Credit Support Annexes used to be the dullest of the dull. A “back-office”, operational necessity that helped reduce counterparty exposures.

Now, they are intrinsic to the functioning of modern day derivatives markets and have blossomed in both number and potential complexity as a result of the Uncleared Margin Rules. If you don’t have a CSA, you probably aren’t trading derivatives in 2024.

I have written about CSAs before – give it a read:

CSA = Margin Agreement

From a pricing perspective, I consider CSA and Variation Margin as interchangeable terms. And the details of these agreements are really important. Simply stated:

The type of margin that you exchange periodically to collateralise your mark-to-market moves on your derivatives portfolio will define the discounting of your cashflows and hence the valuation of the portfolio.

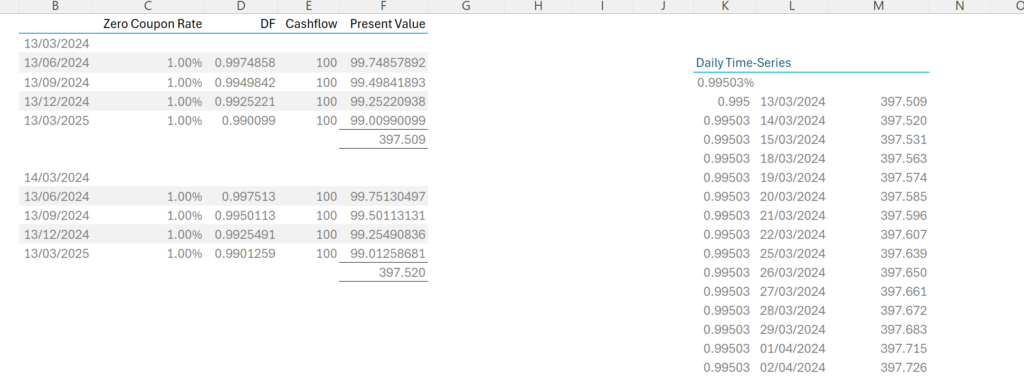

Why is this? Consider a stream of quarterly $100 cash-flows going out for one year:

- If the one year interest rate is zero (which was true not-so-long-ago!), the present value of these cashflows would be $400.

- If you collateralise these cashflows daily, the out-of-the-money counterparty would have to transfer to the in-the-money counterparty a value equivalent to $400.

- If this were at a Clearing House, this would mean “posting” $400 in USD cash. In return for that, the poster would receive daily SOFR interest (i.e. $400 * 1/365 * SOFR fixing).

- If the one year interest rate then moved up in a parallel fashion to 1%, and the SOFR fixing moved up in line:

- The poster would now transfer less than $400 – say $397.51 if all cashflows are discounted at 1%.

- With a completely flat curve, SOFR should be fixing at 0.99503% (the continuously compounded equivalent of 1% annual interest rates (LN((1+Rate)) in Excel).

- The $397.51 would earn SOFR at 0.99503% on the first day.

- The NPV of $397.51 moves to $397.52 on the following day. This $397.52 will then earn SOFR at 0.99503%.

- This means there is no “riskless” arbitrage here. The market participant who receives the $397.51 on day one can only lend it in the SOFR market overnight. The following day, they must pay the counterparty overnight interest on the collateral that they have posted to them – which is equivalent to the SOFR interest they would have earned by lending the mark to market amount.

- Given that the cashflows will be one day nearer to fruition, the change in NPV of the contract will therefore exactly offset the interest owed, and hence no further cashflow would actually take place between the two counterparties.

- It is a fun exercise to get grads and summer interns to prove this on pricing spreadsheets! 😛

Pricing Complexity

The above example is highly stylised, but is how your “CSA” with a Clearing House works in Swaps. The discount rate is equal to the overnight interest (“Price Alignment Interest” or PAI) that Clearing Houses calculate.

But this is not how bilateral markets work:

- On a bilateral CSA, counterparties post a single type of collateral each day to collateralise mark-to-market moves across a whole range of underlying assets, currencies, exposures; you name it from oil, gas, metals contracts to interest rates, credit and FX.

- You might be collateralising USD mark-to-market moves with EUR cash.

- Or collateralising oil mark-to-market moves with UK government bonds (GBP Gilts).

Thinking of a Rates portfolio, where dealer hedges are typically subject to Clearing Mandates, a dealer will be receiving/paying collateral on their bilateral trades in a whole host of currencies/securities (depending on the end client) but always posting cash in the underlying currency at the CCP.

This means that dealers carry funding positions related to their CSAs. A USD swap collateralised in EUR effectively carries a EURUSD XCCY basis position (€STR vs SOFR) for the life of the trade because there will always be a balance of EUR collateral (client trade) versus USD collateral (at the CCP for the hedge trade).

Therefore, the CSA becomes the determining factor in how a swap is discounted and valued. A USD swap collateralised in EUR is discounted with the EURUSD XCCY swap curve, not just the USD SOFR curve.

In each case, it is the collateral that you receive that defines the overnight interest rate that you can earn on that collateral: “If I take the collateral that I receive, what can I do, risk free, to earn a rate of interest?“

(This XCCY exposure is evident even absent the hedges. Consider the accounting for a single trade. You have the mark-to-market value of the underlying derivative versus the mark to market value of the collateral being carried on your balance sheet. One is an asset, earning interest, the other is a liability, on which you must pay interest – and they could be in different currencies).

Dirty CSAs

This is why we have seen a new phrase enter the trading Lexicon – “dirty CSAs”. These largely describe CSAs that are posting non-cash. What to remember:

- The CSA is essentially a derivative that sits atop of your portfolio.

- It is customisable and subject to bilateral negotiation.

- Traditionally, these negotiations were undertaken from an operational viewpoint – which collateral is “easy” for the client to post.

- The eligible collateral that is being posted also impacts the valuation (and risk profile) of the underlying derivatives portfolio.

If clients naturally long e.g. Gilts (UK pension funds), then if they choose to post Gilts as Variation Margin on their derivatives, they have to be aware that they are essentially outsourcing a daily repo trade to their bank counterparty. That term repo will vary in size as the mark-to-market of the derivatives portfolio changes. A bank is not going to do that for free – they will charge a spread for it.

Clients must decide, as we witnessed in reaction to the Gilt crisis, whether the liquidity risk in stressed markets is greater than the cost of the risks that a bank counterparty will have to run every single day.

https://www.risk.net/derivatives/7956945/uk-pension-fund-buyouts-frustrated-by-dirty-csas

One CSA to Rule Them All

Finally, I wrote in the VM Big Bang blog that running a single CSA is beneficial from a funding perspective. It is also true that SACCR exposures are mostly calculated at the CSA level – a so-called “netting set”. From a SACCR perspective, the cleanest CSAs are those that:

- Settle daily.

- Have a zero threshold (to reduce the potential build-up of uncollateralised exposures).

- Cover as much of your derivatives portfolio as possible, increasing netting opportunities.

Directional clients may not immediately appreciate the benefits of netting (“We are always the same way”), but it is beneficial to net your mark-to-markets (winners versus losers) to reduce the Replacement Costs under SACCR (subject to a 140% weighting).

Bringing your mark-to-market back to par reduces the hedging costs that a dealer carries from managing the cross-collateralisation inherent within your CSAs.

In Summary

- The importance of your CSA terms should not be understated.

- The type of collateral you post will define the valuation of your entire derivatives portfolio.

- These are complex risks for dealer banks to manage, and hence carry associated charges.

- It is generally beneficial to run a single netting set with each dealer.