Japan has joined the SEF party with their own flavor of trading venues known as Electronic Trading Platforms (ETP’s). ETP’s launched last week on Tuesday, September 1st. Amir had written about them back in April.

Some rules have since been tweaked, and of course we now have some data. Lets have a look at everything.

Who Has To Use ETPs?

It seems that the “SEF” rules in Japan have been greatly whittled down:

ETP’s are only required when both parties are Japanese Persons (both parties are banks and over the 6 trillion JPY notional outstanding threshold). Trades between a large Japanese bank and a UK bank, for example, can be traded away from ETP.

ETP’s are only required when both parties are Japanese Persons (both parties are banks and over the 6 trillion JPY notional outstanding threshold). Trades between a large Japanese bank and a UK bank, for example, can be traded away from ETP.- Product set limited to 5, 7, and 10 year JPY LIBOR. Importantly this does not include domestic Japanese TIBOR, which is tied to most domestic lending). Nor does it apply to any flavor of basis swaps between LIBOR and TIBOR.

- Any trade that is part of a spread or butterfly is exempt from ETP. So a 2y v 5yr spread trade – even though it has a 5yr leg in it – does not have to be done on or reported by the ETP.

- Other more common things like amortizers being excluded. It really is just basic, interdealer 5, 7 and 10yr LIBOR.

Who Are The ETPs?

For those of us that follow SEF’s closely, the names should not surprise you. There is really only 1 new company in the bunch – Clearmarkets – and they appear to be launching later in the month. The firms are below, both our short names and their legally registered names in Japan:

BGC -> BGC Shoken Kaisha Limited

BBG -> Bloomberg Trade Book Japan Ltd

Clearmarkets -> Clear Markets Japan Inc.

ICAP -> Totan ICAP Cp., Ltd

Tradeweb -> Tradeweb Europe Limited

Tradition -> Ueda Tradition Securities Co.,Ltd.

Tullet -> Tullet Prebon ETP (Japan) Ltd.

Differences to US SEFs

It seems there are many direct parallels in as much as ETPs must do RFQs to 3 firms, and both electronic and voice is permitted.

A couple unique characteristics that I have noticed:

- ETP’s do not report to the trade repository (“TR” – a general term for an SDR). Rather, in Japan, the JSCC handles trade reporting to TRs for all cleared trades.

- The reporting is trade-based, not position based like in American SEFs. This means that each trade has a trade date and time, along with deal specifics like notionals, rates and dates.

- It would seem that all of the ETP’s are publishing intraday. More akin to US SDR trade reporting.

- Trade notionals are capped when above a block size, complete with “+” terminology. For example a notional of “10,000,000,000+” JPY for a 10 year swap, presumably over the 10bn JPY cap size.

Data

We’ve loaded the first week of data into SEFView. No, we do not anticipate an “ETPView” product.

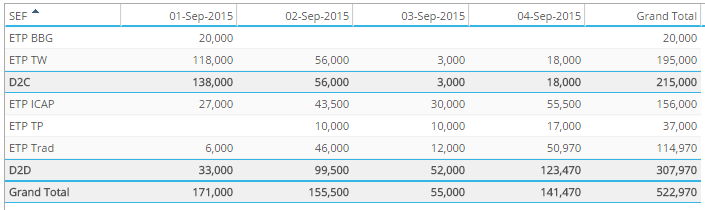

The data is as follows. First, for the ETP notional data:

Out of the 7 anticipated ETP’s, we’re currently seeing data for 5 of them. And we’ve gone ahead and assigned the infamous “D2D” and “D2C” monikers to each ETP, which I believe is fair.

So roughly 130 billion of JPY swaps per day, which translates to just about 1 billion USD equivalent.

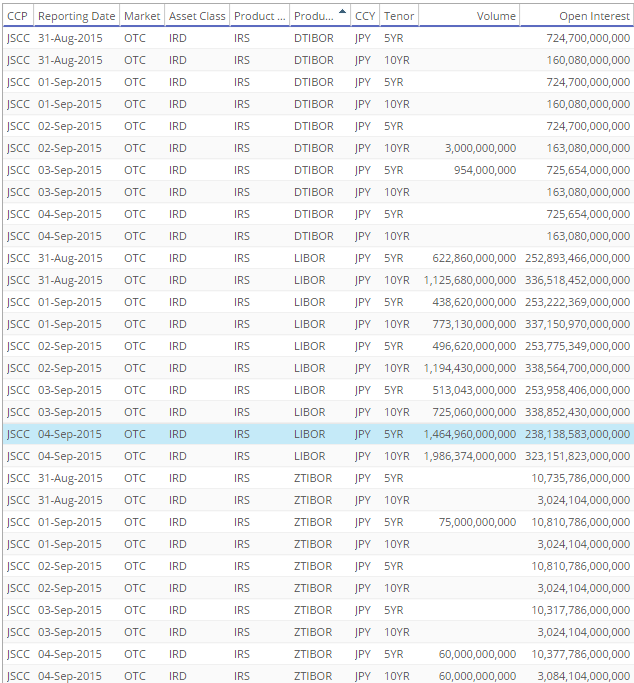

To get a feel for the scale of this activity, we can compare this to the same week in global CCP cleared data:

To be fair, for comparison sake, we can drill down into the cleared data to examine only the eligible JPY swap activity at JSCC:

This tells us a few things:

- JPY Libor is indeed the most active index (over DTIBOR and ZTIBOR).

- Average daily, JSCC-cleared swap activity in tenors between 5 and 10 years is roughly 2 trillion JPY

- The ~523 billion total JPY ETP activity over the first 4 days of September equates to roughly 7% of JSCC-cleared activity in the required Fixed/Float LIBOR tenors

- It is impossible to be precise because JSCC lumps swaps into buckets of 2, 5, 10, 30 and 30+ years.

- The ~523 billion total JPY ETP activity over the first 4 days of September equates to roughly 3% of JSCC-cleared activity in all Fixed/Float JPY tenors and indices

Summary

- ETP’s are live

- 7 Registered ETPs, 5 of them active in first week

- Product and Participant scope seems limited

- Data suggests that only a limited portion of the JPY cleared IRS activity at JSCC is registered on an ETP. Presumably limited by the precise product scope and Japanese Persons language.

That’s all for now but of course we’ll be keeping an eye on the data.