- €STR now accounts for 32-59% of risk traded in EUR Rates markets.

- This transition has been led by OTC markets so far.

- Three major exchanges have now launched competing €STR futures contracts.

- CCPView data assesses where the trading is happening.

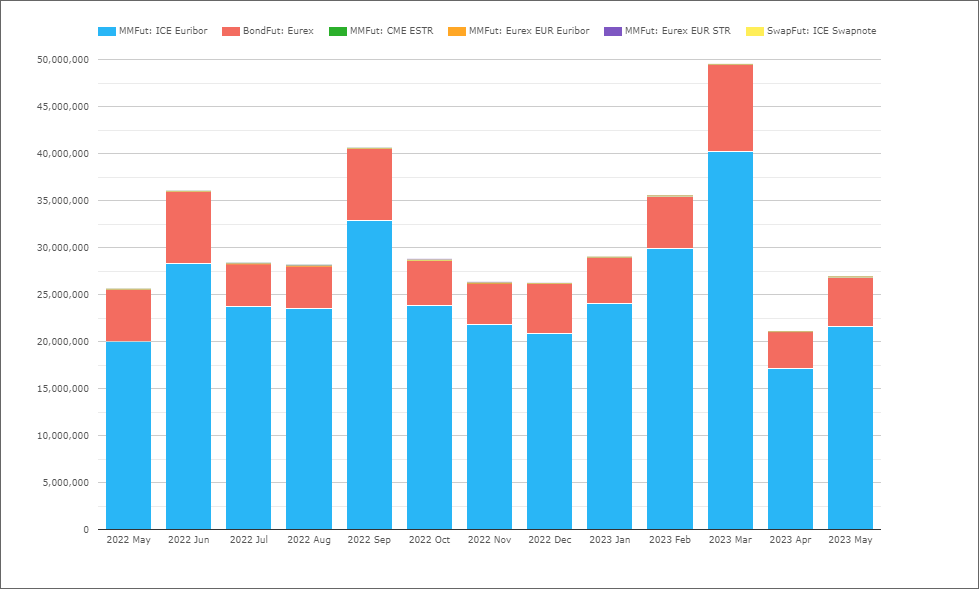

There are extremely liquid markets in a number of EUR-denominated interest rate futures. If you don’t already know your Bund from your Bobl or Schatz then please read our primer “Mechanics and Definitions of Bond Futures“. As you can see from our CCPView volume charts, EUR bond futures are a significant portion of EUR futures trading (in terms of both notional and DV01 equivalents traded):

Showing;

- EUR Bond Futures account for anywhere from €4Trn to €9Trn notional equivalent traded each month.

- All of the trading takes place at Eurex.

- In notional terms, they are the second most significant contracts.

- They are only beaten in notional terms by EURIBOR futures.

- EURIBOR futures continue to be a beast. Average Daily Volumes were €1.1Trn equivalent in 2022, rising to €1.2Trn so far this year.

However, our eagle-eyed readers will have noticed the appearance of some new “slithers” of volume on the charts. And that is what we want to look at today – the new €STR futures.

€STR Futures – Eyes on the Prize

There are now rival offerings from the big exchanges to attract trading liquidity in €STR-linked futures contracts. I guess that comes as almost zero surprise to readers of this blog! Similar to how we saw SONIA and SOFR-linked futures develop, we have three different offerings out there for €STR:

With only ICE offering 1 month futures, it looks like my own personal nirvana of ECB-dated €STR liquidity is unlikely to be developing any time soon. No matter what a washed-up swaps trader thinks, obviously 3 month IMM dated contracts is where the liquidity is most likely to develop.

Competing offerings such as these really shed light on the value of CCPView data. So far, I haven’t been able to find any evidence of traded volumes in the ICE contracts – which seems a bit strange? They are the incumbent in EURIBOR liquidity, so I naturally expected to see some larger volumes than “zero” on their website:

With the ICE three month €STR contract only launched a few weeks ago (end of March I believe?) we are likely to see those numbers change.

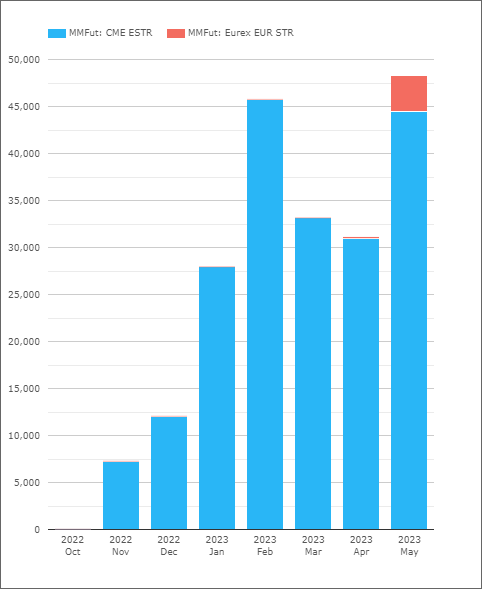

What we can see in CCPView is the successful launches at both CME and, most recently, Eurex:

Showing;

- It remains early days in terms of size of activity in €STR futures.

- However, May 2023 was a “record month” . The chart above shows the number of contracts traded, just to mix up our charts a little bit.

- The Eurex launch helped €STR-linked futures reach almost 50,000 contracts traded.

- To convert to notional-equivalents, we simply multiply by €1m face value of the contracts, so we are almost at €50bn equivalent in a month.

Whilst I am sure no exchange will be jumping up and down in excitement with monthly volumes of 50,000 contracts, it is a start. For reference, EURIBOR contracts trade well over 25 million contracts in most months!

However, I think that the underlying trend we see in Swap markets is particularly interesting in the context of these new €STR contracts.

€STR Swap Liquidity

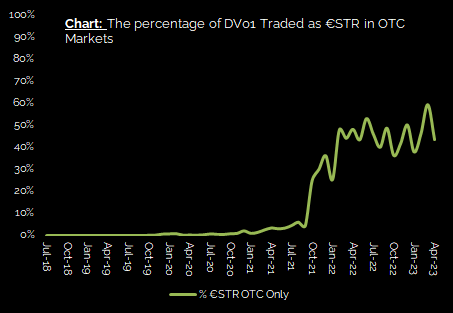

As we have been highlighting in our recent RFR Adoption Indicator blogs, EUR €STR trading is becoming more and more popular:

Showing;

- 32% of all EUR risk was traded versus €STR in March 2023.

- Remember that there is no regulatory mandate to move trading to €STR from EURIBOR.

- This 32% reflects trading across both Swaps (OTC) and Futures. Given the nascent state of the €STR futures market, plus the on-going size of EURIBOR trading, this all points to a signficant portion of the EUR Swaps market now adopting €STR as their preferred liquidity pool.

Looking therefore at the Swaps market component of the RFR Adoption Indicator, we see the following:

As measured by the DV01 traded in cleared OTC derivatives;

- €STR can account for as much as 59% of risk traded in any given month (March 2023).

- In 2023, the lowest proportion of risk traded as €STR was still almost 40%.

- As we have noted with overall €STR adoption, it is a volatile time-series.

- Clearly non-mandated transition to RFR trading is a complex path to walk.

In Summary

USD markets are now seemingly “over the worst” of transition now that the SOFR conversions have happened in Swaps and Futures at LCH and CME.

EUR markets are treading a different path, with no regulatory-mandated transition away from EURIBOR. OTC markets, on the other hand, are amidst a voluntary transition to €STR as the market standard, with up to ~60% of risk now traded vs €STR.

This is where the futures market gets very interesting. Most trading (virtually all) still occurs versus Euribor futures (at ICE). CME, Eurex and ICE all now offer €STR contracts.

It is early days for trading in these contracts. We will continue to monitor their volumes in CCPView to see where the market chooses to trade €STR futures.