Some time has passed since our last blog on the transition to risk-free rates (RFRs). Here we explore what cleared rates swap volumes tell us about the status of the RFR transition. The volumes also tell us what might be necessary for further material progress.

Key takeaways

- Of the $1,076 trillion notional of 2025 cleared rates swaps volumes, trades based only on RFR indexes were just over 62 percent. Trades based on other indexes were just under 38 percent – a sizable untransitioned minority of cleared trades. Of the 38 percent:

- 1.3 percent will be transitioned by the already planned IBOR cessations in ZAR, PLN, and ILS, the last of which is on 31 December 2027.

- 30 percent would be transitioned by hypothetical cessations of USD FedFunds and EUR Euribor.

- 4 percent would be transitioned by hypothetical cessations of AUD/NZD BBSW, CNY Repofix, and of the SEK/NOK/DKK interbank offered rates (IBORs).

- Only just over 2 percent from nine smaller currencies would then still involve non-RFR indexes.

Prompted purely by the volumes, these hypothetical cessations are, of course, easier said than done.

Read on for the charts and data created in CCPView.

RFR adoption in cleared swaps

CCPs do not always provide index breakdowns of cleared swap product volumes to CCPView. However, with a little adjustment we can get a good sense of RFR adoption from product type volumes. Most currencies’ OIS are based only on RFRs, while fixed-float interest rate swap (IRS), FRA, basis swaps, and zero-coupon swaps are based on non-RFRs. I know of only two currency-level exceptions:

- USD has material OIS volume in FedFunds, a non-RFR.

- INR has both IRS and OIS based on MIBOR, a non-RFR.

For this blog, we exclude inflation swaps, which could never be migrated to RFRs. We also exclude variable-notional swaps and cross-currency swaps, both of which are insignificant in cleared volume.

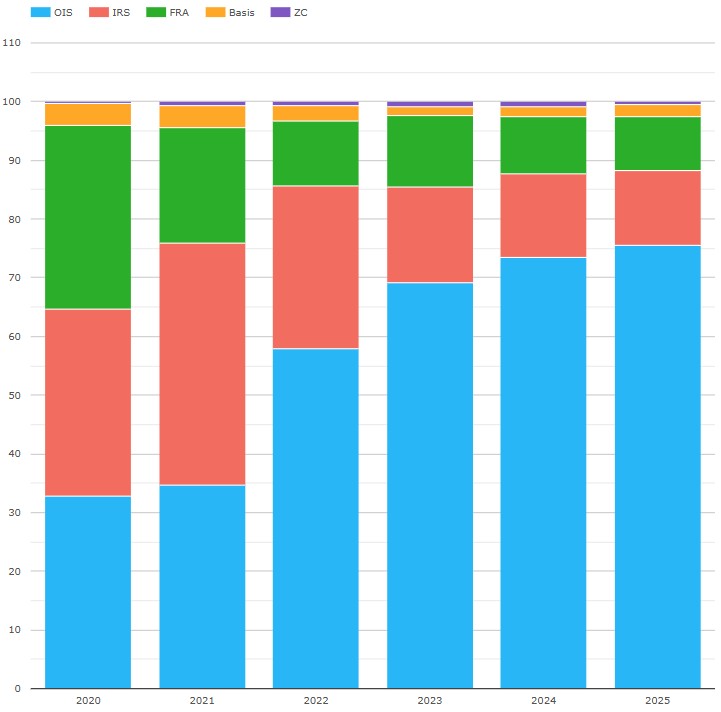

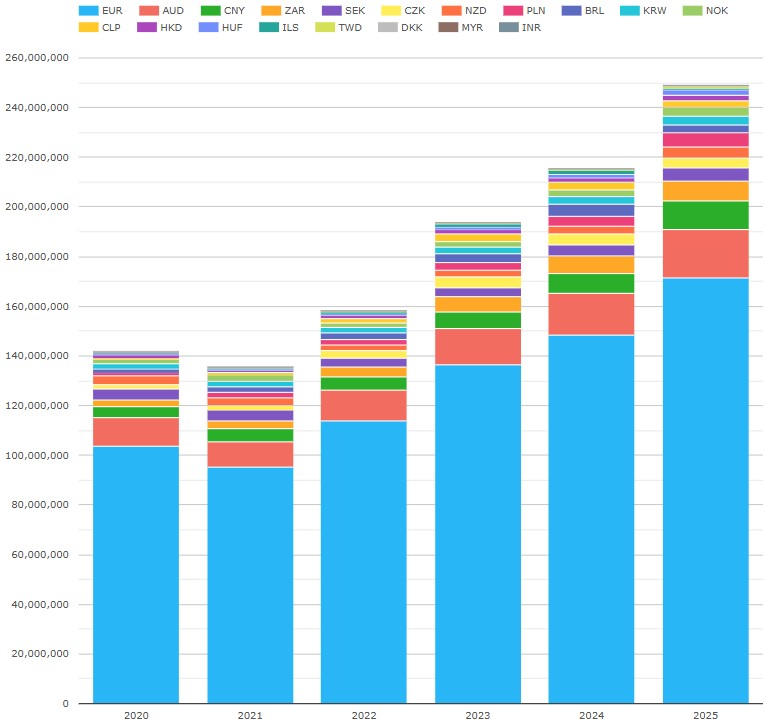

Chart 1: Volume shares by product type of global cleared rates swap products (percentage of USD notional). Source: CCPView

Chart 1 shows that overnight index swaps (OIS) were 75.5 percent of 2025 volume of the five selected products. We treat INR OIS as non-RFR. We also subtract the fraction of USD OIS that is FedFunds-based by extrapolating from SDRView index analysis. This leads to a reduced RFR OIS percentage of 62.3 percent for 2025.

Let’s look at the growth in OIS for major currencies.

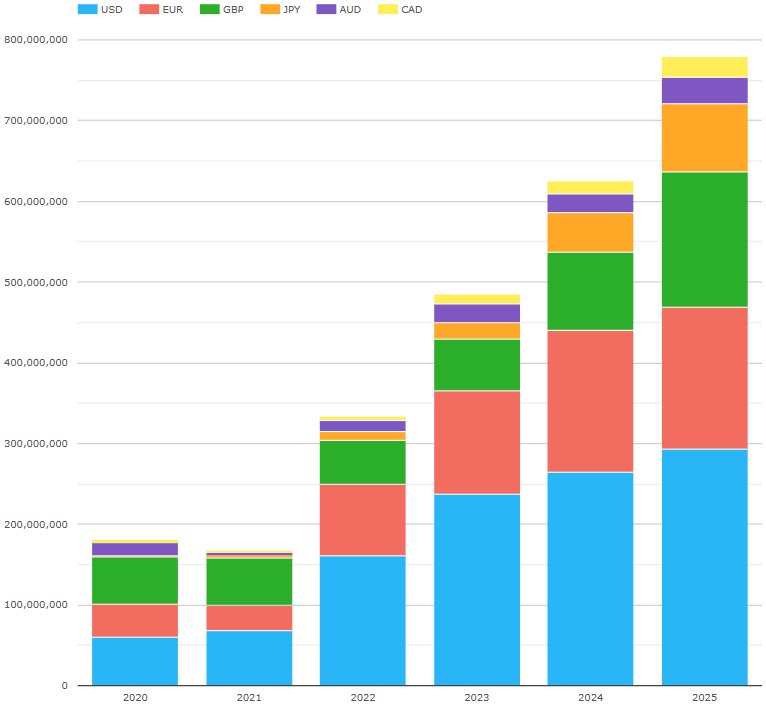

Chart 2: OIS volumes in major currencies (notional USD millions). Source: CCPView

Chart 2 shows that six major currencies grew OIS volumes to $780 trillion in 2025 – up from $182 trillion in 2020, which was based in the main on non-RFRs including EUR EONIA and USD FedFunds.

The first LIBOR cessations were on 31 December 2021. These led to RFR dominance in GBP, with $169 trillion of SONIA OIS in 2025 and in JPY with $84.9 trillion of TONA OIS in 2025.

EUR LIBOR also ceased publication on 31 December 2021. However, EUR Euribor continued publication, leading to Euribor-involved product volumes of $264 trillion in 2025. It was EONIA cessation on 03 January 2022 that established the €STR RFR as the sole basis of EUR OIS. €STR OIS volumes were $175.6 trillion in 2025. With Euribor volume the majority, EUR is not close to RFR-transitioned. There seems to be no current prospect of EU regulators precipitating the transition from Euribor to €STR.

USD LIBOR cessation on 30 June 2023 led to OIS volumes of $293 trillion in 2025, of which $156 trillion was SOFR OIS and the remainder FedFunds OIS. USD is transitioned out of LIBOR, but is not fully transitioned into RFRs. There is currently no prospect of US regulators precipitating the transition from FedFunds to SOFR.

CAD CDOR cessation on 30 June 2024 led to 2025 CORRA OIS volumes of $25.6 trillion.

AUD had no cessation of its IBOR BBSW, which had 2025 volumes of $32.6 trillion.

Overall, the RFR-transition is:

- Materially complete for GBP, JPY, and CAD.

- Partially complete for USD.

- Not started for EUR and AUD.

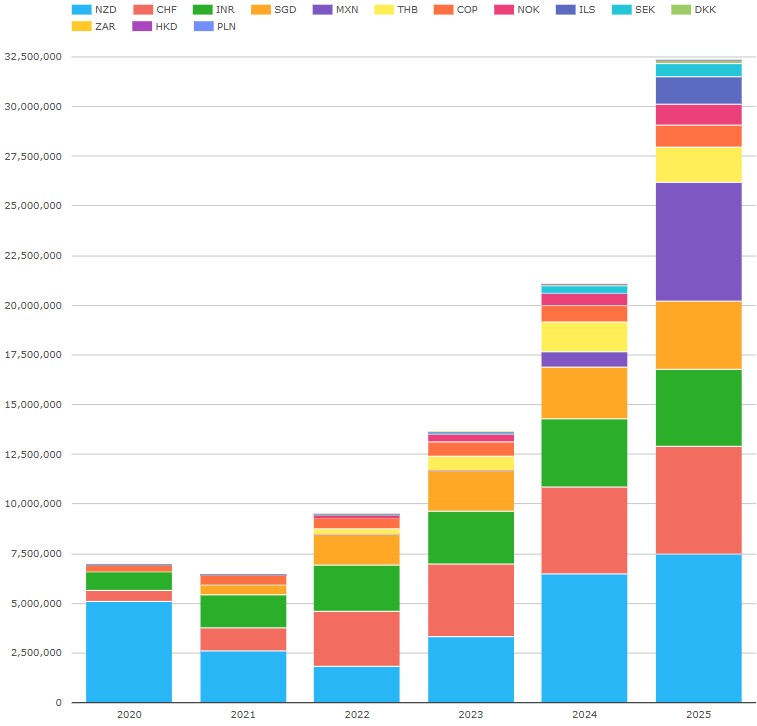

Chart 3: OIS volumes in non-major currencies (notional USD millions). Source: CCPView

Chart 3 shows the visible impact over time of the RFR transitions of CHF, SGD, MXN, and THB on OIS volumes. These four currencies had $16.6 trillion in 2025, up 30x from $557 billion in 2020.

- LIBOR cessation for CHF on 31 December 2021 led to $5.41 trillion of SARON OIS in 2025 — up 9.7x from $556 billion in 2020.

- SOR and SIBOR cessation for SGD on 30 June 2023 led to $3.45 trillion of SORA OIS in 2025 — up 1,896x from $1.82 billion in 2020.

- 28-day TIIE cessation for MXN on 31 December 2024 led to $5.98 trillion of F-TIIE OIS in 2025 — up from zero in 2023.

- THBFIX cessation for THB on 30 June 2023 led to $1.77 trillion of THOR OIS in 2025 — up from zero in 2021.

A couple of other cessations warrant special note:

- MIFOR cessation for INR on 30 June 2023 led to $3.87 trillion of MIBOR OIS in 2025, up 4.1x from $945 billion in 2020. MIBOR is not an RFR and therefore MIBOR OIS is not RFR-transitioned.

- ILS TELBOR cessation 30 June 2025 has so far led to $1.42 trillion of SHIR OIS in 2025, up from zero in 2022. The 2025 figures still reflect TELBOR IRS trades in the first half-year.

Aside from the higher multiple increases in OIS in transitioned currencies and in EUR, currencies with continued publication of an IBOR had $48.3 trillion OIS in 2025, up only 2.1x from $23.0 trillion in 2020.

Non-OIS cleared swap volumes and ongoing RFR transitions

Let’s look first at non-OIS cleared swap volumes in RFR-transitioned currencies.

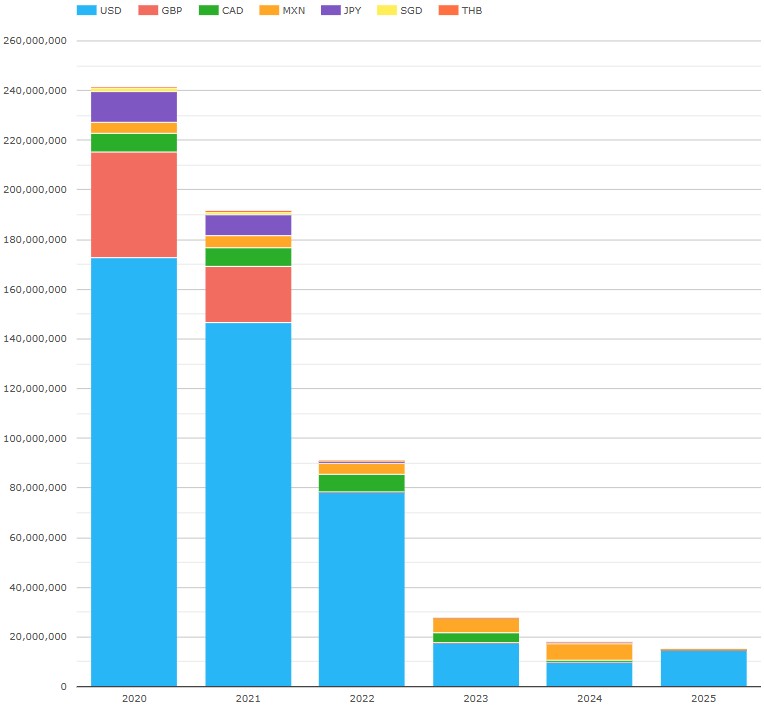

Chart 4: non-OIS cleared rates swap volumes in RFR-transitioned currencies (notional USD millions). Source: CCPView

Chart 4 shows that overall non-OIS volumes in transitioned currencies declined to $14.9 trillion in 2025 – down from $244 trillion in 2020.

- USD was the main residual volume factor with $14.6 trillion (all SOFR versus FedFunds basis swaps).

- JPY had residual volumes of $233 billion (TIBOR IRS) – tiny compared with the JPY OIS volumes noted under Chart 2.

We come to non-OIS cleared swap volumes in non-RFR-transitioned currencies.

Chart 5: non-OIS cleared rates swap volumes in non-RFR-transitioned currencies (notional USD millions). Source: CCPView

Chart 5 shows that non-OIS cleared swaps in the 19 non-transitioned currencies were $248.6 trillion in 2025 – up 1.8x from $141.6 trillion in 2020.

The top three by volume – EUR, AUD, and CNY – had $202 trillion in 2025 and show little sign of regulatory initiative to transition to RFRs.

- EUR had $171 trillion in 2025 (comprising Euribor IRS, FRAs, and Euribor versus €STR basis swaps).

- AUD had $19.5 trillion (comprising BBSW IRS with a side order of BBSW versus AONIA basis swaps).

- CNY had $11.5 trillion (comprising CNY IRS of both onshore deliverable and offshore non-deliverable types).

Three other currencies – ZAR, PLN, and ILS – had $14.3 trillion in 2025 and have full RFR-transitions in progress.

- ZAR’s $8.19 trillion in 2025 will be curtailed by ZIBAR cessation on 31 December 2026 and replaced by ZARONIA OIS.

- PLN’s $5.61 trillion in 2025 will be curtailed by WIBOR cessation on 31 December 2027 and replaced by POLSTR OIS.

- ILS’s $532 billion in 2025 was curtailed by TELBOR cessation on 30 June 2025 and replaced by SHIR OIS.

Voluntary shifts toward RFRs are occurring in CZK, SEK, NOK, and DKK, which had $12.8 trillion in 2025.

- CZK’s $3.95 trillion of IRS in 2025 will see the cessation of two-month and nine-month PRIBOR on 01 April 2025. As other frequencies make up the bulk of PRIBOR IRS, this will not have a significant impact on IRS volumes.

- The Scandinavian currencies (NOK, SEK, and DKK) had $8.84 trillion of IRS in 2025 which shows a voluntary shift in volumes to OIS.

Remaining non-transitioned currencies had $19.7 trillion in 2025. We have not heard of any regulatory initiatives in these currencies to transition to RFRs. These include NZD, KRW, BRL, HKD, HUF, CLP, TWD, INR, and MYR.

I tried to help you see the big picture by pulling together a summary across all currencies and products.

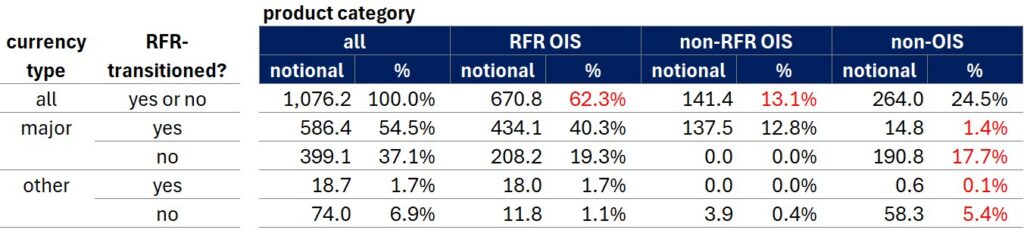

Table 1: 2025 cleared rates swap volumes by currency and product category (notional USD trillions). Source: CCPView, author analysis.

Table 1 shows that 62.3 percent are in RFR OIS (40.3 percent in transitioned major currencies and 19.3 percent in untransitioned major currencies). The remaining 37.7 percent breaks down as follows:

- 13.1 percent are non-RFR OIS (mostly 12.8 percent USD FedFunds OIS with 0.4 percent in INR MIBOR OIS).

- 17.7 percent are non-OIS in untransitioned major currencies (mostly EUR Euribor-involved trades and AUD BBSW trades).

- 5.4 percent are non-OIS in nine untransitioned smaller currencies.

- 1.4 percent is non-OIS in transitioned major currencies (mainly USD SOFR versus FedFunds basis swaps and JPY TIBOR IRS).

- 0.1 percent are non-OIS in transitioned smaller currencies (mostly ILS SHIBOR IRS, which will not recur in 2026).

The ongoing RFR transitions in ZAR, PLN, and ILS would eliminate 1.3 percent of 2025 non-OIS. This would leave 36.4 percent untransitioned, which is best understood by considering what further index cessations would have the largest impacts.

- 15.9 percent in EUR (Euribor IRS, FRA, and Euribor vs €STR basis swaps) would be transitioned by Euribor cessation.

- 14.1 percent in USD (FedFunds OIS and SOFR versus FedFunds basis swaps) would be transitioned by FedFunds cessation.

- 2.2 percent in AUD (BBSW IRS) and NZD (BBSW IRS) would be transitioned by BBSW cessations.

- 1.1 percent in CNY (Repofix IRS) would be transitioned by Repofix cessation.

- 0.8 percent in SEK (STIBOR IRS), NOK (NIBOR IRS), and DKK (CIBOR IRS) would be transitioned by Scandinavian currency IBOR cessations.

Completion of those hypothetical cessations would leave only 2.2 percent in IBOR-involved trades in INR, CZK, KRW, BRL, CLP, HUF, HKD, TWD, MYR.

Making the index cessations I hypothesized happen in practice is no small undertaking. However, it is not clear why the transition imperative is less strong in one currency or index than another.

I’m interested in your views on the currency level pros and cons here.

End note

Skip back to the top to reread the key takeaways if you like.

We used five charts and one table for a full overview of cleared swaps and the status of RFR transition, but there are a lot more data in CCPView.

Please contact us for information on the data products, or for more details on any of the above analysis.