Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

Cristiano Ronaldo couldn’t make Portugal front page news in July, but its’ financial system certainly could.

The worries over the financial soundness of Banco Espirito Santo (BES) began on the July 3rd, but on July 2nd, Portugal issued the largest ever USD issue in the 10 year sector from a sovereign.

The $4.5bn 5.125% 10 year offering was widely seen as vindication that Portugal was finally out of crisis mode. However, the timing of the subsequent BES news highlights the importance of the Portuguese collateral agreements – no bank would offer an un-collateralised 10 year settlement or credit limit for $4.5bn to an entity with such volatile credit spreads.

The issuing body, the IGCP, were quoted as saying that the cost of issuance – around 5.225% in USD terms – was roughly equivalent to their 10 year yield in EUR– approximately 3.63% back then and pretty much where it is back to today (21st July). (For everyone’s sanity, I’ll gloss over the intraday spike to 4% since then!).

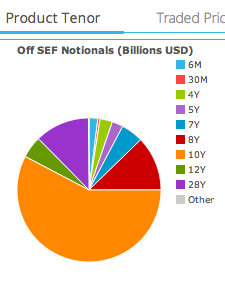

The most obvious evidence in the data for this transaction are the three Fixed/Fixed Cross Currency swaps reported between the 3rd and 8th of July. Using SDR View Researcher and the new Product Tenor View, we can easily see that these 10 year trades make up the lion’s share of Fixed/Fixed Cross Currency activity in EUR/USD this month:

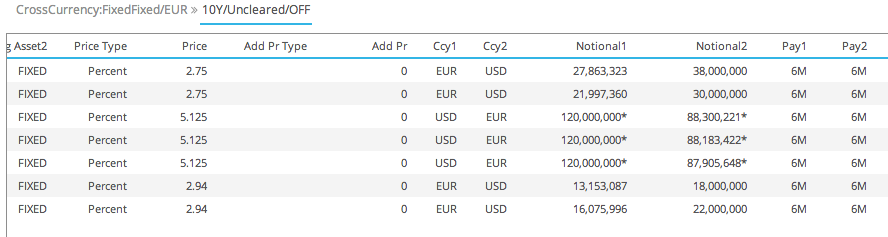

If we drill-down on the 10Y tenor we see:

Three trades with a fixed rate of 5.125% (matches the bond), maturity of 15 Oct 2024 (not shown) and each of these is above the capped size of EUR 120m.

This is particularly interesting as only 6.5% (EUR292.5m) of the whole issue went to investors in Europe. Coupled with the reporting bias towards American counterparties, it is therefore unlikely these are asset swaps from the European buyers.

A couple of scenarios that can explain these swaps:

- IGCP appointed a duration manager for the market risk of the swaps, who later held a credit auction for the exposure to Portugal on the swaps. Whilst the IGCP swaps will (probably) have a reporting exemption, the hedges for the market risks between the banks will be reported. This would explain why the swaps are transacted as late as the 8th July, long after the bond pricing.

- The swaps were done by US asset managers using derivatives to create a synthetically longer-than 10 year Portugal sovereign bond. There is a large gap in maturity for outstanding PGBs between the February 2024s and April 2037s. Artificially creating an October 2024 position will allow fund managers to get closer to a benchmark ten year maturity.

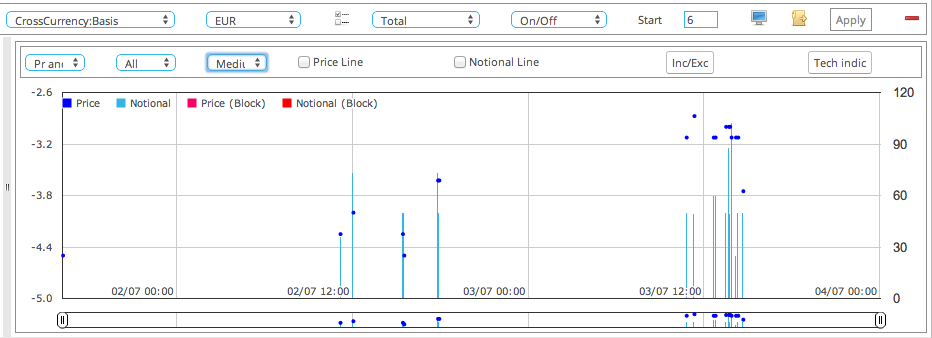

In terms of the market risk itself, we can see in SDRView Pro using the Intra-Day Price chart that the market struggled to digest $4.5bn of 10 years in Cross Currency space, as 10 year EUR-USD moved consistently higher between the 1st and 3rd of July:

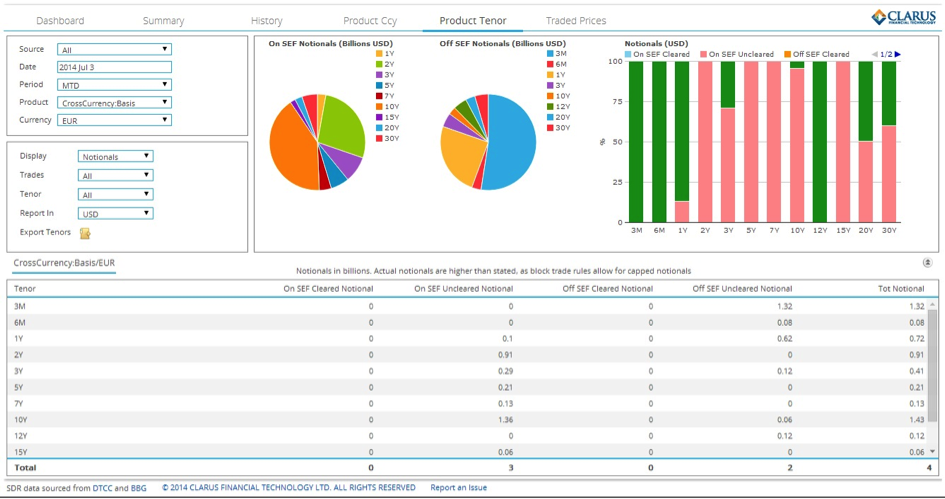

And that 10 year EUR/USD saw by far the majority of trading in the first 3 days of the month. As per the below, nearly 51% of trades above 2 years were in the 10 year tenor:

Previously, we have looked at such bond issues before; the Oracle issue moved through markets and left its’ indelible footprint in USD Swaps, and the EIB’s bumper USD issue seemed to leave an imprint across all areas of the markets – if you knew where to look.

Portugal is not quite so clear – the majority of the bonds were sold into the US and yet there is no evidence of single-currency asset swap activity – the funds who bought the bonds appearing to be in a yield grab for any USD-denominated sovereign paper. Some managers (maybe) saw value in swapping back to fixed EUR rather than buying the current ten year PGB. But with the sheer size of the transaction, plus the timing of the swaps after the bond pricing, I think we are most likely seeing the results of a credit auction.

It is very much a sign of the times that, even with CSAs in place, IGCP must still go through a credit auction.

I guess the banks couldn’t agree on Ronaldo’s haircut…..