- Limited market moves didn’t necessarily dampen trading volumes

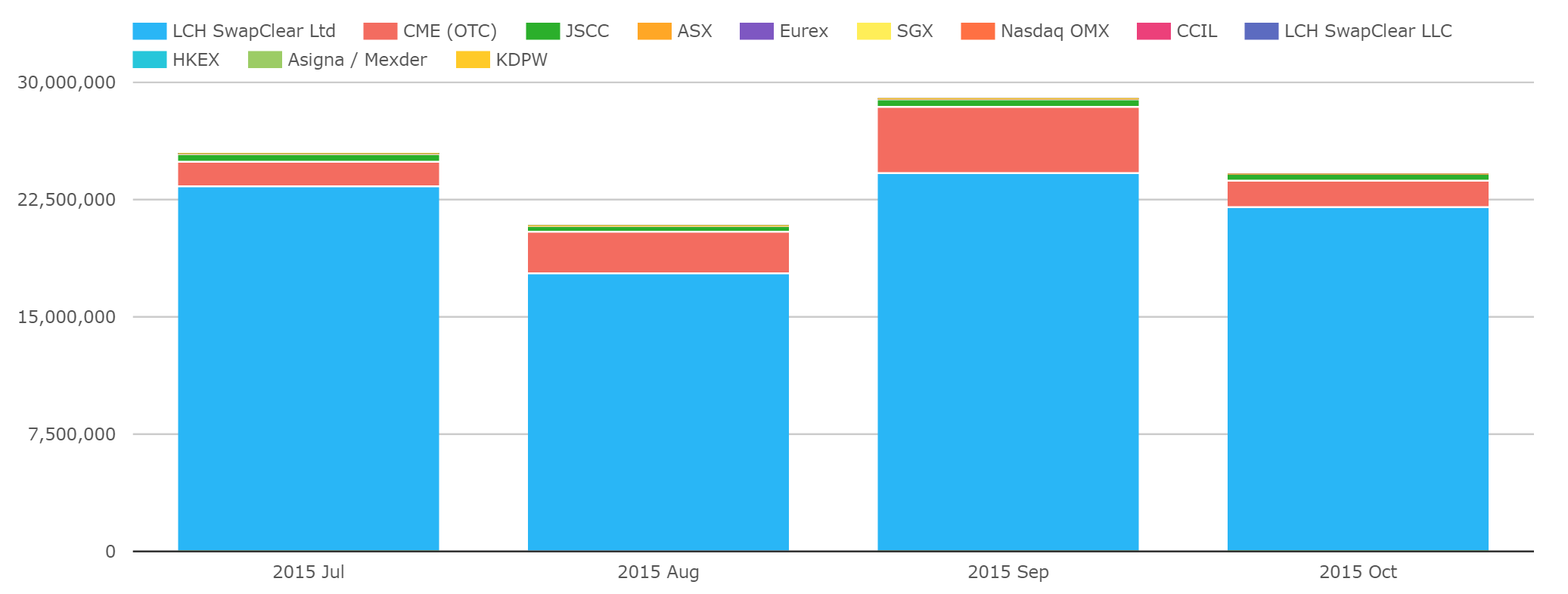

- Despite a widening CCP Basis, volumes in the hedging of this price differential have materially decreased

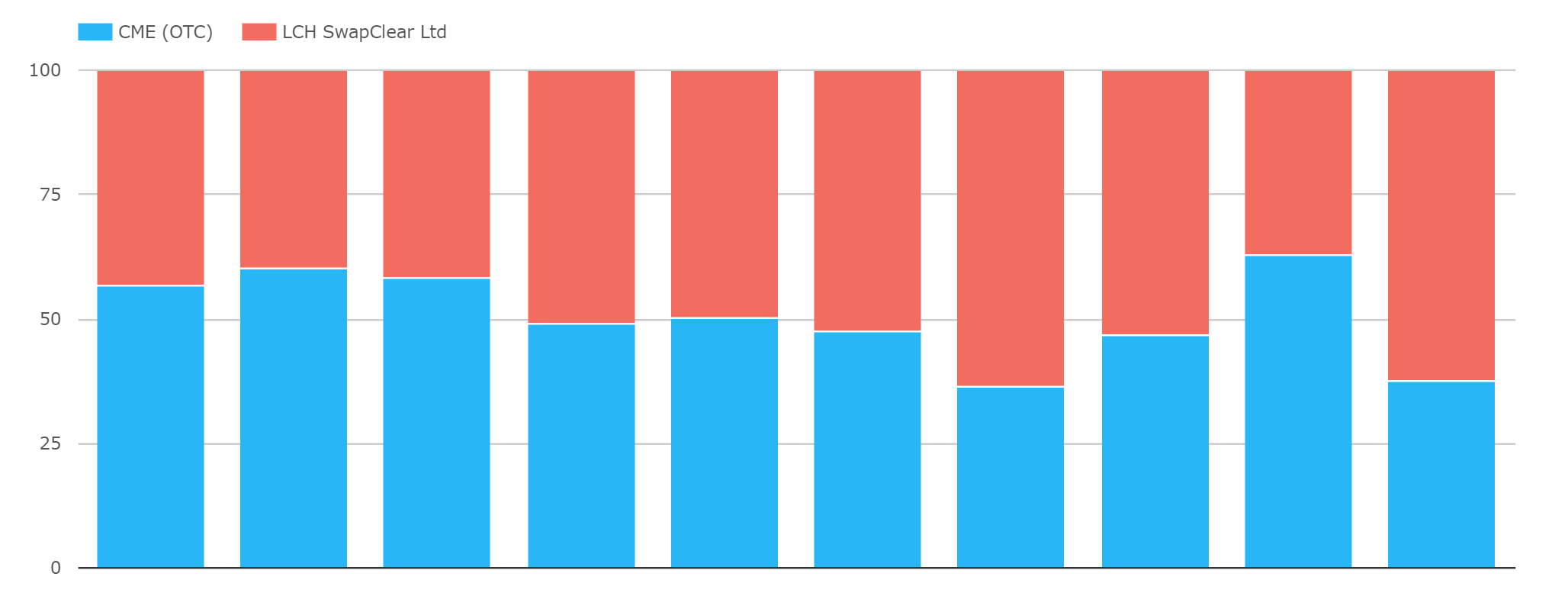

- Whilst LCH have increased their market share of USD swaps in the Client Clearing space

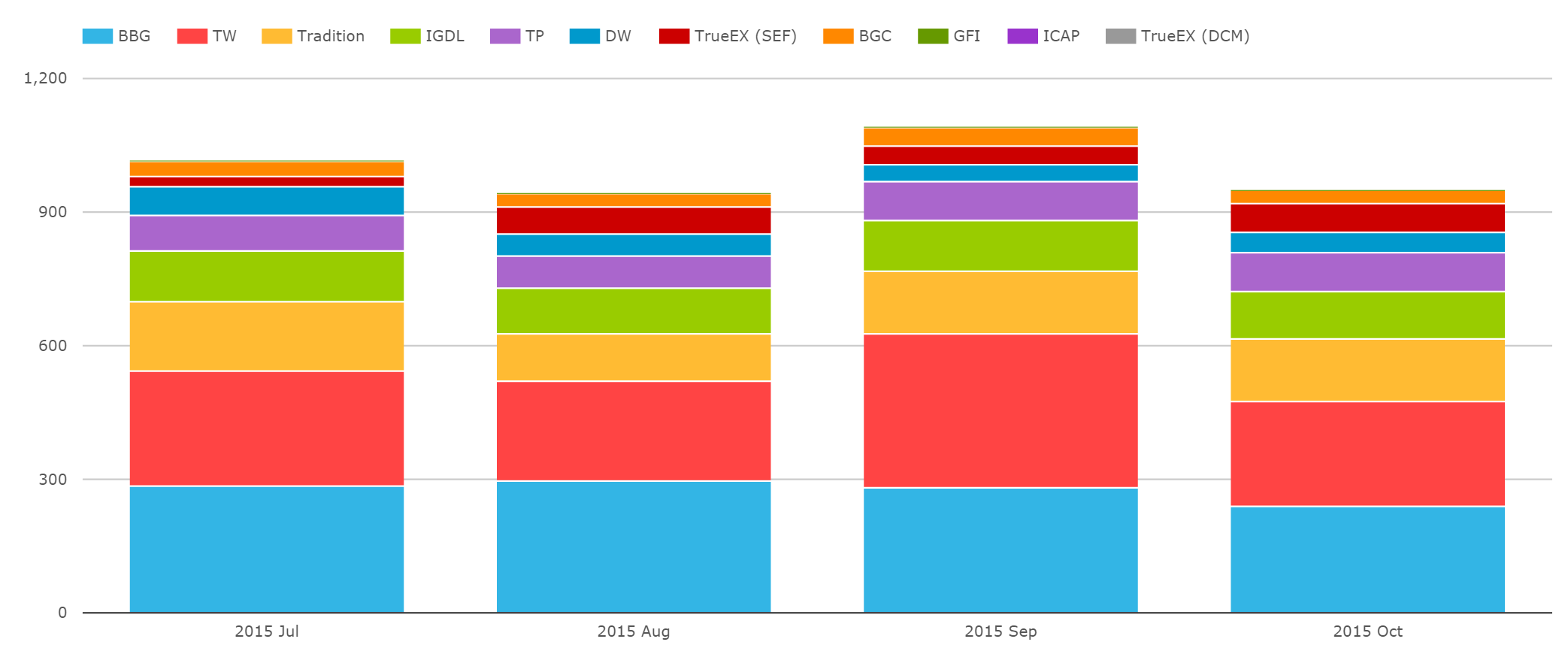

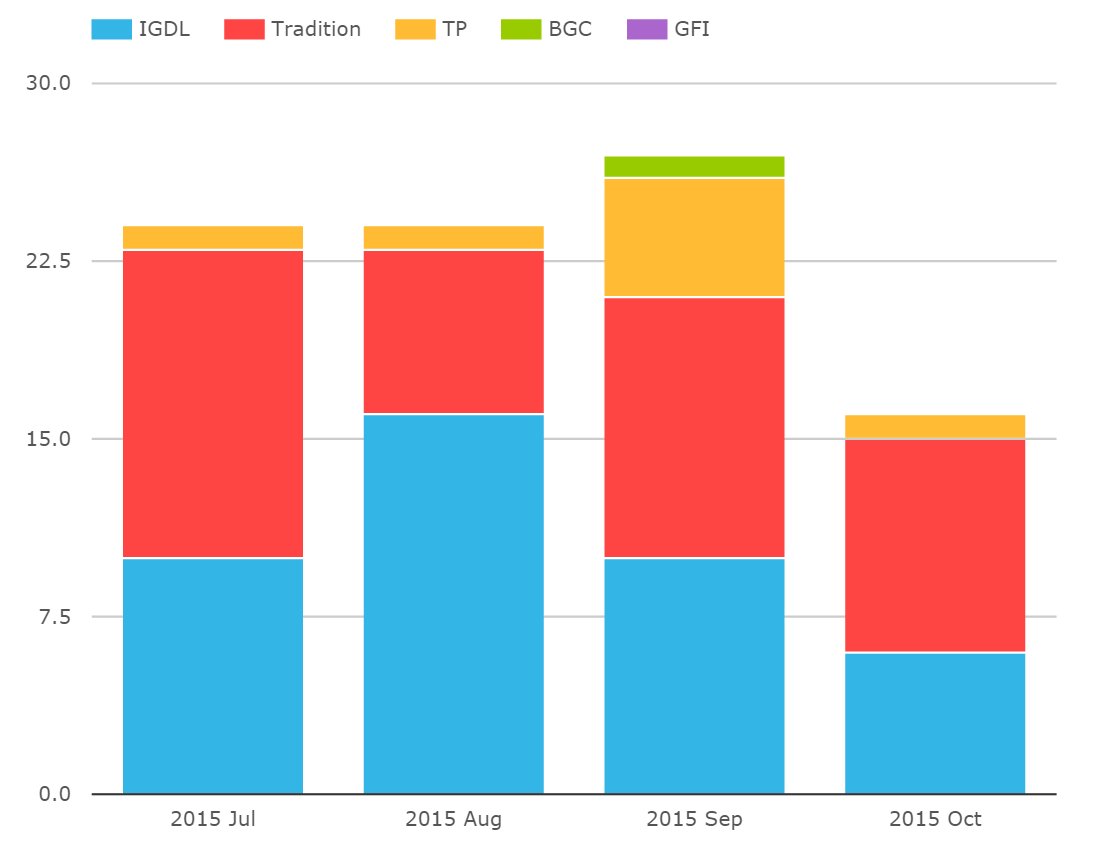

- For the SEFs, both Trads and Tulletts enjoyed very strong months

Market Moves

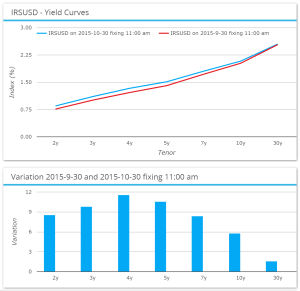

Well, talk about a dull market in October. Despite ending close to the highs in 10 year yields, we’re still talking about moves of less than 10 basis points across the curve. Move along…not much to see here:

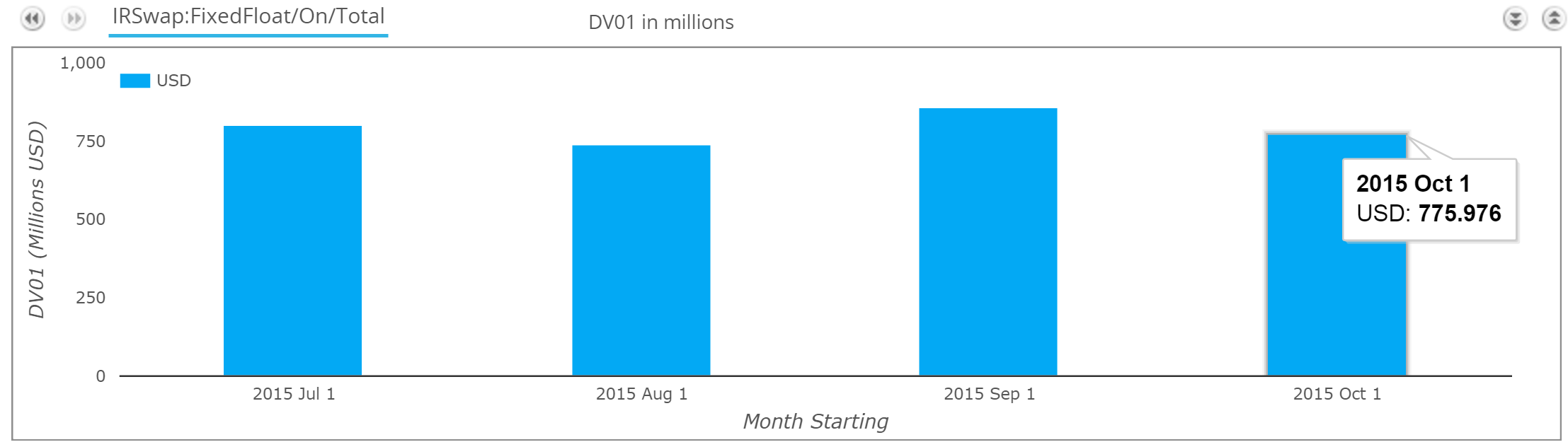

USD IRS On-SEF Volumes

This dull price action may be expected to lead to a dearth of volumes, but they were actually fairly robust. Across many metrics, volumes looked similar to July this year. So does that make July the pre-Summer healthy period, August the Summer lull that wasn’t, September the Fed-driven anything-could-happen-but-didn’t month and October a welcome return to normality? It sure feels that way:

SEFView

This return-to-normal gives us similar figures in SEFView to SDRView – once again, we see roughly $1trn in DV01 trading, which is some 25% higher than in SDRView. This suggests there wasn’t a crazy amount of capped trades going through last month, despite the preference for RFQ that we’ve been writing about.

It’s worth noting that November has started with the CFTC extending the NARL relating to Block Trading across SEFs, so we won’t be seeing any change in trading protocol until at least this time next year.

Global Cleared Volumes

From CCPView, we see that volumes were pretty healthy across all of the Cleared Rates products:

That chart helps once again highlight the similarity to July. And on a market-share perspective shows the very good performance of LCH, which we revisit further down the page.

CCP Basis

As a point of note, the CCP Basis (see Amir’s last update here) has seen volumes materially decrease during October. All of the IDBs were affected, suggesting it’s a market-wide phenomenon:

We’re a little surprised by this development, as our latest market-update shows that the basis was widening or maintaining its’ widest levels, which had driven volumes in previous episodes. Maybe CCPView can (inadvertently) shed some light.

CCP Client Clearing

We don’t update our clients on this every month, so it’s worth refreshing our assumption that all of CME’s cleared volume is client-related. Before the CCP Basis blew out, this was a fair assumption, and this month we’ve seen a decrease in CCP Basis volumes in the IDB market anyway, so the basis does not distort the volume picture as much as it has in previous months.

That stated, the LCH volumes look impressive this month. Taking just the client-clearing volumes from LCH, we see they enjoyed an equal YTD market share high of 63% for USD swaps in October:

We’d need to see a continuation of this LCH-dominance to start looking seriously at the reasons for the market-share gain. And as Amir said in his blog, it’s not necessarily evident in the week-by-week numbers. But the aggregated time series does raise some questions.

Is the LCH market share increase due to clients rolling positions out of CME at both the March and Sep IMM dates? Is it due to the recent triOptima compression run at CME reducing any portfolio maintenance trades? We do not know the answers to these questions just yet, so it’s best to keep an eye on these numbers. We certainly will be!

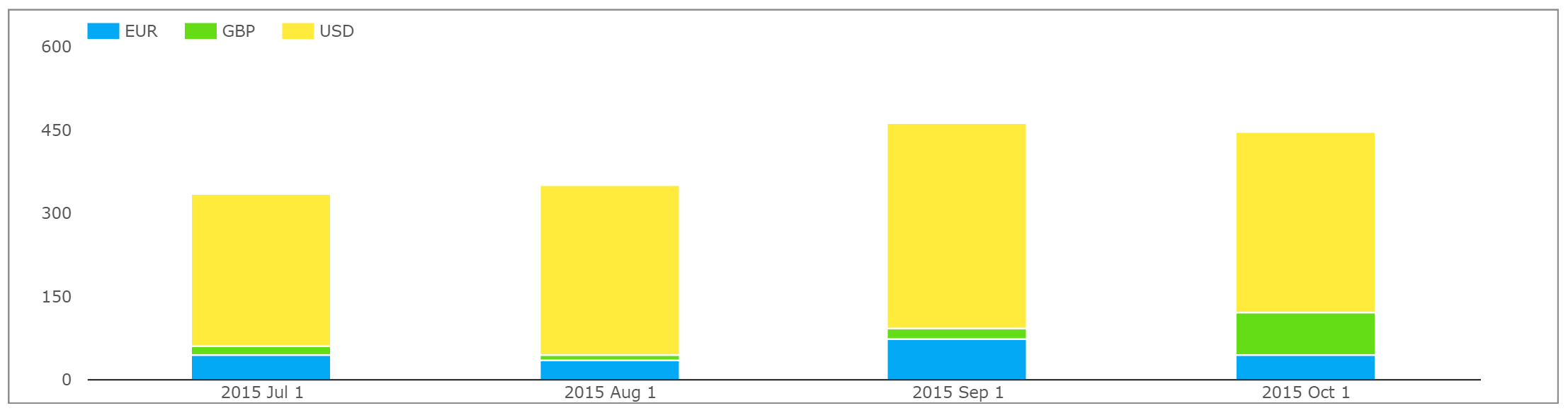

Ex-USD Block Trading

Seeing as I appear to have a penchant for all things block-related at the moment, I did a quick check this month of capped trades. It seemed rude and churlish not to after my blogs on the subject here, here, and here.

And then the CFTC goes and extends the NARL, so that the current vogue for trading RFQ is cemented until at least this time next year….so it seems timely to look at some history of volumes. See below:

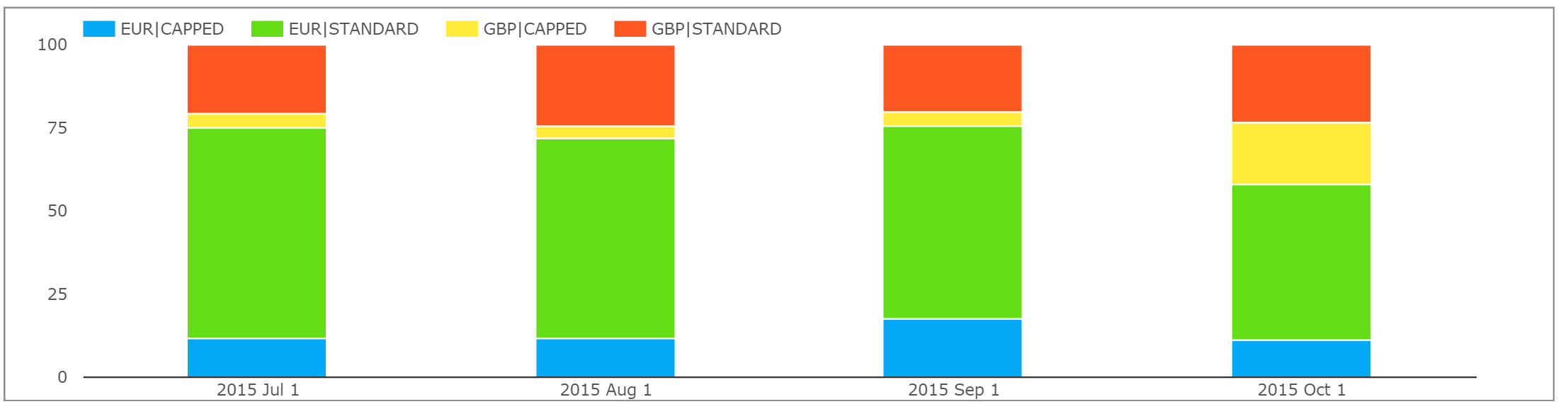

From that chart, the most significant story during October seemed to come from the non-USD currencies. In particular, take a look at the relative percentage of EUR and GBP capped trades last month:

Thanks to a huge increase in GBP capped trades, we saw GBP trades nearly match EUR IRS trades in DV01 terms. Now, granted, this is not the whole market (come on MIFID II…) but it’s still a large chunk of business – much of which I guess was done as RFQ thanks to the aforementioned NARL concerning block trades. In such a small and concentrated market as GBP swaps, you can bet those were sent as RFQ1 trades as well to “minimise” information leakage….

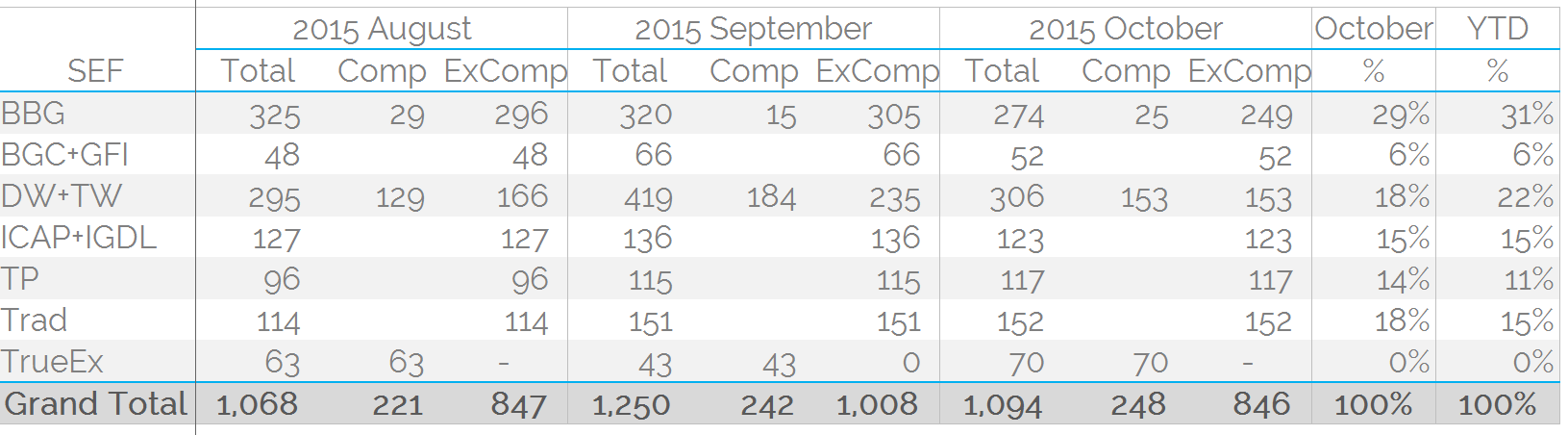

SEF Market Share ex-Compression

From a market-share perspective, there hasn’t been a huge shift this past month but a couple of notable moves are evident in our table below (normal assumptions apply):

- It wasn’t a great month for the D2C/RFQ platforms. I hope our blogs on RFQ didn’t cause this! Both Bloomberg and Tradeweb registered falls in market share of 2-4% compared to their Year-To-Date run rate.

- These falls were picked up by Trads and Tulletts on the whole. This is somewhat surprising given the paucity of CCP Basis we saw trading, and therefore shows a particularly strong performance from these two IDB SEFs in the rest of their businesses.

- However, it doesn’t do much to change the fact that BBG are still number 1, Tradeweb number 2 year-to-date.

- And for the order-book SEFs in IDB land, we see Trads at number one with an 18% market share during October, bringing them level pegging with ICAP on a YTD basis in top spot. Tulletts sit happily in third place, both for the month and year, although they were very close to the ICAP numbers last month.

- It will be interesting to see whether the Icapullets behemoth that is about to be created will rival the D2C platforms for overall number one spot. But I doubt they’ll be offering free EUR swaps trading any time soon!

In Summary

- October was far from a ground-breaking month.

- We saw a decrease in CCP Basis volumes but this didn’t adversely affect the performance of either Trads or Tulletts in the market-share stakes.

- It has been interesting to see that LCH have recently increased their share of client clearing volumes in USD IRS.

- Whilst GBP block trading was particularly evident in the non-USD space.

- The recent extension of the CFTC’s NARL with respect to Block Trading suggests that the current line-in-the-sand between DTC RFQ platforms and order-book driven D2D platforms will be here to stay for some time.

- With the recent price action in Swap Spreads in USD, November looks set to be a completely different story already!

Hi Chris,

Here is a thought about the relationship between UST rates, Swap Rates and LIBOR rates.

The common market wisdom is that swap rates and LIBOR rates are supposed to be the same thing. (Which is why a 5-year ED (Eurodollar/LIBOR) strip in the futures market “used to” add up to the 5 year swap spread). If this is correct, then swaps rates “should” reflect not just rate expectations but also credit expectations about banks. But recently they don’t. Why?

In a “centrally-cleared” interest rate swap market (like we have today) swaps no long have a credit component. They are just derivatives that have no funding or counter party risk whatsoever. LIBOR, meanwhile, does have a credit component because it involves real funding/lending between bank counter parties. Swaps used to have a credit component that “mirrored” LIBOR because swaps were traded bi-laterally between banks in the absence of a CCP. I use the term “mirror” because the bi-lateral credit component of a swap coincidentally created the same credit risk as a funded LIBOR transaction. So my assertion is that swaps no long have anything to do with banks or their creditworthiness. Consider this example: Imagine, Microsoft does a swap with Johnson and Johnson (both AAA credits) and they centrally clear the trade. What does it represent? Purely rates, nothing to do with the credit of banks and it has absolutely no funding component.

Now with regard to swaps vs.UST: UST has funding, swaps do not. Hence, in a world of centrally-cleared swaps the true benchmark for a credit-free and FUNDING-FREE interest rate is not UST but rather a centrally-cleared swap. And if this is correct then the technical and credit factors that relate to supply and demand for assets like UST, LIBOR, Corporate bonds etc. will dictate whether they trade above or below swaps. With this in mind, I believe the next time we have a bank crisis (and we will) LIBOR rates will become completely unhinged from swap rates to reflect the credit/funding components of LIBOR vs. the credit-free/no funding attributes of swaps.

It is also likely that UST will stay above swap rates for the foreseeable future and will only trade below swaps in the event of a credit crisis when the demand for UST is temporarily exaggerated.

Very best,

Dick MacWilliams

Managing Partner

Vista Capital Advisors