In a recent blog, we looked at the adoption of risk-free rates (RFRs) in cleared rates swaps. Now we explore the same topic for rates exchange traded derivatives (ETDs). What do rates ETD volumes over time tell us about the status of RFR transition?

Key takeaways

- In 2025, trades executed in RFR-based products were 62 percent of the $3,307 trillion notional of the six major currencies’ MM futures, MM options, and swap futures.

- The untransitioned 38 percent were materially made up of ETDs based on USD FedFunds, EUR Euribor, and AUD bank bills.

Read on for the charts and data created in CCPView.

Background

In rates ETDs, RFRs can be adopted into money market (MM) futures, options on MM futures, and swap futures. However, we exclude bond futures and options from our RFR adoption universe because these are invariably based on fixed rate bonds.

MM futures

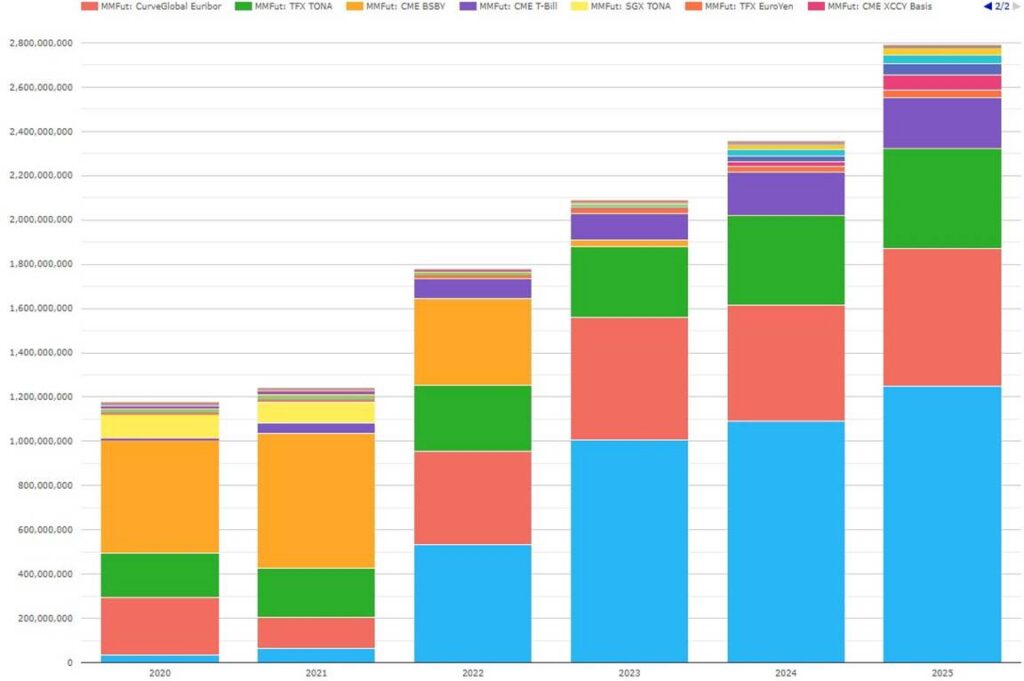

Chart 1: Volumes by product subtype of major currency rates MM futures (notional USD millions). Source: CCPView

Chart 1 shows the shift in the share of total volumes as major currency MM futures transitioned to RFRs aligned with their transitions. Three of the currency transitions are complete. This results in uniformly RFR MM futures volumes totaling $265 billion in 2025.

- After GBP LIBOR cessation at the end of 2023, ICE SONIA took over from ICE Sterling (based on GBP LIBOR).

- After JPY LIBOR cessation at the end of 2023, JPX, TFX, and SGX TONA took over from TFX Euroyen (based on JPY LIBOR).

- After CAD LIBOR cessation in mid-2024, TMX CRA (based on CAD CORRA) took over from TMX BAX (based on CAD CDOR).

- The other three currencies have partial transitions. This results in RFR MM futures volumes totaling $1.38 trillion and non-RFR MM futures volumes totaling $1.14 trillion in 2025.

- After USD LIBOR cessation in mid-2023, CME SOFR (and FMX SOFR) took over from CME Eurodollar (based on USD LIBOR), while CME MM futures on FedFunds (a non-RFR) continued to trade and totaled $621 billion in 2025.

- After EUR EONIA and LIBOR cessation at the end of 2022 (though with no EURIBOR cession), ICE, Eurex, and CME €STR became material. ICE and Eurex Euribor (a non-RFR) also continues and was $492 billion in 2025.

- Given no AUD RFR transition, ASX cash futures (based on the AONIA RFR) declined to $2.36 billion, while ASX bank bill futures increased to 30.2 billion in 2025.

We can break the chart into RFR and non-RFR subsets to show the dynamic more graphically.

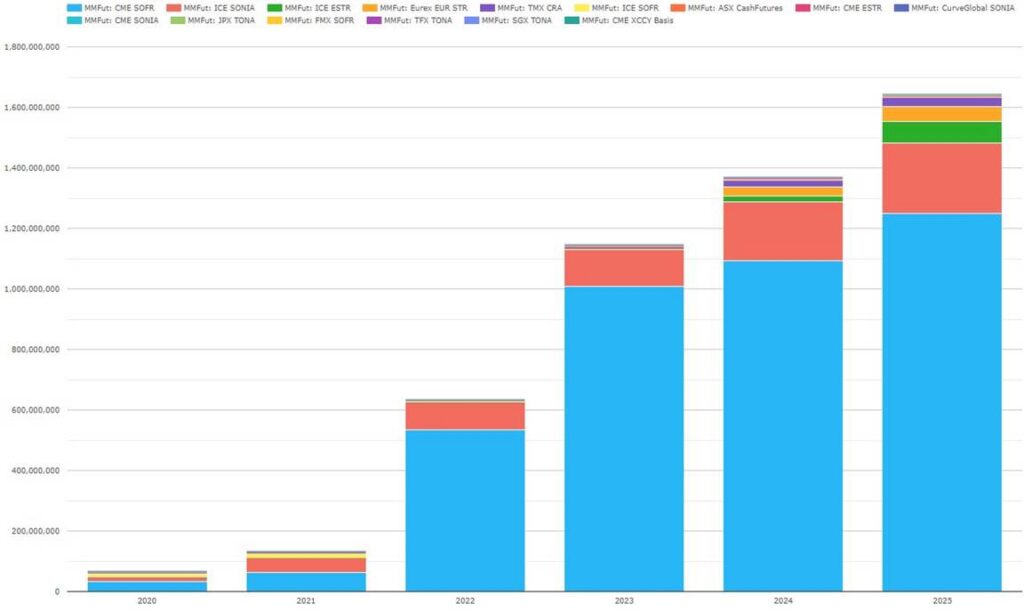

Chart 2: Volumes by product subtype of RFR-based global rates MM futures (notional USD millions). Source: CCPView

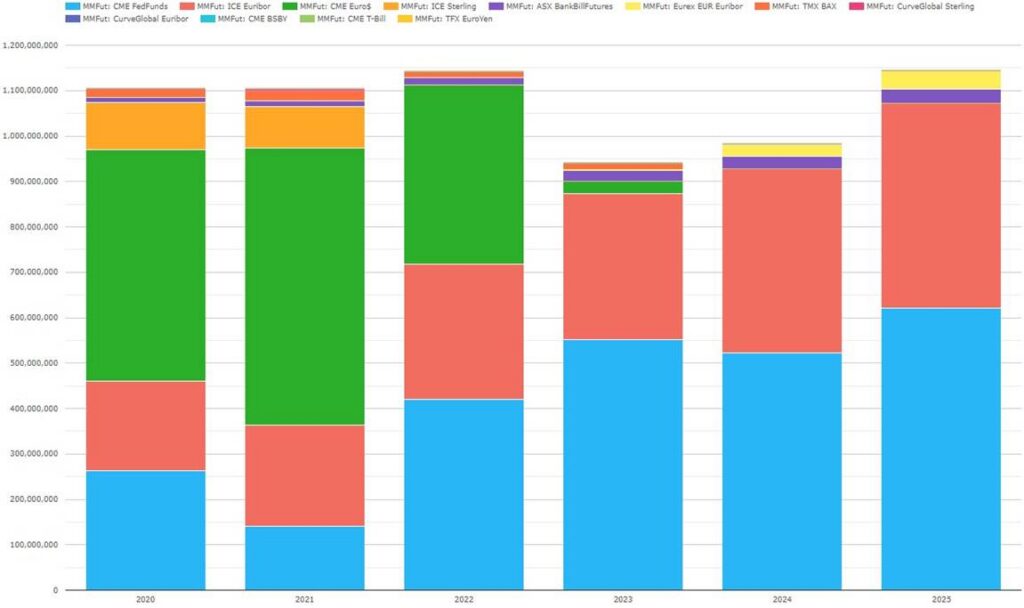

Chart 3: Volumes by product subtype of non-RFR-based global rates MM futures (notional USD millions). Source: CCPView

Chart 2 shows that RFR-based MM futures notional volumes grew from $65.5 billion in 2020 to $1.64 trillion in 2025 – comprising 11 material subtypes across 9 exchange-CCP combinations. By contrast, Chart 3 shows that non-RFR-based MM futures notional volumes barely grew from $1.11 trillion in 2020 to $1.14 trillion in 2025 – comprising 4 material product subtypes across 4 exchange-CCP combinations.

MM options

An MM option (that is an option on an MM future) is based on the same index as the underlying MM future. In practice, this product type is limited to USD, EUR, and GBP currencies.

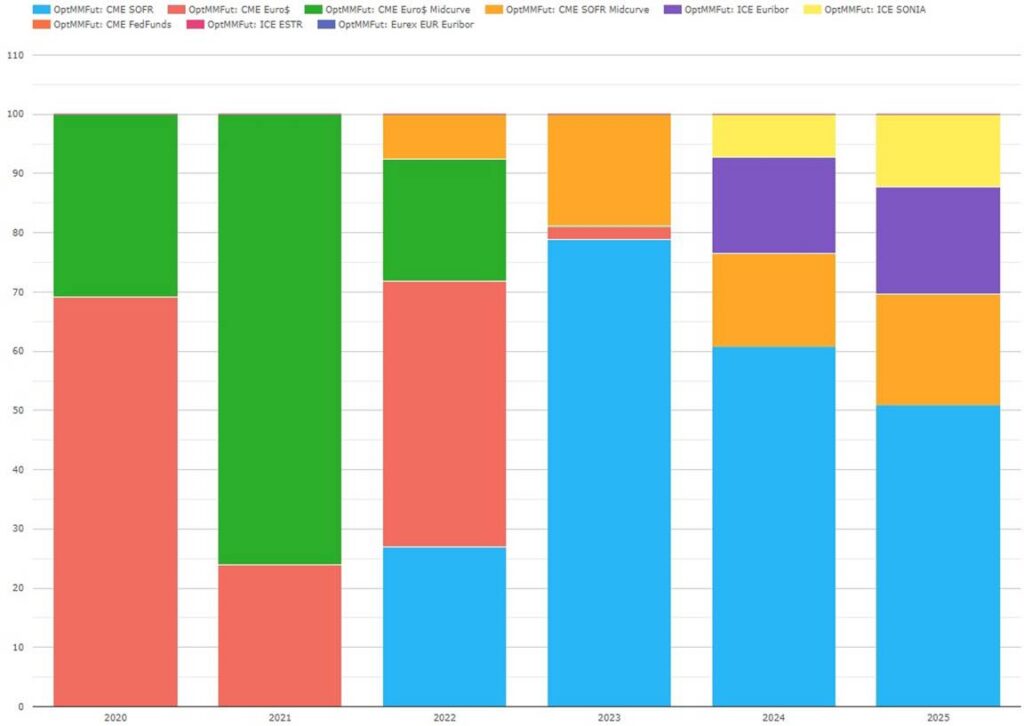

Chart 4: Volume shares by product subtype of major currency rates MM options (percentage of USD notional). Source: CCPView

Chart 4 shows the shift from CME USD Eurodollar futures only in 2021 to futures on three MM indexes in 2024, after only two years of transition in 2022 and 2023.

- CME USD SOFR (70 percent) after Eurodollar was converted by CME to SOFR and stopped trading in Q2 2023.

- ICE EUR Euribor (18 percent) and ICE GBP SONIA (12 percent) both launched in January 2023.

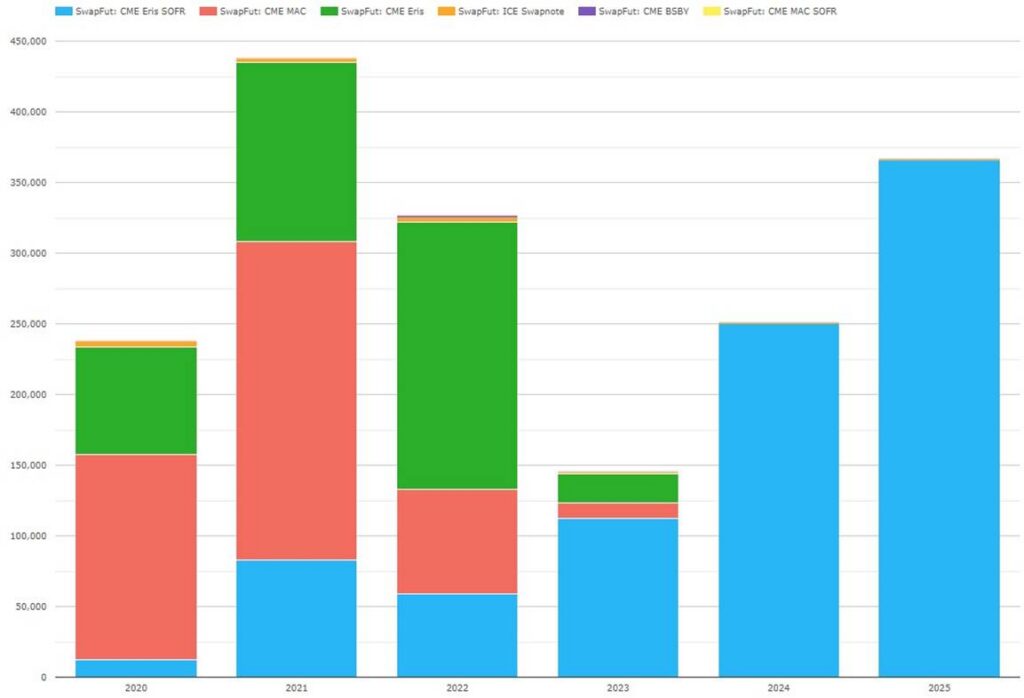

Swap futures

Swap futures are futures with swap cash flows and interest characteristics.

Chart 5: Volumes by product subtype of swap futures (notional USD millions). Source: CCPView

Chart 5 shows the shift from CME Eris SOFR futures (RFR-based) emerging at low volume in 2020 to being the only product subtype with meaningful volume in 2025 with volumes of $366 billion. ICE’s non-RFR based EUR swapnote had only token volume in 2025.

Summary of rates ETD RFR transition

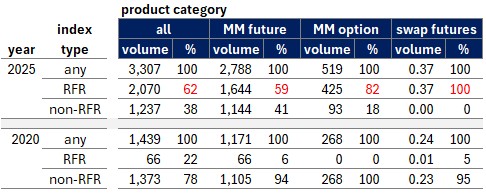

We can calculate a total rates ETD RFR adoption rate by combining ETD volumes from the three sections above.

Table 1: major currencies rates ETD volumes by product category and index type (notional USD trillions). Source: CCPView, author analysis.

Table 1 outlines that in 2025 the six major currencies ETD had a 62 percent adoption rate of RFRs. Adoption rates by product category were 59 percent for MM futures, 82 percent for MM options, and 100 percent for swap futures. This compares with 60 percent for cleared swaps from the recent blog.

To summarize from this blog and our prior blog, swaps and MM futures and options on USD FedFunds, EUR Euribor, and AUD BBSW accounted were the main components of volume based on non-RFR indexes.

End note

Skip back to the top to reread the key takeaways if you like.

We used five charts and one table for a full overview of rates ETD RFR transition, but there are a lot more data in CCPView.

Please contact us for information on the data products, or for more details on any of the above analysis.