Last week’s default at Nasdaq Clearing in the power market, generated a lot of press, both because member defaults are few and far between events at CCPs and the fact that it coincided with the ten year anniversary of the Lehman’s bankruptcy.

There are few analogies that we can draw between the two events; the Lehman’s bankruptcy was of global systemic importance, resulting in a massive loss of trust in the safety of the entire financial system, one that required regulators to step in with emergency crises management measures, while the former is limited to a regional commodities market and has been handled by the clearing house and its members.

However given that one of the major regulatory reforms from the Great Financial Crisis was to move more Derivatives to central clearing and so increasing the systemic importance of CCPs, it is of concern that in last week’s default, we had the rare event that two-thirds of the mutual default fund had to be used as the defaulting traders margin was grossly insufficient.

For this reason there is a lot of regulatory interest with Swedish regulators announcing an investigation. For my part I thought it would be instructive to look at what the CPMI-IOSCO Quantitative Disclosures that all CCPs publish on a quarterly basis tell us about Nasdaq Clearing and its Commodities clearing service.

Recap

First a quick recap of events.

- Mon 10 Sep, spreads between Nordic and German Power markets diverged massively, with a move 17 times larger than a normal day

- Tues 11 Sep, Einar Aas, a well known Norwegian power trader and one of the largest tax payers in Norway, who was clearing his own trades, was not able to meet margin calls and was declared in default

- Wed 12 Sep, his portfolio with outsized positions was liquidated and bought by another large trader in the market (four firms were invited to bid).

- It cost EUR 114m to close out the positions, which was covered by the Default Resources of the Clearing House, EUR 107 million from member contributions and EUR 7 million from Nasdaq, out of a total Default Fund of EUR 166 million (so over two-thirds)

- Nasdaq asked members for EUR 100 million to replenish the default fund

- Mon 17 Sep, Nasdaq informed members early in the day that 90% of the recapitalisation funds were received and the remaining would be there by end of day

Sources and more details for the above are Financial Times, Reuters, Reuters, Bloomberg and for more on Einar Aas himself, see Financial Post.

Thoughts

The unusual fact that springs out from the above was that an individual trader, was self-clearing! Granted he was a very successful professional trader with a 20 year history in these markets; but even so it is unusual, unless in commodity markets this is more prevalent than asset classes.

Self-clearing means the layer of oversight from a clearing member was missing, but then Nasdaq itself had direct visibility on the positions.

Initial margin using SPAN allows for offsets between intra-commodity and inter-commodity spreads, which are calibrated by the Exchange using historical price data. It is well known that in times of market stress historical correlations break down and consequently full offsets are not given between commodities in the margin methodology.

While I can see how IM would not be sufficient for a 17 times(!) larger than normal move, I would think that contract position limits would have been a line of defence here against such outsized positions and should have kicked in earlier to reduce the loss possible.

No doubt the investigation by Nasdaq’s supervisor will report on these and other matters in its findings.

Onward.

Nasdaq Clearing Disclosures

The most recent CPMI-IOSCO Disclosures, covering margin, default resources, credit risk, collateral, liquidity risk and more are for 31 March 2018.

We collect these in CCPView for all major CCPs, so lets look at what they tell us about Nasdaq Clearing. First we note that Nasdaq operates three separate Clearing Services, each with their own Default Funds and Membership, these are Commodities, Financial Markets and Seafood and only the first is relevant here.

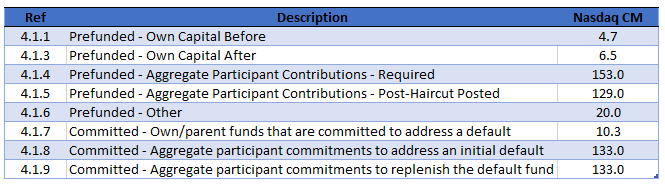

The Default Fund for Commodities as at 31 March 2019, all amounts in EUR millions.

Showing that:

- Nasdaq’s own capital to be used before participants was EUR 4.7 million, so this will have been lost.

- Pre-funded aggregate participant contributions of EUR 153 million (or EUR 129 post haircut), so the EUR 100 million will have been lost from this

- Nasdaq’s own capital after was EUR 6.5 million, so presumably the balance of EUR 3.3 million out of EUR 7 million came from this

- I don’t know where Prefunded Other of EUR 20 million comes from and if this will have been used

- Committed by Nasdaq to address a default EUR 10.3 million

- Commited by participants to address an initial default is EUR 133 million and a subsequent default(s) a further EUR 133 million, a total of EUR 266 million

So certainly more than enough Default resources available to cope with the Einar Aas default.

Of course those who lost a large chunk of their contributions will ask why the IM and DF contribution of the defaulting party was not sufficient to cover the loss. But that can be a double edged sword, as most members would not want IM to be so high as to never require the use of a default fund, that would make clearing more expensive for all.

(More details on the Default Fund Waterfall are here).

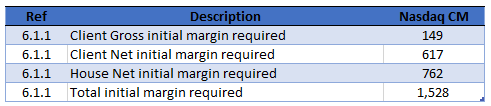

Initial Margin

As of 31 March 2018, we see:

A Total Initial Margin required of EUR 1.5 billion, half from members (house) and the balance from clients. Presumably Einar Aas’s IM would have been in the House figure of EUR 762 million.

Of-course the IM as of 10 Sep 2018, will have been different from EUR 1.5 billion, either higher or lower as it changes based on the size of positions and market volatility, but it is unlikely too have been too far from this number.

The disclosures tell us that SPAN is used for the IM calculation, with the usual 16 price and volatility scenarios to simulate worst loss in contract series and allowing for netting (correlation) of margin between contracts with opposite positions within and across markets, so it is this last that will most likely have been found wanting in this case.

Other details on IM:

- The Margin Period of Risk (MPOR) used for Nordic and German Electricity contracts is 2 days, while for Dutch, UK and Other Electricity contracts it is 4 days.

- Confidence level of 99.2% and a lookback period of 2 years (+25% buffer).

- Backtesting is performed using the SPAN model and a max MPOR of 4 days and 99.98% and these showed that for Energy there were 8 breaches out of 46,065 observations with a peak breach of EUR 286K.

- Meaning that either the characteristics of the type of position held by Enar Aas was not included in one of the backtested portfolios or the historical observations did not contain any such market move (plausible for a 17 times the daily move event).

Other Disclosures

Lets look at a few more of the relevant disclosures from March 2018

- 4.4.3 Estimated largest aggregate stress loss (in excess of initial margin) that would be caused by the default of any single participant and its affiliates in extreme but plausible market conditions; Peak Day Amount in previous 12 months was EUR 94 million.

- 4.4.7 Which is as above but for two participants was EUR 116 million.

- Given it now 6 months later, the EUR 94 million is ballpark comparable with the actual EUR 114 million of last week; presumably a more recent 4.4.3 calculation would have been higher.

- 4.4.6 Actual largest aggregate credit exposure (in excess of IM) to any single participant; peak day amount in previous 12 months was EUR 9,000, showing how actual historical experience can differ massively from what can happen in the future.

- 6.8.1 Maximum aggregate initial margin call on any given day over the period was EUR 549 million

- (Maximum Total VM is only available at the Nasdaq Clearing level and not Commodities level, so not relevant here).

- Number of general clearing members was 16, number of direct clearing members 84, number of others 115, where others includes Clearing Clients and Client Representatives, of which Einar Aas must have been one.

- Percentage of open positions held by largest 5 clearing members at its peak was 52%, while the percentage of IM posted by largest 5 was 77%, and largest 10 was 83% not unusal concentrations for a clearing service.

- Average Daily Volume data show that the Power contracts are massively larger than any other commodity traded (Carbon, Freight, Fuel Oil, Renewables).

So a lot to digest there, the one that stands out for me is that with 213 member participants, press reports state that only were invited to 4 bid in the default auction with one buying the whole portfolio?

Presumably these were the only firms large enough to be able to take over these positions at such short notice.

There is a lot more to digest and analyse.

Including comparisons with other CCPs in similar markets.

CCPView has lots of disclosure data for those interested.

Final Thoughts

For myself, the question remains is blame entirely with Einar Aas?

After all an experienced professional trader should not end up in this position.

Or is Nasdaq Clearing also responsible in some way?

How long were these positions open and could they have been reduced earlier?

Would the situation have been different if Einar Aas was not self-clearing?

Or is the fact that the loss was contained within Default Resources, testament to the fact that Clearing worked as intended and every now and again such events happen?

We will need to wait for Nasdaq and the Swedish regulators reports to get answers.

Nice article!

Although Nasdaq members had to bear the loss by writing off part of their default fund, should we now expect that EBA will review the default fund requirements from regulatory capital view point!

Thank you.

Good point, capital requirements for ccp exposure might need to be looked at.

What this shows is that the clearing houses are not fit for purpose:

SPAN is not an appropriate tool for risking power spreads. It is embarrassingly simplistic.

The IM on these kind of positions is clearly insufficient.

’17 times larger than a normal day’ ? How many times does the error in this thinking have to be pointed out?

The clearing houses are not capable of correctly risking these positions. They just roll out the same methodology over and over again, whether or not it makes sense.

The clearing members would much prefer IM to be higher so as not need the default fund. DF is lost cash, the IM is funded collateral. Big difference.

Only 7m of their own contribution? Expect that to be recalibrated across the board.

Canary in the coal mine.

Thanks for your comment, you raise some very good points.

I don’t know much about the Power market, but agree SPAN is a dated methodology.

Very good point on IM as funded collateral and a Default being lost cash.

I did read that Nasdaq have raised their margin rates, which is to be expected.

On the CCP’s own contribution, there was a long running “skin in the game” debate last year,

which seems to have gone quiet, so we may expect more on this.

https://streetwiseprofessor.com/he-blew-up-real-good-and-inflicted-some-collateral-damage-to-boot/

More from Pirrong:

https://streetwiseprofessor.com/the-smoke-is-starting-to-clear-from-the-aas-nasdaq-blowup/

He is right to bring up the intricacies of the auction process. One thing he leaves out though is when a defaulted portfolio is auctioned, traders from the clearing firms are seconded to the CH to perform the operation (certainly in OTC, I forget if this is the case in futures). So you are auctioning a defaulted portfolio into a stressed market and have all the issues he mentions; the firms want a discount, the CH wants to restrict who gets asked for bids so as not to spread panic, and the traders most qualified to manage the risk to the clearing members are not at their own desks.

If this happens in a smaller market and the auction fails, they may just cancel the trades. Thus the party who is in the money has their position extinguished.

If it happens with a big OTC portfolio, that’s anybody’s guess, but it won’t be pretty.

Thanks for the article. Self-clearing was a big problem, absolutely. This frames the whole affair.

The position ended up being too large for the liquidity of the market. (Position limits for the trader?). This raises the question of which contracts should be eligible for CCP clearing.

Then there was the issue with MPOR. Was it the minimum 2 days? Unwinding the trader’s position under normal conditions wood have taken more.

NASDAQ’s lookback for commodity IM calibration is just 1 year, not 2 years.