The Default at Nasdaq Clearing has re-invigorated industry discussions on default management practices and we are now seeing the fruits of these labours. For example CCP12 recently published a CCP Best Practices Paper and LCH published Best Practices in CCP Risk Management.

Today I will look at the BIS CPMI-IOSCO “Discussion paper on central counterparty default management auctions” (available here). At twenty-one pages it is a short enough read, but one that requires dedicated concentration to get thru, without suddenly remembering something you simply must do instead…

So, in no particular order, here are the highlights that I found interesting.

Client participation

Chapter 6 of the paper discusses client participation in a default auction, which sounds a radical idea as only clearing members mutualize the losses of a CCP and are obliged to participate in a default auction, which sounds in many ways more like a duty you have to do but would rather not.

The paper lists the following benefits:

- For CCPs, an increase in the number of participants in the auction may increase the competitiveness (better price), the probability of auction success (super important) and distribute the defaulting portfolio risk more broadly (generally good).

- For Clients, the incentive may be financial gain (always compelling) or to avoid negative outcomes from a failed auction (good and a public good to boot).

Considerations for client participation mentioned are:

- As a clearing member guarantees a client’s trades, the member also needs to ensure it is comfortable with it’s client winning the auction and the CCP generally requires explicit consent from the member, who in turn may require an explicit agreement with the client to cover the risk as well as additional margin.

- To avoid giving clients a “free look” at the defaulters position without a serious bid, a CCP may require a client to contribute an established amount that the CCP can use in a manner similar to a default fund contribution (interesting, I wonder if this has happened in practice).

Legal readiness, Operational readiness and Information leakage are also discussed and are each important.

Default across multiple CCPs

This has garnered more attention and in recent years we have seen more co-ordination between CCPs, for instance on running default exercises concurrently. The concern is that in a multi-CCP default there could be:

- resource bottlenecks in the ability of members to meet CCP requests to convene Default Management Gorups (DMGs) in order to advise, analyse and hedge the defaulting portfolio

- potential market impact of the hedging, auction and liquidation of collateral

- operational challenges including different jurisdictions

Conducting concurrent default management exercises are a way to mitigate the above.

The flip side being that such exercises are very resource intensive on members. Software automation helps to a degree but the human expertise element remains a constraint.

Practically this means that the context narrative for a default exercise should change, so one year it could be a large member with many CCP memberships defaulting and require co-ordination between CCPs in the same product class and at other times it could be a small regional member default simulation only for that CCP.

Auction Design

We are all familiar with auctions in some way; either with the classic image of a hammer falling as a bidder pays the highest price to acquire a work of art (e.g.Jeff Koons “Rabbit”) or the auction that Google runs each time you use search to serve up Ads (see What is Google Adwords).

The paper describes considerations in the auction design for:

- Preparation, choosing to auction the whole portfolio or splitting into smaller segments (e.g. by currency) and deciding to enter into hedges before auctioning to increase the likelihood of bids and a more successful auction.

- Auction Format, the two most established being single unit pay your price, the winner is the one who pays the highest acceptable price and modified dutch,each participant bids for a percentage of the portfolio and winners are defined on a cumulative basis from highest to lowest with the price applied to all being the lowest accepted price.

- Requirement or Incentives, some CCP rule books require mandatory participation with fines or disciplinary actions on firms that do not adhere to bidding obligations, while incentives include “juniorisation” of default fund contributions of those members that do not bid or provide less competitive bids.

- Flexibility and Predictability, this is one that comes up on conference panels from CCPs. Rigidly pre-determined auction elements are well and good but CCP’s need flexibility to respond to specific conditions of the default (e.g. adjusting auction format, participation and mechanisms to incentivise bidding).

Operational Considerations

This section discusses steps to take during business as usual (BAU) to prepare, onboarding auction participants in advance, requiring them to take part in regular testing exercises and training.

Communication

Which leads to the importance of effective communication both before, during and after an auction. Communicating the actual portfolio aka “auction file” or “auction pack” is essential and while these differ between CCPs, they generally include:

- full trade or position level information of instruments (contracts)

- information needed to price the instruments (curves etc.)

- margin requirements that the winning bidder must meet (either estimated by the CCP or with enough information that margin simulation tools can estimate this)

Testing

Testing may be operationally focused or an end-to-end default management exercise, the latter requiring a hypothetical event, market narrative and simulating the entire process, so DMG convening at a CCP, all the way to selecting bids and notifying participants of the outcome.

As with all testing, a test plan with documentation communicates to participants and regular test exercises (semi-annual or annual) is important.

There is more content in the paper, but not a single chart or image and I am conscious that so far my blog is all words too! Time to remedy that.

DMP Firedrills

At Clarus we help customers with their default management obligations, both regular firedrill tests and in the event of an actual default. We do this specifically for Swaps clearing and currently for LCH, CME and ASX clearing members.

Swap auction packs need complete trade economics information, which unlike Futures and Options are non-trivial in their format (i.e much more verbose than contract, delivery month and position). CCPs generally provide these packs to their members in either proprietary formats or in FpML (an ISDA standard).

In CHARM, a user can simple drag & drop the Auction pack folder onto the dialog to create the portfolio in seconds, even one with tens of thousands of swaps.

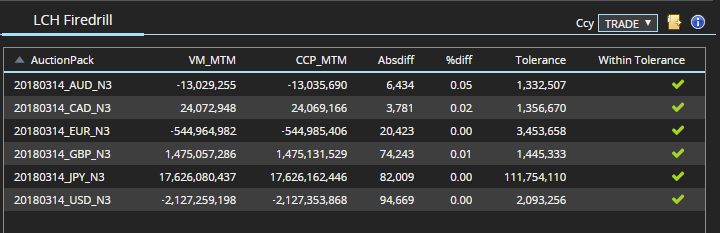

To be sure that created trades are correct, either all trade cashflows need to reconciled with a report provided by the CCP or even better using the same market data curves used by the CCP calculate a mark-to-market and check it is within an acceptable tolerance of the CCP valuation.

The CHARM screen below shows this mtm comparison, with each of the currency auction packs well within an acceptable tolerance amount.

All within a few minutes.

We know that members using some vendor systems can take many hours or days to get to this point! (Not such a big deal when it is a drill and time and resources are readily available, but a critical issue in a real default situation, when time is of the essence and there may be many currency packs to bid on).

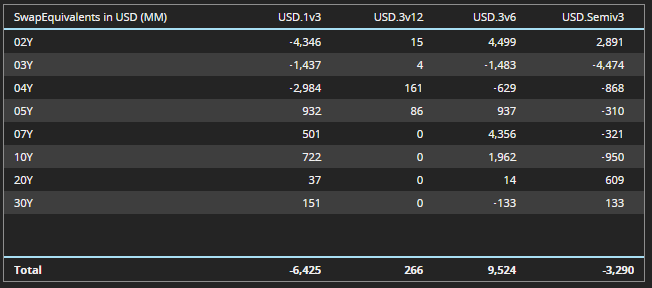

Next the member will need to:

- assess the risk in the pack (outright, tenor, basis) and decide if they are comfortable taking this on

- or if not, work out hedges needed to neutralise and the associated cost of entering into these hedges

- assess the increase in margin required by the CCP, as well as any incremental operational and infrastructure cost, should the member ended up wining the bid

- value each auction pack on the specific day and time window requested by the CCP, using the members own view of the market at that time (upload own curves)

- submit a bid to the CCP for each auction pack, inclusive of hedging and any other costs

The CHARM hedging view is shown below:

You get the point.

Fast, efficient, comprehensive functionality for default management auctions of swap portfolios.

Summary

Valuation and hedging of large swaps portfolios is a non-trivial task and one that is crucial in a default management auction.

Default management tests aka Firedrills are important in testing member readiness.

As firms respond to the questions in the BIS discussion paper, I expect we will see more focus on some of the points raised e.g. client participation, multi-CCP defaults, auction design, operational readiness and improved end-to-end testing.

At Clarus we help our customers adopt best practices in default management.

If you are interested in learning more, please reach out.