Given that it is now one week since the first of the IRS Package exemptions expired on May 16, I thought I would look at the data.

We know from our blog, SEF:Week 32 (Final Week Before Packages) that from May 16, the first of the package types, those where all components are MAT, are no longer exempt. This means that Swap Curve strategies , Swap Butterflys and Unwind/Offset packages.

Recall that IRS Swaps that are MAT can be seen on the CFTC site.

Lets start with some Charts.

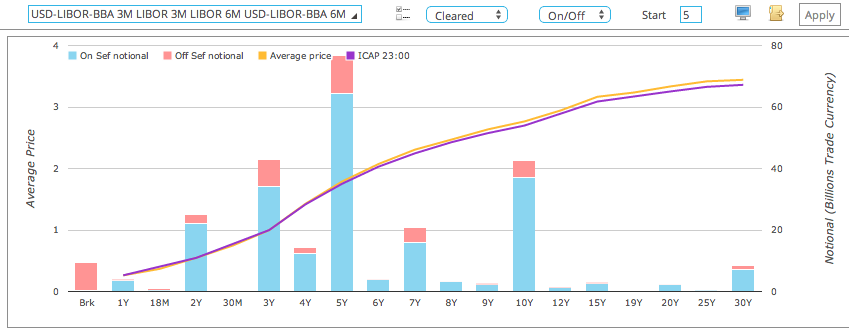

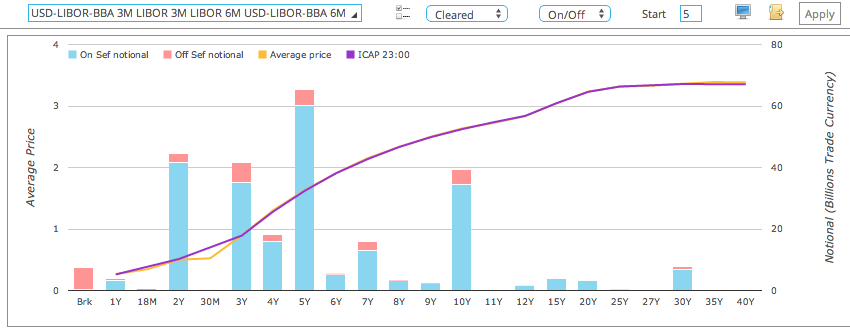

USD IRS Spot Starting Swaps

Focusing only on the Libor 3M & Libor 6M indices that are MAT.

First for the week of April 28 to May 2, our comparison case, lets see what SDRView Professional shows.

Then the week of May 19 to May 23, the first week post package exemptions.

We don’t need to look too carefully to see that there is less red (Off SEF) in the second chart.

So far so good. But how do the numbers stack up in more detail?

On SEF vs Off SEF tables

Which shows a significant reduction between the two weeks, with:

- Off SEF Trade count dropping from 576 to 398

- Off SEF Notionals dropping from $48.9b to $34.7b

- Meaning that On SEF is now 87% vs 81% in notional terms.

If we were to look at specific tenors. for example the major 5Y one, we would see an even higher On SEF of 92%.

So, we can re-iterate our so far so good.

Which Exemptions are expiring next?

June 2, we have packages where one component is MAT. We don’t expect that to alter the percentages much.

June 16, spreads over treasuries. This we do expect to alter the percentages. And we wait to hear how SEFs will tackle the requirement to simultaneously execute the treasury trade and the swap.

November 16, invoices spreads (swaps vs futures).

What is the larger picture?

Now we have focused our analysis on the liquid spot starting swaps that are MAT.

We could also look at forwards on IMM dates and MAC Swaps, both of which are MAT. But there is not much volume in these, so will leave that to another day.

However what of the the other types of swaps? The forwards that are not on IMM dates (there are lots and lots of these). The spot start that are not par but at a spread to the floating rate (there are some of these).

We are currently working on a specific view for forwards in SDRView Professional, which I plan to write about in the next week or two.

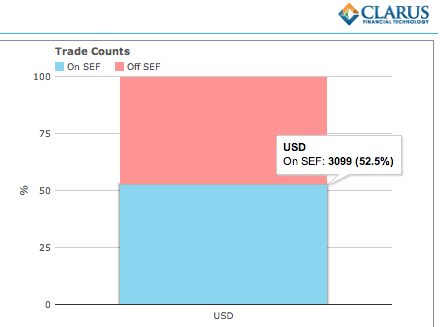

In the meantime lets look at at a chart of all USD IRS FixedFloat in the week of 19 May to 23 May.

Which shows that 52.5% in trade count terms of all USD Swaps executed last week were On SEF.

I think that is pretty good.

But I leave you to draw your own conclusion on that.

Summary

The ending of the May 16 Package exemption has led to an increase in On SEF trades.

The percentage for spot starting swaps has increased from 81% to 87%.

The next dates are June 2 and June 16, the first of which may have little impact but the second certainly will.

Overall just over 50% of USD fixed vs float Swaps are now traded on SEF.