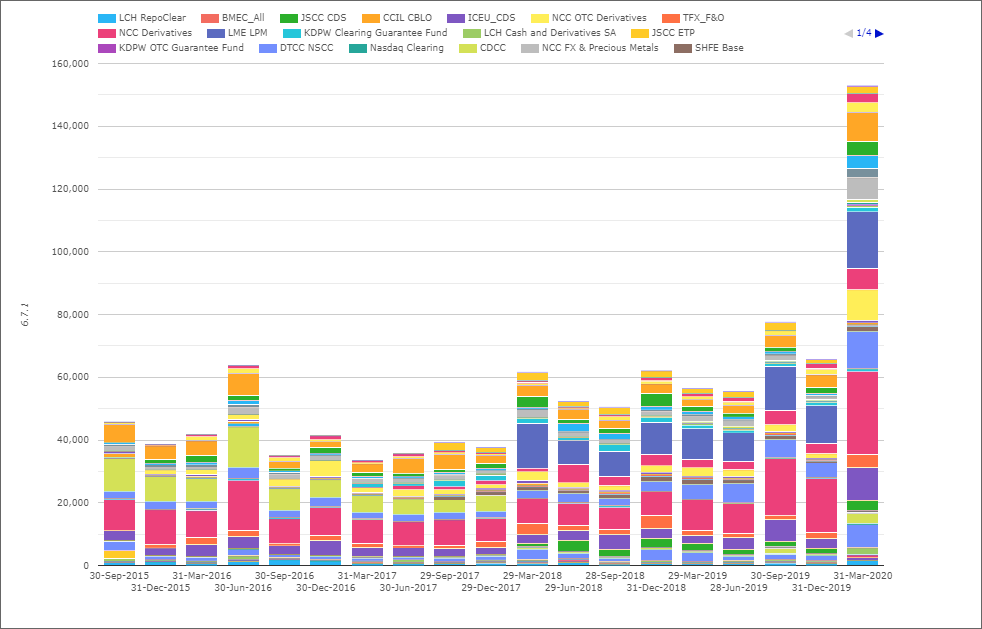

From CCPView, we can therefore take a very high level, multi-asset class view of margin calls during Q1 2020. I don’t think it is a huge stretch to state that all of the largest flows will have come during March, albeit not on the same day:

Showing;

- We have margin call history on a quarterly basis dating all the way back to 2015 (5 years and counting…).

- By my count, we now cover 59 clearing services across 37 CCPs.

- These are diverse data sources, covering all asset classes I can think of (Equities, Commodities, FX and Rates across Futures, Options, OTC, Derivatives and Cash products).

- Whilst the chart isn’t representative of a single day, it does show the uniquely global impact of the COVID-19 crisis.

- I hope it is clear that we cannot say $150bn was the maximum margin call. It is tempting, but that is not the case.

- It is also not fair to say that Max VM has quadrupled since 2015. We have added more and more CCPs to our data sample over time, and not all have provided a complete history of disclosures.

- Therefore please just take this chart as a good illustration of the sheer size and scope of margin calls, but don’t rely on absolute numbers.

It is also worth noting at this juncture that some of this data is difficult to work with. This is because some CCPs provide both service-level and CCP-level disclosures. I’ve done my best to remove any double-counting.

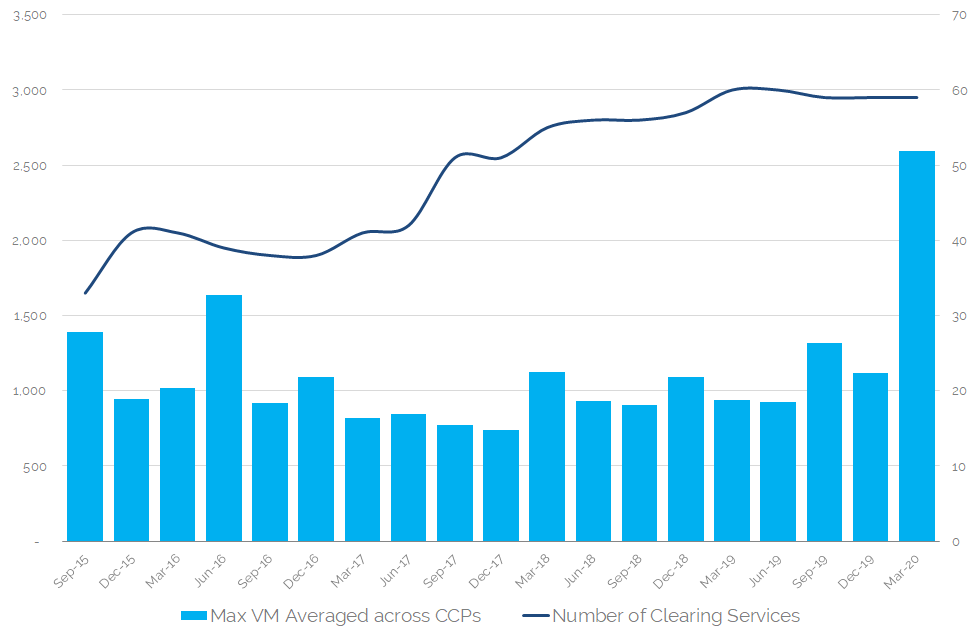

Peak VM Per CCP as an Average

With that stated, I therefore looked at how the maximum VM has evolved as an average per CCP. I believe this is the best illustration of the impact on margin calls of the COVID-19 crisis:

Showing;

- The average maximum VM call (“Peak VM”) per CCP per quarter in our sample.

- The evolution of this time-series allows us to quantify the impact of the COVID-19 crisis.

- The outright value of $2.5bn in March 2020 may be pretty irrelevant (we’d be interested to hear reader’s thoughts on that figure?).

- March 2020 saw 1.6 times more margin called than the previous peak quarter.

- The previous peak was June 2016, no doubt from the Brexit-related volatility.

- March 2020 saw 2.3 times the peak margin called compared to the prior quarter.

- The chart also shows that we nearly doubled the number of CCPs covered since 2015.

Uncleared Margin Calls

We therefore know that for each CCP you clear at, it is fairly likely that your VM requirements at the peak of the crisis went up by around 2.3 times quarter-on-quarter during 2020.

That is a very useful stress-scenario to dictate your liquidity needs in the future.

We will of course re-calibrate with the June 2020 disclosures (out in September/October) to see how quickly this reversed course.

But the huge missing piece of the puzzle is what happened in Uncleared Markets to margin calls? Cross Currency swaps, for example, remain uncleared and were at the centre of the Central Bank responses to the crisis. What were the margin calls related to those products? What about Swaptions? And FX Options?

It remains a large failing in the transparency regime. We have no data sources regarding margin calls in Uncleared Markets. Why not? We believe these should be published somewhere in a timely manner. A central resource would be ideal, or as part of individual dealer reporting requirements (Basel III disclosures maybe?).

In Summary

- CCPs provide transparency surrounding maximum variation margin called during a quarter.

- We estimate that the maximum margin calls were 2.3 times as large during the COVID-19 quarter as the previous quarter.

- These margin calls were 1.6 times larger then we have seen before.

- The previous peak margin calls were as a result of Brexit.