Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in Nov 2015.

First the highlights:

- On SEF USD IRS Nov 2015 volume was similar to Oct 2015 and up 25% compared to Nov 2014

- USD SEF Compression volumes were down 50% from Oct and the lowest since April 2015

- GBP & EUR SEF Compression volumes were $50b, more than double any prior month in 2015

- USD Swap Curve flattened over the month

- CME-LCH Basis Spreads continued to rise significantly

- With 30Y up from 2.5bps to 4.5bps

- CME-LCH Switch trade volume was double the monthly average at $75b

- Tradition captured most of this with $45b

- SEF Market Share remains largely similar to YTD

- Bloomberg in front with 31%

- ICAP and Tullet combination would be second with 26%

- Tradeweb plus DW is down, 18% in Nov compared to 22% YTD

- Mainly due to lower compression volumes

- Global Cleared Volumes in G4 Ccys were higher than Oct and similar to Sep

- LCH SwapClear Client Clearing USD Vanilla IRS volumes continue to gain vs CME

- LCH SwapClear’s share was 70% vs 30% at CME, a YTD high

And there is more. So onto the charts, data and details.

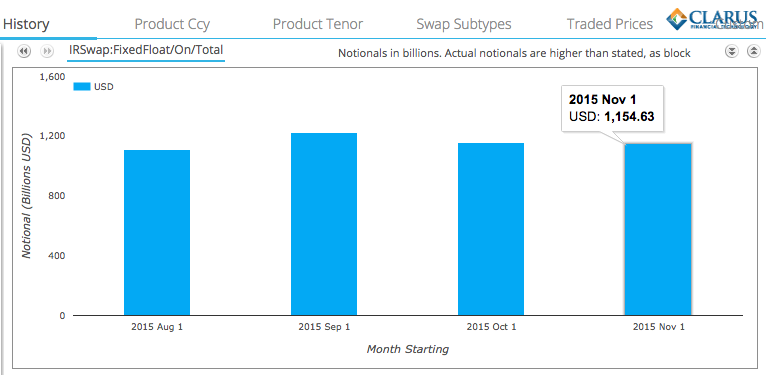

USD IRS ON SEF

Using SDRView lets start by looking at gross-notional volume of On SEF USD IRS Fixed vs Float and only trades that are price forming, so Outrights, SpreadOvers, Curve and Butterflys.

Showing that:

- November gross notional is >$1.15 trillion

- Similar to October and down 5% from September

- Compared to Nov 2014, gross notional is up 25%

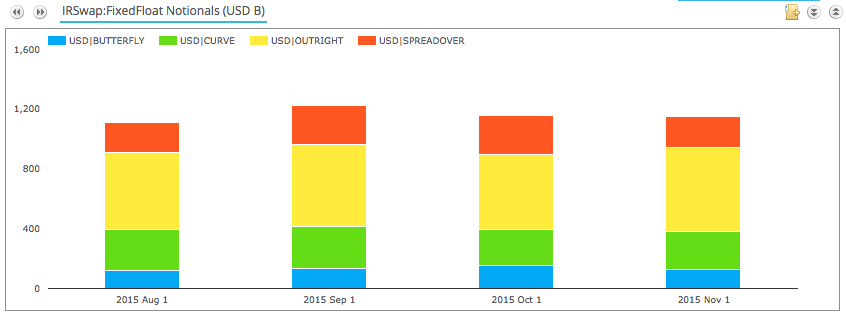

And splitting this by package type.

We see similar overall volume compared to October, with Outright and Curve in higher proportion.

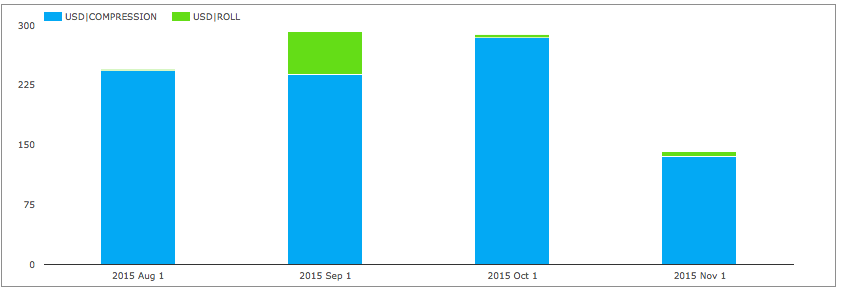

And non-price forming trades; Compression and Rolls.

Showing that:

- Compression activity is significantly down

- >$136b in Nov, vs >$285b in Oct

- Down 50% and the lowest since Apr

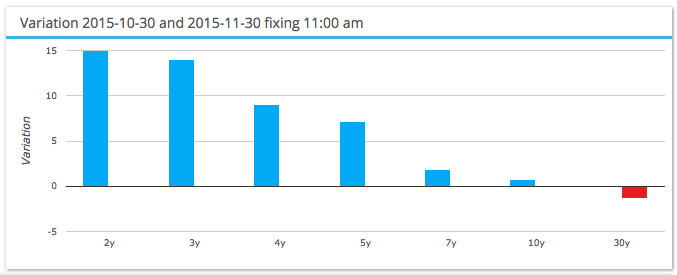

USD IRS Prices

Using SDRFix lets take a look at what happened to USD Swap prices in the month.

Showing that the Swap curve flattened:

- Short tenors rising 15 bps

- Medium tenors rising 7 bps

- Long tenors flat or down slightly

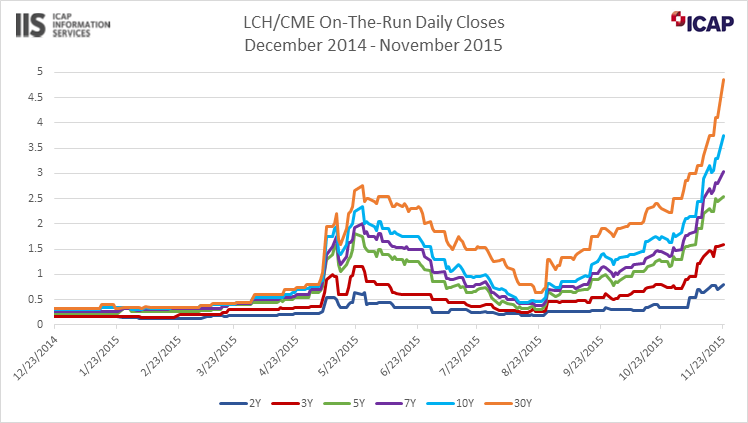

CME-LCH Basis Spreads

The real price action took place in CME-LCH Basis Spreads, with prices hitting new highs.

Lets look at the Tradition page from 23 Nov.

Showing that:

- 30Y hit a new high of 5.3bps, up from the 3.7bps in my Spreads Blow Out blog

- 10Y at 4bps (from 3bps) and 5Y at 2.8bps (from 2.3bps)

- While rates were back down the next day, with 30Y at 4.5bps, 10Y at 3.4 bps and 5Y at 2.4bps

- They remain at elevated levels

- Compared with 30-Oct spreads of 30Y at 2.5bps, 10Y at 1.8bps and 5Y at 1.35bps

The chart below from ICAP, illustrates this nicely.

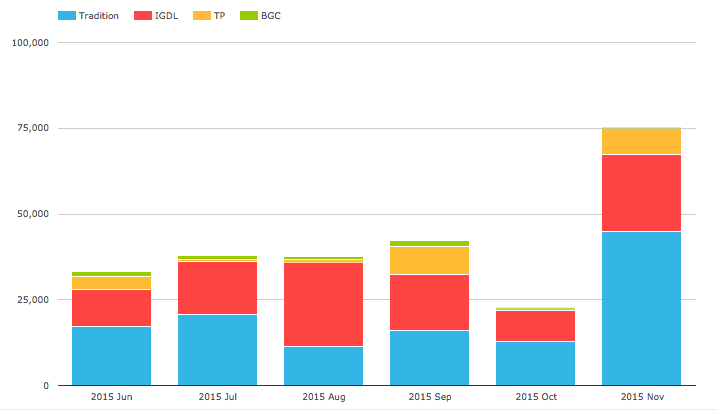

CME-LCH Basis Swap Volumes

This increase in level and volatility of the spread has resulted in higher volumes of CME-LCH Switch trades.

Using SEFView we can isolate CME Cleared Swap volume at the four major D2D SEFs (on the assumption that this is all CME-LCH Switch trade activity). Lets look at this for the past 6 months.

Showing that:

- Nov gross notional volume was $75 billion

- Double the usual $35b we see in a month

- Tradition captured most of the increase

- Tradition did $45b of the $75b for a 60% share

- ICAP at $22b was also higher than its monthly average

- Tullet at $7.7b

- In DV01 terms Nov share was Tradition 56%, ICAP 37% and Tullet 6%

- YTD DV01 Share is Tradition 48%, ICAP 42%, Tullet 7.5%, BGC 1.8%

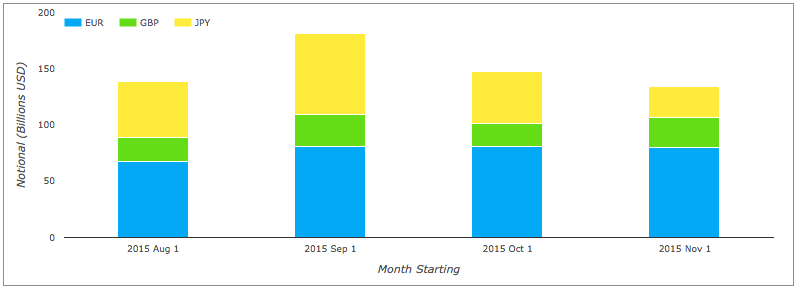

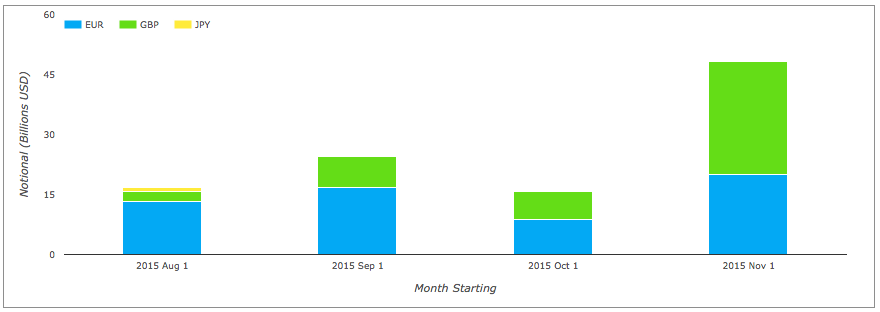

EUR, GBP, JPY Swaps

Lets also take a look at On SEF volumes of IRS in the other three major currencies.

Showing that for price-forming trades JPY volumes were much lower in Nov compared to Oct, while EUR were similar and GBP slightly higher.

And then looking just at SEF Compression activity.

We see that unlike USD, compression volume is higher, with EUR at $20b and GBP at $28b. In-fact this is by far the highest month for EUR and GBP in 2015, almost double the previous monthly high in Sep.

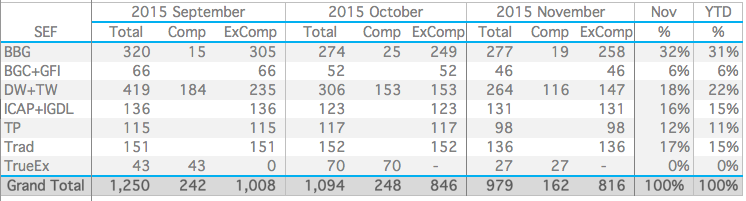

SEF Market Share

Lets now turn to SEFView and SEF Market Share in IRS including Vanilla, Basis and OIS Swaps.

We will start by looking at DV01 (in USD millions) by month for USD, EUR, GBP and by each SEF.

Showing that

- Bloomberg’s Nov share of 32% is consistent with its YTD 31% share

- BGC+GFI is 6% in Nov and YTD

- DW+TW in Nov is 18%, well below its 22% YTD share

- Both Compression and Price-Forming volumes down from prior months

- ICAP share at 16% is similar to its 15% YTD

- Tullet volume is down but share at 12% is similar to 11% YTD

- Combining ICAP and Tullet would be 26% YTD, so No 2 in the list

- Tradition volume is down from prior month, but share at 17% is above the 15% YTD

- TrueEx is down from prior months

- Compression is down at each of BBG, TW, TrueEx

- Overall DV01 ExComp at $816m is just below Oct and 20% less than Sep

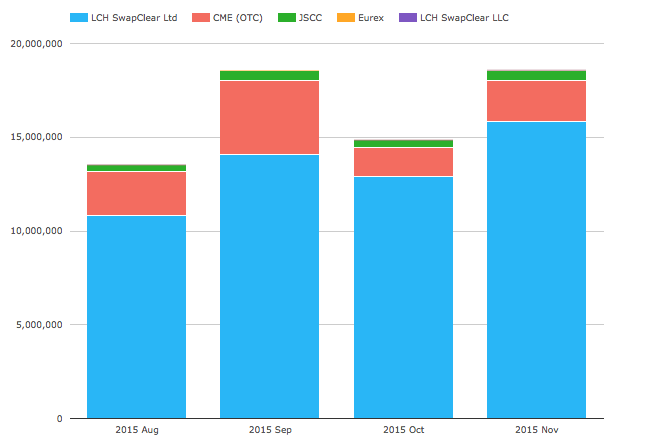

Global Cleared Volumes

Finally lets use CCPView to look at Global Cleared Swap Volumes for EUR, GBP, JPY & USD Swaps.

Showing that:

- Overall volumes in Nov are much higher than Oct and similar to Sep

- LCH SwapClear volume is up at $15.8 trillion (cf $14.1 trillion in Sep)

- CME volume at $2.2 trillion is higher than the $1.5 trillion in Oct and $1.8 in Sep

- JSCC volume at $565 billion is higher the the $525 billion in Sep

- Eurex just about showing on the chart with $8.7 billion

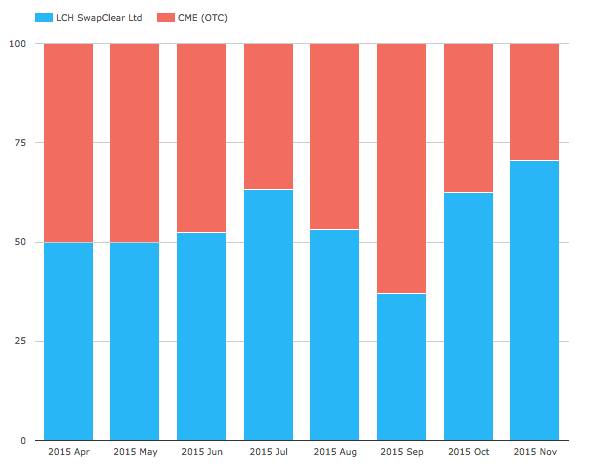

Given the CME-LCH Basis Spread widening, it is also interesting to look just at USD Vanilla IRS and compare LCH Client Clearing with CME OTC on a percentage of total basis.

Showing that:

- In Apr/May/Jun the share was equal at 50% each

- This has been increasing in LCH SwapClear’s favour

- We need to ignore Sep as CME includes TriReduce compression in this month

- Oct was 62% to 38% in LCH SwapClear’s favour

- Nov is 70% to 30% in LCH SwapClear’s favour

Clearly the CME-LCH Basis spread widening has resulted in a significant shift of Client volume to LCH. Comparing April to November, we estimate that around $450b gross notional volume has shifted from CME to LCH.

Thats it for today.

A lot of charts.

Thanks for staying to the end.

Our Swaps review series is published monthly.