A couple months ago, I published an article “SBSDR: The SEC Version of SDR” detailing the generalities of SBSDR – the new trade repositories intended to capture securities based swaps such as single name CDS and equity swaps. At the time, there had been no applications by potential candidates. Fast forward to today, and it appears as though ICE Trade Vault has thrown their hat into the ring to process single name Credit Derivatives. You can see their completed FORM SDR and all of the related exhibits on the SEC page here.

Brief Timeline

Before you get too excited, lets try to understand what this means for when we might first see our first single name CDS come out of an SBSDR. Trying to piece together a timeline is not as easy as it might seem but here is my attempt:

- It would seem ICE first filed their form SBSDR on 29 March 2016, amended it 18 April 2016, and the SEC published the notice on 22 April 2016. I believe it’s that 22 April date that has meaning when it comes to when they could be approved.

- For good measure, it was published in the federal register on 28 April but the appropriate certification clock seems to be on the notice date, not the register date.

- By law, the SEC has 90 days to grant registration or start proceedings to determine if registration should be granted. These proceedings need to be completed within 180 days, but can extend another 90 days if the SEC deems necessary. By putting out the request for comment on 22 April, I take that to be their “proceedings”.

- If you add this up, 180 days from 22 April is 22 October (perhaps slipping to 22 Jan 2017?) and if you add the 6 month compliance lag time for participants to comply with a certified SBSDR, that takes you to 22 April 2017 for the first INBOUND trade reports to happen.

- Then – we’re not done yet – another 3 months before the first public dissemination, so July 2017 to see the first PUBLIC securities based swap report.

I am aware others have quoted a faster timeline, but I am sticking with this one.

Interesting Tidbits

I’ve now read all of SBSDR legislation §240.13-n and §242.900 – §242.908, as well as ICE’s submission and their appendices. I have to say, they seem to have their heads on straight, and I trust them to get this right. I am particularly excited about the flags that they have included in their 901(c) Primary Trade information; however I will leave my thoughts on that to another blog on another day (SBSDR Part 3!), as I intend to formally respond to the SEC request for comment, and do not want to front-run the government here.

If you read through the entire ICE application and exhibits, I would broadly classify their filing documents as follows:

- Organizational disclosures, internal governance, financial references

- Policies for the SBSDR and sample forms they would use to request participant information

- Exhibit GG.2 which I interpret as their draft rulebook

- Exhibit N.5 which details every field they propose be reported to the SBSDR by the reporting counterparty

- Exhibit M.2 which discusses ICE Trade Vault fees

Fees

I’d often wondered what sort of revenue an SDR can garner, and frankly whether Clarus should start our own SDR. I was also curious to know what kind of “tax” this whole SBSDR would mean to the market. So I was drawn to the fee schedule. Here is the ICE Trade Vault SBSDR fees:

- Flat $1.13 per $1 million notional

- Fees charged to the clearing agency (for cleared) or both participants (uncleared)

- Minimum monthly fee of $375 (if you have any position)

- No rebates

- No further fees for lifecycle events, helpdesk, etc

- No double-counting / double-charging for swaps previously reported elsewhere.

This fee structure is nice and clean, and mimics the ICE Trade Vault fee schedule for their CFTC CDS Index offering which is $1.13 per million for single name and $0.45 per million for Index trades. (Remind me – why was there ever single name CDS in CFTC SDR?).

As a comparison, the DTCC SDR fee structure for all 5 CFTC asset classes is a monthly position-based maintenance fee. You get 1,000 positions free every month, but that 30 year IR swap will count as a position for the next 360 months, so if it is above your 1,000 free cap, it will cost you anywhere from 40 cents to $3.50 every month, or $144 to $1,260 over the life of the trade.

Bloomberg’s CFTC SDR charges $10 per trade. Very Bernie Sanders-like – “10 bucks a trade”. And the maximum monthly charge is $50,000.

CME’s CFTC SDR fee schedule is also trade based. Participants get 25 free IR, Credit and Commodities reports every month and 1,000 free FX reports per month. Each IR, Credit and Commodity trade above that is $5 and each FX trade is $1.50 (Bernie Sanders might say “Buck Fiddy”). There is a $200 minimum fee per month, and a $250,000 cap per year.

Ongoing Cost to the Industry / (Is being An SDR Lucrative?)

So I thought it worthwhile to see what sort of revenues ICE could expect from an SBSDR venture.

To start with, you need to know the size of the single name CDS market. Without having access to private data, that’s difficult to quantify. In fact, that is one of the arguments for having a swap data repository! It just means that we’re forced to do some back of the napkin math to see how many CDS trades we can expect to see in an SDR:

-

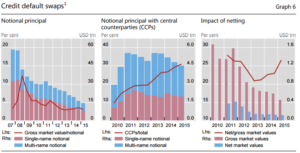

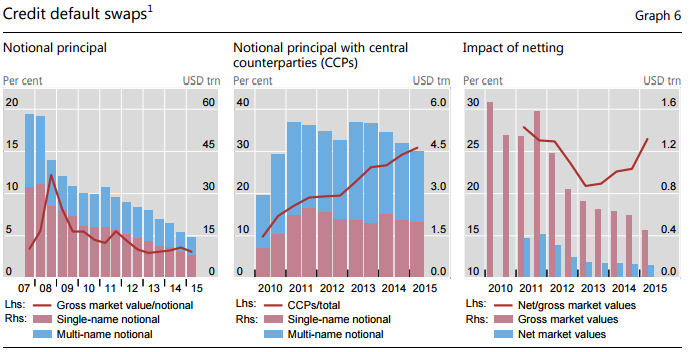

BIS June 2015 Survey The ISDA surveys here seem to only tell us about notional outstanding, so I will skip that.

- The recent 4 May 2016 BIS statistics here seem to also only focus on notional outstanding. But you are able to glean two things from their global data:

- 27% of notional outstanding in total Credit is in the US. Europe is almost double that.

- Single name CDS accounts for 58% of the total Credit notional outstanding of 12 trillion USD.

- The older BIS statistics here seems to roughly mimic those numbers, and are still in notional outstanding. The important thing is this tells us what percent is cleared: 30% as of June 2015 (probably again in notional outstanding terms but I will take it)

- Last year I did a separate back-of-the-envelope estimate that concluded that 15% of the single name CDS market in the US was cleared.

- CCPView tells us there were on average 7,000 single name CDS trades cleared every week last month (split roughly 61/35/4 across ICE US, ICE Europe, LCH).

- CCPView tells us there was on average $31 bn notional of single name CDS cleared every week. Which equates to a seemingly small average trade size of $4.5 m.

-

TIW Weekly Data Table 17, Week Ending 6 May 2016 TIW data tends to require a decoder ring to decipher, but I believe its telling me that there were roughly 17,000 new Single Name trades last week, totalling 181 trillion in notional. This in fact nicely corroborates the story from CCPView and BIS that ~7,000 trades are cleared each week and 30% of the market is cleared. Though it does imply the size of your average cleared trade is smaller than a bilateral trade.

So, if you followed my back-of the napkin math – and I admit its a pretty filthy napkin by now – I feel somewhat comfortable to say:

- Weekly single name CDS Trade activity is ~20,000 trades

- Average trade size is ~10mm USD (with cleared trades being much smaller than bilateral)

- 30% of the market is cleared

Wouldn’t it be so much simpler if we just had actual trades we could look at!? SBSDR couldn’t come too soon.

Now, before we multiply ICE’s $1.13 per million fee x 20,000 trades x 10 to get their projected weekly revenue, we need to adjust that 20,000 trades for how much of it will come under the remit of the US SBSDR rules. Remember that BIS said 27% of the outstanding notional was “US”. I think that is too aggressive to use in our math. I recall the SBSDR rules generally say:

- If a US Person on either side – you need to report the trade

- If cleared by a US Clearing agent – you (the DCO) needs to report the trade – and of course ICE clearing house will report to ICE Trade Vault

- Some confusing language about registered swap dealers / swap participants but that are not US persons (they need to report too, but the data will not be publicly disseminated)

Frankly, I have to guess here. How much of the CDS market is touched by a US Person? Is ICE Clear Europe a US Person? Is Asia really insignificant in CDS? Will non-US dealers register with the SEC?

So lets assume everyone is a US Person:

$1.13 fee per million X 20,0000 trades per week X Average trade size of 10 million = $226,000 per week

Or just under 12 million dollars per year. However we also must consider the fact that both sides of an uncleared trade need to pay the fee, so lets add 50% to that, which gives us $340,000 per week. So $17 million dollars per year.

That is if they dominate a market where everyone is considered a US Person. So not likely. Probably more like a quarter of the market touching a US person, so perhaps $4 million per year. Frankly, because ICE are the dominant clearing house for CDS and hence will have to report all cleared trades executed on venue, they probably think it’s better to have $4 million in revenue per year than to have to pay SBSDR fees to another SBSDR!

If anyone sees flaws in my math, please let me know. Otherwise I am sticking with it.

Summary

Securities based swap trade reporting is coming. Just when is up in the air but the action starts anytime from later 2016 to mid 2017.

ICE have submitted their application, and it is very thorough. Their fee structure would seem to not inhibit the market; the implied “tax” to reporting counterparties is on the order of $4 million per year to the market as a whole. Of course this $4 million does not include the presumable billions in costs to conform with the regulations. But I am optimistic that outside of the major banks, and particularly for cleared trades, its less of an impact than the first (CFTC) SDR implementation.

And just think of the benefits – we will finally be able to play with real trades and get rid of our filthy napkins.

Lastly, I again ponder whether Clarus should start our own SDR. We’re a mean and lean fin-tech firm, we could do it. But of course we’d have to hire lawyers and lobbyists to chase down that $4 million per year revenue. Let us know what you think, I bet we could arrange a discount to $1.12 per million for you!