A new study funded by ISDA on Margin Requirements for Non-cleared Derivatives authored by Professor Rama Cont of Imperial College London, was the topic of much comment and debate at the ISDA AGM. It was also covered extensively in the press, see CFTC, Treasury officials boost ISDA push for IM revamp and ISDA faces member backlash on margin lobbying, on Risk.net (subs required).

Lets take a look at what the study proposes.

Background

Starting with a quote from the ISDA Press release, “The framework for calculating initial margin requirements has been imported from existing practices for cleared derivatives, except that regulators have increased the margin period of risk, presumably because there is a perception that non-cleared derivatives are intrinsically harder to close out or unwind if one counterparty defaults. Our study questions the rationale for this approach, and advocates an alternative that takes into account the default management process, as well as the size and complexity of trades”, said Professor Cont.

Study Overview

The study argues that the 10-day liquidation horizon or margin period of risk (MPOR) has little basis, beyond the fact that it is greater than the 3 to 5 days used for cleared OTC contracts and the same as the FRTB guidelines for capital requirements.

It then makes two proposals:

- That the liquidation horizon should depend on the size of the position relative to the market depth of the assets, which is achieved by specifying a minimum liquidation horizon and scaling this horizon linearly with position size.

- IM should not be based on the exposure of the initial position over the entire liquidation horizon, but on the exposure over the initial period required to set-up the hedges, plus the exposure of the hedged position over the remainder of the liquidation period.

A size-dependant liquidation horizon penalises large concentrated positions without requiring a liquidity add-on, as used by CCPs, while the second proposal reflects actual market practice, where a firm would hedge market risk as quickly as possible with liquid hedges and only the residual unhedged basis would remain until liquidation.

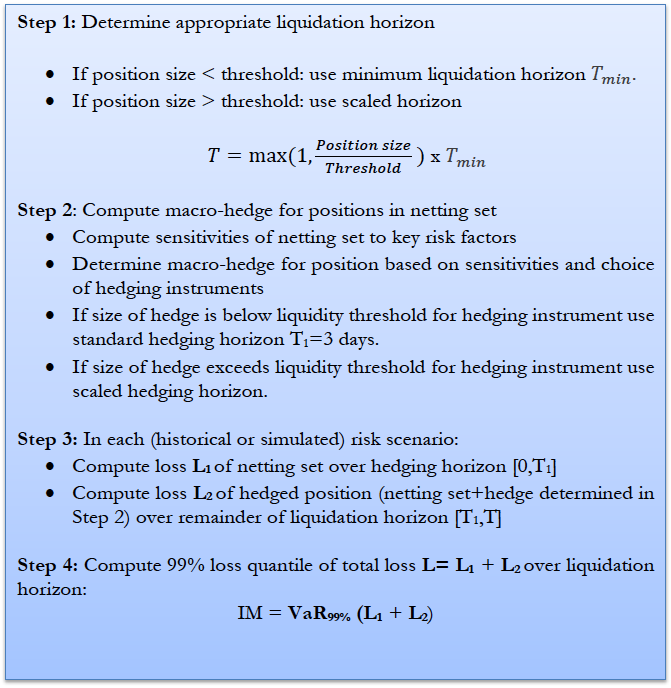

Four Step Approach

The study proposes a four step approach ro the margin calculation:

- Determine the appropriate liquidation horizon

- Compute macro-hedge for positions in a netting set

- In each scenario compute loss over hedging horizon and loss over remaining horizon

- Compute 99% loss quantile of total loss

There are worked examples in the study for single name CDS contracts, which on default being declared are hedged with CDS Index contracts and then liquidated.

These assume 3-days for the hedging period and a minimum 5-day liquidation horizon, which is scaled for larger positions. This scaling results in IM increasing in proportion to position size by a factor of N * sqrt(N) or N to the power of 3/2.

While there is no categorical statement in the study, it does propose a 5-day minimum for liquidation horizon (to be in line with cleared OTC derivatives) and a 3-day hedging period.

And that the actual liquidation horizon should be determined by reference to the daily trading volume or the typical trade size.

So for example if average daily volume for a product is estimated to be $200 million notional and our position is $10 million, so 5% of daily volume, it is safe to assume that it can be un-wound in one day. However if our position is $300 million, we could assume unwinding at 10% of daily volume would avoid market disruption, leading to a 15-day liquidation horizon.

Study Conclusion

The study concludes that a fixed liquidation horizon does not provide a good basis for calculating IM for non-cleared derivatives, in particular it leads to an overestimation of margin for small portfolios and an underestimation for large concentrated portfolios.

It argues that making the liquidation horizon proportional to the size of the position relative to market depth and splitting this horizon into the time to implement hedges and the residual risk period better reflects reality and will result in more realistic margins.

My Thoughts

Compelling arguments indeed, well argued and well presented.

Yet somehow I find myself disagreeing that the proposals will be useful in practice.

The study is certainly interesting and worthwhile, indeed more research is welcome. It would be good to see more on liquidity thresholds, liquidity add-on determination by CCPs, market practice in managing exposures in the event of default, the timing of cashflows that may exceed daily market volatility by multiples (Andersen et al, 2017) and more.

But the question is do the proposals in this study merit a change to regulatory guidelines?

And should ISDA SIMM then be modified to take account of these?

I would answer no to both.

My reasoning being that:

- making liquidity horizon rely heavily on daily trading volume, gives too much credibility to the quality of trading volume metrics for OTC derivatives trading, a market which is generally episodic or periodic in nature, with high variability in volume and a lack of comprehensive granular data

- splitting the liquidity horizon into a shorter hedging period and a residual liquidation period, introduces both complexity and subjectivity, which could result in a variation of approaches by participants and possibly a material understatement of margin

- while the regulatory guidelines specify 10-day (and 99% confidence level calibrated to include a stressed market period) this does not necessarily result in a significantly higher margin than that determined by CCPs for cleared derivatives and generally not the 40% higher (sqrt(10/5) used as a common approximation

Lets take each of these in turn, in reverse order.

Cleared Margin

The majority of CCPs that clear interest rate swaps use a 99.7% confidence level and either a 5-day liquidation horizon for clearing members (house) or a 7-day liquidation horizon for clients.

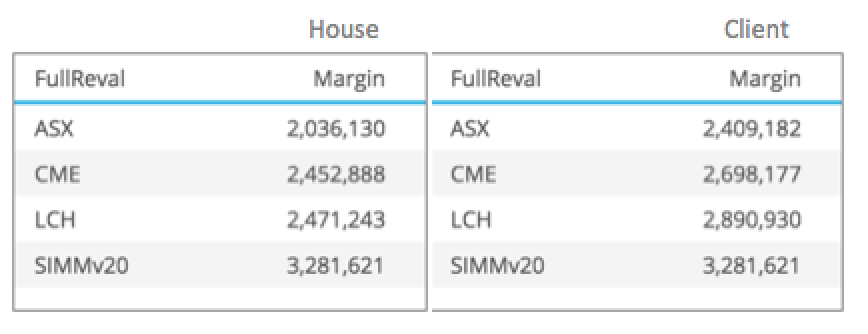

Using CHARM we can compare CCP margin for a cleared product with the uncleared margin from ISDA SIMM.

Lets do this for an AUD IRS 100m 10Y received fixed trade.

Showing that:

- SIMM is 33%, 34% and 60% higher than LCH, CME and ASX respectively for house

- SIMM is 13%, 21% and 36% higher than LCH, CME and ASX respectively for client

Further if we look at price moves in the USD Swap market over the start of May to mid June 2018 period (Italian political crises), we see the following for the 10Y Swap rate:

- Largest 1-day move up was +11bps and move down was -9 bps

- Largest 5-day move up was +18bps and move down was -25 bps

- Largest 10-day move up was +17bps and move down was -25 bps

- (the latter two are calculated as overlapping return periods)

Meaning that 99% confidence level moves for this small set of observations are very similar for both 5-day and 10-day and would result in similar margin.

The point I am making here is that isolating the fixed liquidation horizon of 10-day compared to 5-day as a cause of the overestimation of margin for small portfolios is not necessarily correct. Other factors such as choice of confidence level, the calibration period and back-testing of margin results are as important.

Splitting liquidity horizon

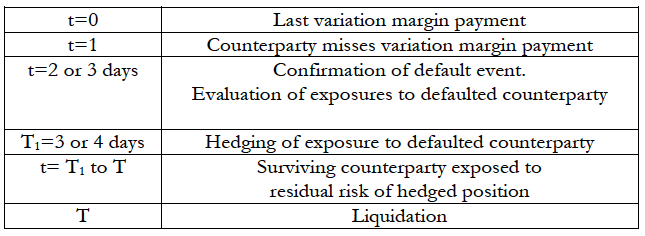

Next lets consider the proposal for a shorter period of 3 days of exposure until the main risk are hedged with liquid hedges and residual risk for the remainder of the liquidation period.

On page 13 of the study a rationale is offered for this along the lines of that a CCP has to hold an auction and liquidate the whole position for a defaulting member (hence the fixed 5-day horizon) while the situation is different in the bilateral world, where the surviving counterparty will not necessarily liquidate but will first hedge against further market moves using liquid market instruments and manage the residual risk until liquidation or replacement.

My experience does not accord with this, as LCH SwapClear and other CCPs also follow the practice of first hedging major exposures and then auctioning the defaulting portfolio including hedges.

So this is not a valid rationale for introducing such a concept.

Granted it is closer to what happens in reality, so I would expect has been considered by some CCPs. However the added complexity of such an approach does not seem to me to lead to a materially superior result.

In-fact it could lead to lower margins for uncleared risk than equivalent cleared risk.

A result that would not be welcome to regulators and would be manifestly problematic given that cleared products have a CCP that determines settlement prices, while for bilateral exposures, the surviving party would need to find consensus on the valuation with a new counterparty(s).

Daily trading volume

Those of you who follow the Clarus Blog, know that we regularly write about OTC Derivatives volumes and collect as much data as we can on these markets. (See Data Products).

However for non-cleared derivatives it remains difficult to get comprehensive and granular data to allow the determination of market depth and liquidity (see MiFID II).

The nature of some products, a low number of trades, sometimes not every day with episodic trading, introduces further subjectivity.

Which leads to the question as to who will determine the liquidity horizon to be used?

- A regulator?

- A utility?

- ISDA?

- Consensus between the parties?

And even with this we may not end up with a materially better margin number.

Too high or too low?

Which leads to the question, what is the lesser of two evils?

A margin number that is too high or too low?

Most people would err on the too high side.

On balance that is better for systemic risk.

Of-course we only want it to be little high not too high.

CCPs have 20+ years experience of margin, using 3, 5, or 7 days.

A 10-day liquidation horizon does not make it too high.

Large concentrated portfolios definitely need to have higher margin.

CCPs do this with liquidity add-ons.

These methodologies are not always transparent or capable of replication.

An art as much as a science?

Certainly more research in these would be welcome.

Final Thoughts

Phase 3 firms will implement Uncleared Margin in Sep 2018.

Phase 4 in Sep 2019 and the remaining firms in Sep 2020.

Industry efforts are focused on successful adoption.

ISDA SIMM for most cases, perhaps Schedule for some.

Methodology changes should be not be introduced.

Until all firms are live and after some time in operation.

Backtesting and calibration of SIMM are the way to go to tune results.