This year both CME and LCH launched clearing in new Non-Deliverable Swap (NDS) currencies and in today’s article I will look at how volumes in these products have performed.

CME – NDS in CLP and COP

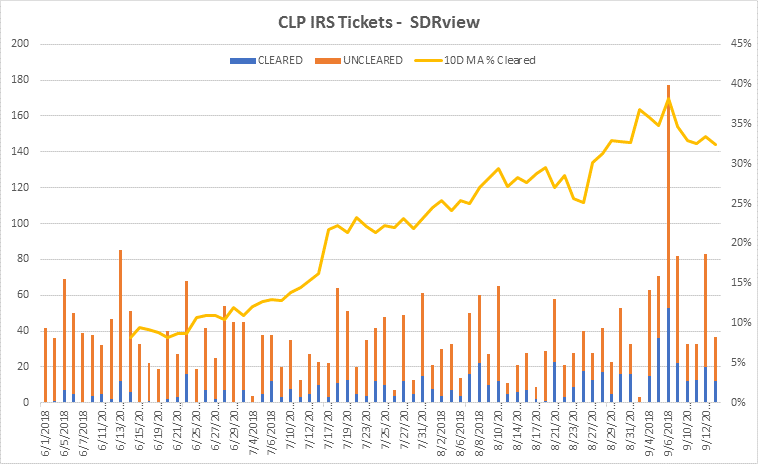

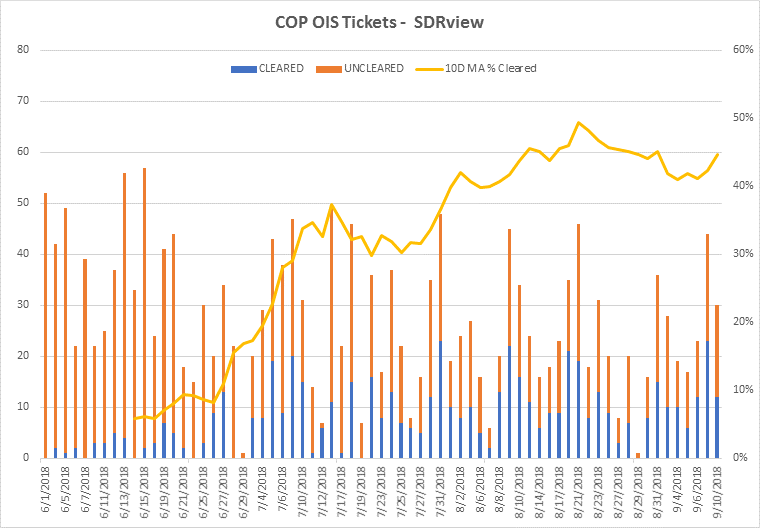

In May 2018, CME launched Chilean Peso and Columbian Peso NDS as new currencies and both of these have seen very quick market uptake.

Using SDRView, we can see that the number of trades reported by US persons that are cleared in just over 3 months from launch has gone from zero to 30% for CLP and 45% for COP.

The yellow line shows the 10-day moving average of the % of cleared trades in the total trades reported.

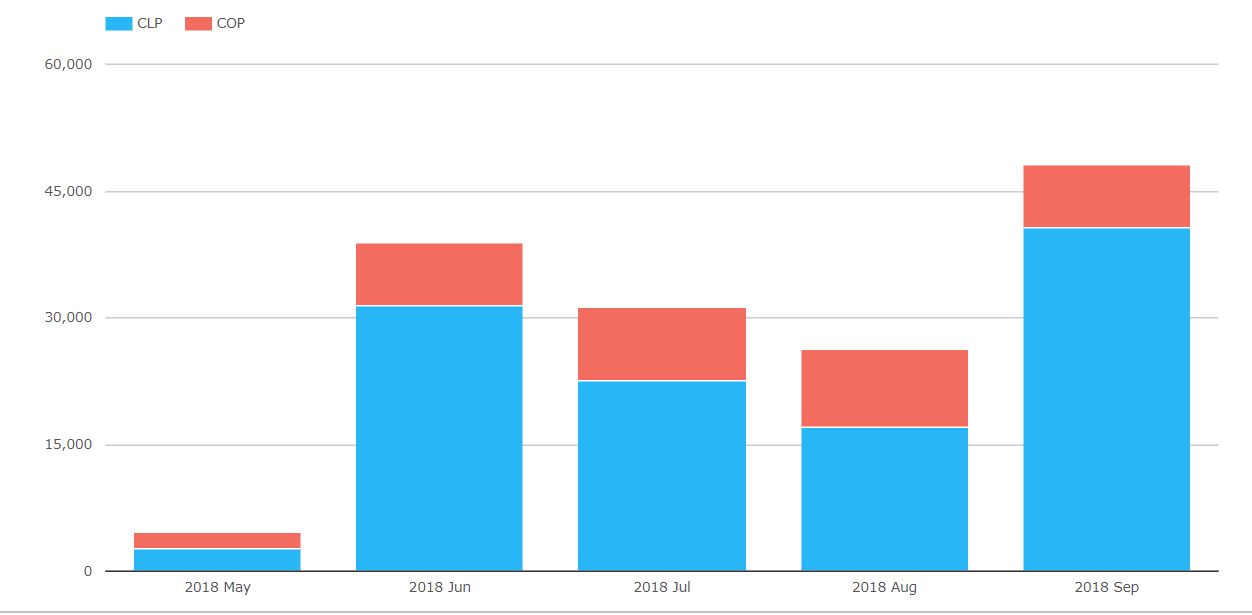

And from CCPView the single-sided cleared gross notional monthly volume.

Showing CLP the larger with $40 billion in September (up to 21 Sep only) and COP with $9 billion in August and on track to exceed that this month.

These currencies adding to the dominant market share and strong growth that CME has shown in LatAm with BRL and MXN to the fore. (Note that BRL is non-deliverable and a zero-coupon structure).

(The full list of CME OTC Cleared IRS products is here).

LCH – NDS in CNY, INR, KRW

In April 2018, LCH SwapClear launched CNY, INR, KRW, which have also performed very strongly since inception.

Showing large month on month increases in single-sided gross notional cleared and with only 3 weeks out of 4 in the September figures, looks like September will be the largest month to date.

KRW the largest with $166 billion gross notional in August, CNY next with $79 billion and INR with $54 billion.

These currencies adding to the dominant market share and growth that LCH SwapClear has shown in Asia.

(The full list of LCH SwapClear products is here).

A Two Horse Race?

So can we assume that in NDS it is a two horse race, with CME the winner in LatAm and LCH in Asia?

Pretty much.

As while there is significant volume in specific currencies in domestic CCPs, for example Shanghai Clearing in CNY and CCIL in INR, for wider currency coverage, it is only a choice between CME and LCH.

Widening our scope from NDS to deliverable currencies in each region, further reinforces CME and LCH’s regional strength, as CME is also dominant in BRL and MXN, while LCH SwapClear is also dominant in HKD, SGD, NZD.

And while LCH also offers MXN and CME offers many Asian currencies (e.g. HKD, INR, KRW, NZD, SGD), each CCPs respective market share in these is a fraction of the dominant share of the other.

It will be interesting to see if this LatAm vs Asia, split between CME and LCH continues.

Or if regional CCPs attract more international participants and market share.