Following on from my article on MiFID II and Transparency for Swaps, I wanted to look at Fixed Income Securities and specifically Bonds.

Background

The ESMA Final Report deals with Draft Regulatory Technical Standards (RTS) of which there are 28 and describes the consultation feedback received, the rationale behind ESMA’s proposals and details each RTS.

While MiFID II was scheduled to apply from January 3, 2017, there has been much press that the deadline would need to be moved.

Today the European Commission announced that the deadline has been moved forward to Jan. 3, 2018, to “take account of exceptional technical implementation challenges faced by regulators and market participants,” the Brussels-based commission said in a statement. The delay is “strictly limited” to allowing technical work to be finished. (See Bloomberg).

RTS 2 – Transparency requirements in respect of Bonds

RTS 2 has requirements on transparency to ensure that investors are informed as to the true level of actual and potential transactions, irrespective of whether the transactions take place on Regulated Markets (RMs), Multi-lateral Trading facilities (MTFs), Organised Trading Facilities (OTFs), Systemic Internalisers (SIs) or outside these facilities.

This transparency is meant to establish a level playing field between trading venues so that price discovery of a particular financial instrument is not impaired by fragmentation on liquidity.

Meaning that there are both pre-trade and post trade transparency requirements.

Post-Trade transparency

Trading Venues and Investment firms trading outside venues are required to make public each transaction in as close to real-time as possible and in any case within a maximum 15 minutes of execution, which drops to 5 minutes after Jan 1, 2020.

Meaning that most trades will be made public within a few minutes of execution and the data will include:

- Trading date and time

- Venue of execution

- Instrument identification code (ISIN)

- Price

- Notional

As well as Flags to signify details such as Cancel or Amend transaction or Non-Price Forming or Package transaction and many others.

Importantly a time deferral of 2 business days is available for transactions which are either:

- Financial instruments for which there is not a Liquid Market, or

- Large in Scale compared to normal market size for the financial instrument, or

- Above a Size Specific to the Instrument trading on a venue, which would expose liquidity providers to undue risk.

We will come back to the definition and operation of each of these.

Pre-Trade transparency

Trading Venues are also required to make public the range of bid and offer prices and depth of trading interest at those prices, in accordance with the type of trading system they operate. Interestingly for RFQ markets this means making public all the quotes received in response to the RFQ and doing so at the same time. In addition RFQ or Voice trading systems are also required to make public at least indicative bid and offer prices, where interest is above a specified threshold.

Which means lots of public pre-trade price information including depth.

Importantly this requirement is waived for the following:

- Orders that are Large in Scale compared to normal market size

- Orders that held in a order management facility of a trading venue pending disclosure

- Actionable indications of interest in RFQ or Voice that are above a Size Specific to that financial instrument, which would expose liquidity providers to undue risk.

We now need to tackle the meaning of Liquid Market, Large in Scale and Size Specific to Instrument.

Liquid Market

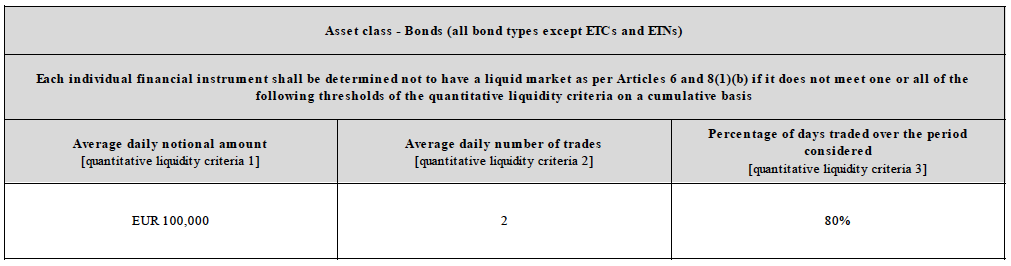

The assessment of Liquid for Bonds is based on a periodic (quarterly) assessment of quantitative liquidity criteria on an Instrument by Instrument approach (IBIA):

So for an ISIN to be liquid:

- Average Daily Notional must be greater than EUR 100,000,

- Average Daily Number of Trades must be greater than 2,

- Percentage of Days Traded over the period greater than 80%.

Competent Authorities will publish by December 1, 2016 the results of these transparency calculations, based on the reference period Aug 1, 2016 to Oct 31, 2016 and this assessment will apply from Jan 3, 2017 to May 15, 2017, after which it will be periodic (quarterly).

The Average Daily Notional and Average Daily Number of Trades look like low hurdles for many bond issues, but the Percentage of Days Traded at 80% will exclude many issues.

As a side note ESMA collected bond transaction data for the period Jun 2013 to May 2014 and included in the analysis 54,935 bonds, out of which 49% did not trade over the period.

So we are talking ten’s of thousands of ISINs, out of which a decent portion should be liquid.

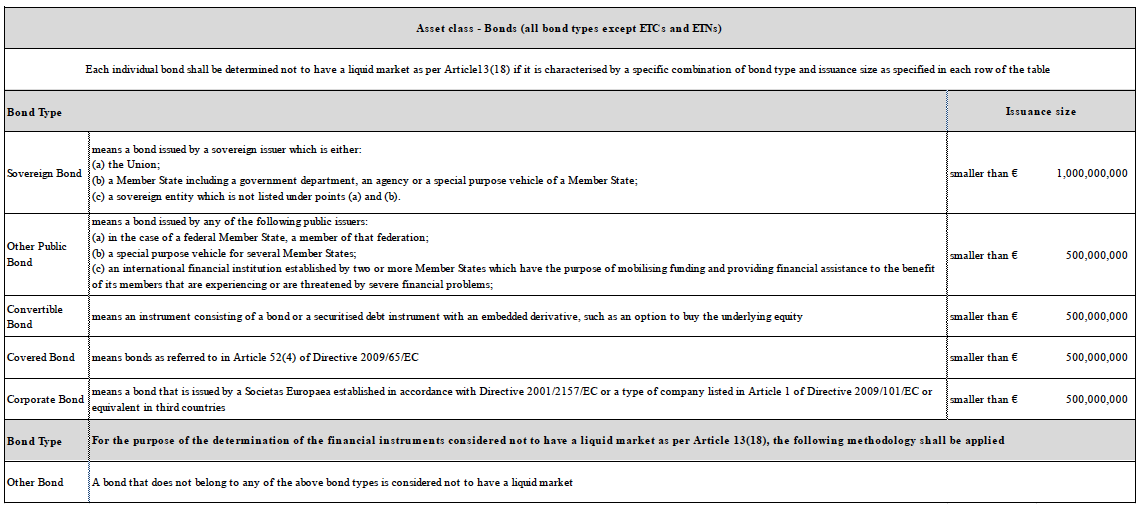

For Bonds that are admitted to trading or first traded on a trading venue in the prior quarter, shall be considered to have a liquid market based on the Issuance szie table below:

So a Sovereign Bond with Issue size of €1billion or more will be Liquid, while a Corporate Bond with Issue size of €500million or more will be Liquid.

Bonds first traded in the period from Oct 1, 2016 to Jan 3, 2017 shall be considered not to have a liquid market.

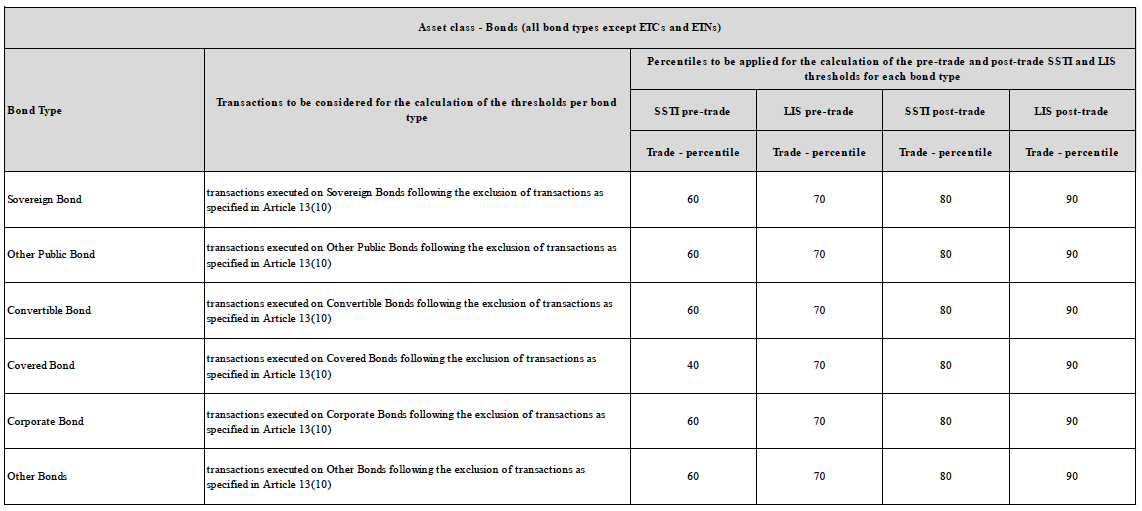

Large in Scale (LIS) and Size Specific to Instrument (SSTI)

For Pre-Trade and Post-Trade there are distinct thresholds for each Bond Type as to what is Large in Scale (LIS) or Size Specific to Instrument (SSTI) and these are lower for pre-trade given the greater sensitivity of this information. These are specified based on a trade percentile.

Showing that for a Sovereign Bond pre-trade LIS is 70% trade percentile and SSTI is 60%.

While for post-trade the LIS is 90% trade percentile and SSTI is 80% volume percentile.

Again the same periodic basis determination process will be used.

So we will know the threshold sizes by December 1, 2016.

And we can expect lots of new data to have to be published pre-trade and post-trade on lots and lots of bonds.

Well that completes the definitions and meanings.

I hope you are still with me.

Examples

Time for a few simple examples.

RFQ for a German Sovereign Bond in 100m notional size which then trades

This will surely be a Liquid Market, meaning that pre-trade the quotes provided to the RFQ will be made public in real-time (as technologically possible) and all at the same time.

And post-trade details will be made public, including execution time-stamp, instrument code, price and size.

RFQ for a Small Corporate Bond in 25m notional size which then trades

This will likely not be Liquid, meaning that no pre-trade quotes will be public and on trade execution only on T+2 business days will details be made public.

RFQ for a German Sovereign Bond in 500 million notional size which then trades

This will be Liquid and possibly above the LIS or SSTI threshold for pre-trade but below the post-trade thresholds.

Meaning no pre-trade quotes are made public but on trade execution, details will be made public in real-time.

RFQ for a German Sovereign Bond in 2 billion notional size which then trades

This will be Liquid and possibly above the LIS or SSTI threshold for pre-trade and post-trade thresholds.

Meaning no pre-trade quotes are made public but on trade execution, details will be made public on T+2 business days.

Final Thoughts

Thats it for MiFID II and transparency of bonds.

I am sure you will agree that the transparency changes are profound and significant.

For a market with tens of thousands of securities, with high volumes in specific issues and a long tail for many others, this transparency will have a profound impact and be interesting to say the least.

Roll on Jan 2017, sorry Jan 2018.

I plan to cover further aspects of MiFID II in future blogs.