Many firms are restructuring their fixed income businesses in order to compete in the new world of swaps. New regulations have made the industry more competitive, one where clients are no longer beholden to their large dealers; one where clients are reportedly taking liquidity based upon price, firmness, and response time.

We are seeing the overriding initiative in this restructuring to be centered on cost efficiencies, implemented around a few themes:

- Automation

- Leveraging pre-existing industry services

- Incentivizing cost-efficient behavior at the front-line (dealer level)

I will touch on the first two themes, but want to focus on the last point – that of instilling cost-efficient behavior at the front line.

Probably the largest cost that dealers incur is that of financing the margin requirements associated with their positions. Of course, it is not just a problem for large dealers, but also is of concern for insurance companies and large funds. In just the past few years, we have begun to see firms more explicitly charge their dealers (and investment managers) financing of initial margin.

It sounds easy, but when you have more than one book or entity trading into a single clearing account, someone is going to cry that they are paying more than their fair share. So how does an enterprise go about equitably sharing the costs of initial margin?

Example

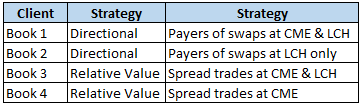

Let us take a hypothetical example, where a swaps business has 4 separate “books” or “entities”. You can think of this swaps business as anything ranging from a global swaps dealer down to an large investment manager or small fund. Taking this theoretical example, we have 2 distinct strategies across these 4 books – either a very directional position – or a relative value strategy. Their positions are summarized as follows:

Any smart enterprise will have all 4 of these books/entities trade into the same clearing accounts at CME and LCH, thereby gaining any possible diversification across the books, and hence minimizing margins.

I have, however, been surprised to learn that there seems to be many methods of sharing the costs across these books. I’ll list out the top 3 that we see:

- Gross Model. Each book pays costs based upon their portfolio’s gross margin, as if each book cleared directly. Costs are paid to an internal “broker” that faces the clearing member. The internal “broker” receives gross from each book, and pays net margins to the clearing member.

- Net Model. Each book pays their portion of costs, based upon their portfolio’s share of the net margin (based upon each books gross % share).

- Don’t Care Model. At the end of the month, each book gets assigned the same share of margin costs (1/4 in this example).

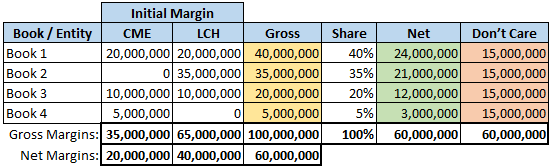

To illustrate this example, let’s take some hypothetical margin numbers:

To start with, the Net Margins at the very bottom are the important number, as they are the actual margins required to be pledged to the clearing member. In this example, it is 20 million for CME and 40 million for LCH. The question is, how much does each book pay? It depends on the approach:

- Under the Gross model, each book pays their gross amount (in the yellow column). The sum of these gross amounts is 100 million. The “internal broker” or business head takes those funds and pledges 60 million to the clearing member.

- Under the Net model, we compute each books share of the gross margins, and use that proportional percentage share of the net margins. Everyone here shares macro-level diversification equitably.

- In the final “Don’t Care” model, the business head or broker just asks everyone to split the costs equally (not equitably!)

It should go without saying that the “Don’t Care” model does not lead to dealers and portfolio managers acting in the best interest of the firm. The intent should be to incentivize appropriate behaviors by implementing some equitable share. Whether that is 1 or 2 (gross or net) it doesn’t really matter.

To really drive the behavior home, this financing charge should be assessed daily as part of a dealers P&L.

The Rub

Once it is decided that each dealer/book will share the costs on some equitable basis (gross or net), there arises two points of concern:

- Somebody needs to compute the book-level margins and costs every day, as you will likely not get this on a consolidated broker statement.

- In order to maximize their performance, a wise dealer will want to be able to incorporate this costs into their pricing. Note, this is precisely the desired behavior, as they will be actively managing the amount of margin and capital deployed for their strategies.

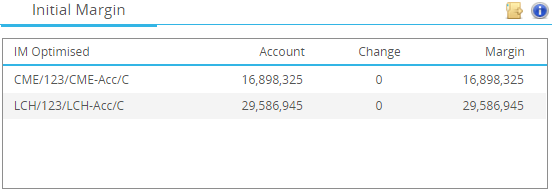

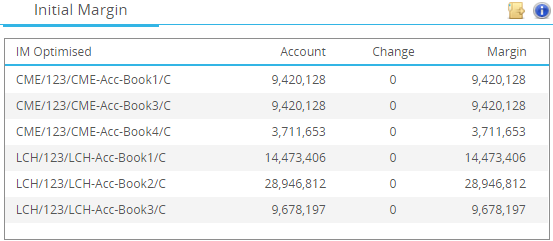

Number 1 is quite straightforward by leveraging a service such as CHARM. Below we’ll take a real example of these 4 accounts, but look at them both on the top-level broker (CME & LCH) account level, as well as the individual account level:

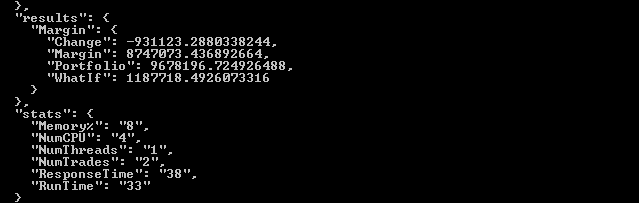

Number 2 – empowering the dealer to quickly understand the impact of incremental transactions – is also possible with the right tool. This time leveraging the CHARM API, we are able to retrieve the gross margin for our particular book – and do it in milliseconds.

In this example, within 33 milliseconds (over a WAN to the secure hosted CHARM micro-service), the dealer is able to ascertain that the incremental swap he is putting onto his books will result in a portfolio offset of $931,000 in margin terms.

Summary

Times are changing. The banks that wish to remain competitive in the swaps market need to actively assess what their business would look like if they built it from scratch. Building from scratch requires not only new technology, but also new behavior.

We at Clarus want to help, so please get in touch!

The ‘correct’ way to do it is none of those.

The firm has some amount of margin it must post. If a particular book were to close its position, what would this amount of margin become? The difference is the book’s marginal contribution to the firm’s required margin. Floored at zero: no negatives.

So, if book A is massively received 10Y, book B is massively received 10Y, and book C is slightly paid 10Y, then C should be free — it is net reducing the firm’s need for margin.

Thanks for the comment Julian. Yes agreed, a very good example of Incremental Var. It behaves like the “Gross” model in that the sum of each books marginal contributions will be larger (or in rare cases at least equal to) the net due to the clearing firm.

Not quite: ‘Marginal’ incentives players to have positions in the opposite direction to others in the firm; whereas ‘Gross’ is neutral between increasing and lessening the firm’s risk.