- MAS is playing catch up and proposing to mandate trading of USD, GBP and EUR fixed float swap trades in organised markets, aligning themselves with the EU and US regulators.

- The proposed tenors covered are the most liquid (under 10Ys) on the respective currencies curve.

- However no JPY, AUD or SGD trading mandate yet.

Proposed Mandate

On 20th Feb the Monetary Authority of Singapore (MAS) issued a consultation paper on the mandatory trading of OTC derivatives contracts in Singapore. A trade reporting mandate has been in place in Singapore since 2013 and a proposed clearing mandate for USD and SGD has been under discussion for since 2015, so with this proposed trading mandate, MAS is playing catch up to the EU and US regulators.

The consultation paper has two parts. The first covers a trading mandate and the second part ask’s for feedback on the inclusion of EUR and GBP into Singapore’s proposed clearing mandate.

The consultation paper focuses on Fixed Float IRS Swap products and proposes a trading mandate for spot starting and IMM USD, EUR and GBP trades. MAS states at the outset that the goal of the paper is to focus on global OTC derivatives as in their words products with limited domestic or regional liquidity pool may not be appropriate to be subject to global trading obligations. JPY and SGD are therefore not included.

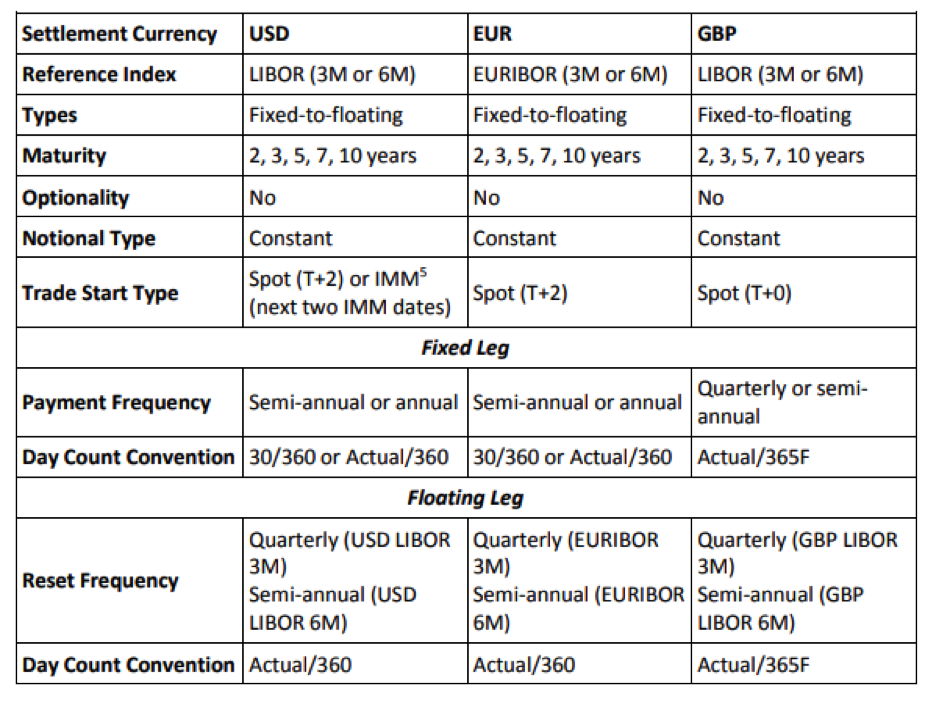

The following table outlines the scope of the proposed mandate.

(The MAS consultation document is available here).

The Currencies

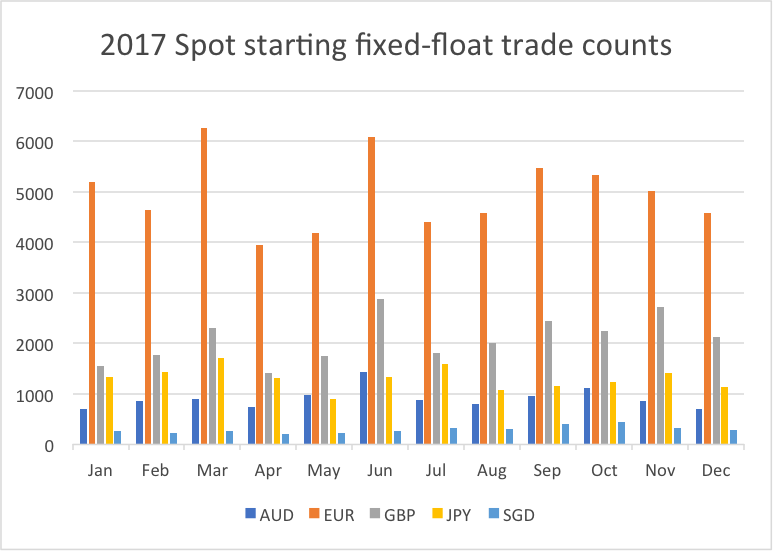

The proposed currencies are very similar to the MIFID list of currencies subject to the trading obligation. In the past we at Clarus have questioned why JPY was not included in the MIFID trade obligations. As JPY appeared to be of similar size to the GBP market, however when we look at the trade counts 2017 (taken from the US SDR) you can see JPY (and the AUD/SGD) trade counts are significantly lower than the GBP trade counts.

The Tenors

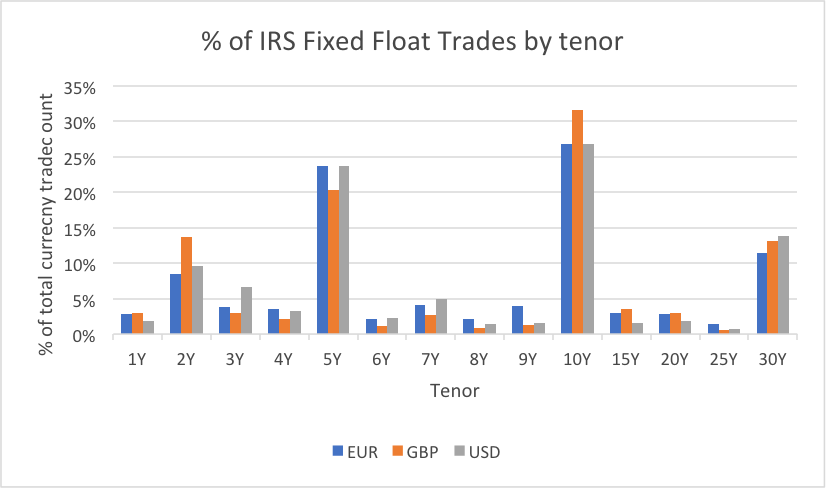

MAS does not reveal what selection criteria have been used to determine which products are to be subject to the trading mandate, other than referring to some historical surveys that have been conducted. The consultation paper does propose the tenor of trades to be included in the trading mandate. If we look at the US SDR data, the broad break out of the tenors of USD, GBP and EUR Fixed/Float IRS Trades are as follows.

When determining what tenors to mandate, MAS have ensured the most liquid tenors (2Y,3Y,4Y,5Y, 7Y and 10Y) are covered, but have excluded the 4Y,6Y, 8Y and 9Y tenors that were required under MIFID.

MAS has not described a mechanism as to how changes to the mandated tenors/currencies will be made. I assume that they will just update the mandate as required? If you are interested in the challenges that the European and US regulators had determining what to cover, see our blog from last year on the “data driven analytic approach” that the EMIR regulation took. Do also look at our blog on the broken MAT process that shows some of the challenges establishing the MAT process in the US.

New Currencies for Clearing

In the second part of consultation paper MAS proposes to include the GBP and EUR swaps in their proposed clearing mandate. Makes sense if they are to be included in the trading mandate.