The G20 commitment of 2009 that “all standard OTC Derivative contracts should be traded on exchanges or electronic platforms” has so far only been implemented in the United States where Swap Execution Facilities (SEFs) have been live since October 2013.

In this article I will look at the situation in Japan.

Background

First lets start with a recap of the progress of Regulatory reform in Japan.

The equivalent of Dodd-Frank in Japan is the Financial Instruments Exchange Act (FIEA). An amended version of this FIEA(1) was issued in May 2010 and a further version FIEA (2) in Sep 2012.

Mandatory Clearing of JPY IRS and iTraxx Japan CDS started in Nov 2012 for Large Financial Institutions. This requirement was extended in Dec 2014 to Financial Institutions with outstanding OTC volumes of greater than 1 trillion Yen ($8.4 billion). It will be further extended in Dec 2015 to Financial Institutions with greater than 300 billion Yen outstanding and in Dec 2016 to Insurance companies and Trust accounts.

Mandatory Trade Reporting commenced in April 2013 for Large Financial Institutions and is being extended to other participants. There are three channels of reporting, direct to JSFA, to a registered TR (which is DTCC Japan) or by JSCC for cleared swaps.

SEF and ETP

Firstly the equivalent of SEFs are termed ETPs in Japan, which stands for Electronic Trading Platforms.

The mandatory use of ETPs will start on 1 Sep 2015, covering JPY plain vanilla Interest Rate Swaps and will apply to Financial Institutions with outstanding notional of greater than JPY 6 trillion ($50 billion).

ETPs are required to have an Order Book or Request for Quote to no less than 3 counter parties, but this requirement is not applied to Block trades. Voice will continue to be an acceptable protocol. (A bit of a stretch of the word “electronic”!)

ETPs are required to publish Trade information “without delay”. In practice this may mean reporting to the ETPs website on an intra-day frequency e.g. hourly. This information will exclude counterparties to the trade, but include product, amount, etc.

For block trades the requirement is to publish next day.

Differences to US SEF Rules

The first point that springs to mind is that there is no equivalent of the CFTC Made Available to Trade (MAT) concept where a SEF can propose a product for mandatory SEF execution.

In addition while ETPs will have additional regulation and costs, these will not be as significant as the US. For example Trade Surveillance is not a requirement for ETPs.

[Update: In-fact there are requirements on prevention of unfair transactions and JFSA guidelines for Supervision of Financial Instruments Business Operators. The difference is that these regulations are principles based and not as prescriptive as US ones, meaning that they are likely to prove less burdensome for operators of ETPs.]

So on the face of it, 1 Sep 2015 for ETP may be a softer start than the 2 Oct 2013 was for SEFs, with less focus on pushing market structure change.

Which Firms will launch ETPs?

We think up to eight firms will launch ETPs.

- The IDBs: Tradition, ICAP, Tullets and BGC.

- And Bloomberg, Tradeweb, Dealerweb and ClearMarkets.

Is there room for them all in JPY IRS?

Unlikely as we know from WMBA figures that currently ICAP and Tradition have dominant share.

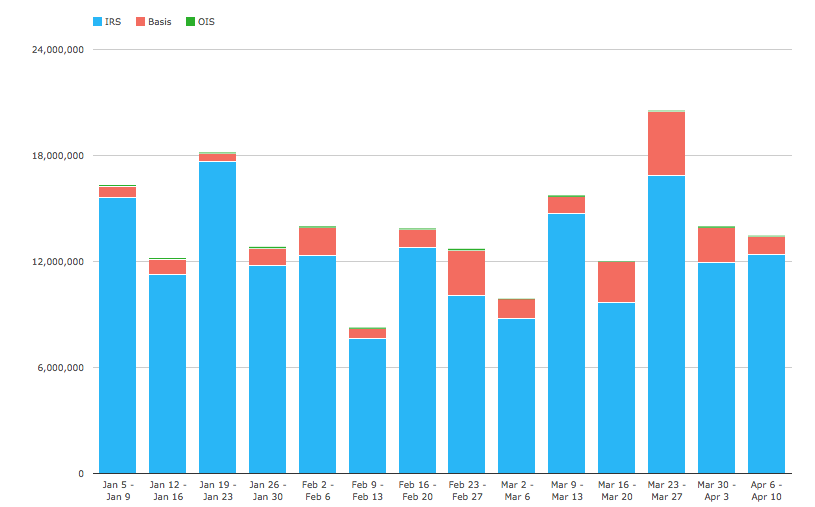

JPY IRS Volumes

The best way to look at the volume and size of market that these firms will battle for is to look at JSCC volumes.

Using CCPView we can look at the year to date weekly gross volumes reported by JSCC:

Which vary from a low of JPY 10 trillion in the week of Feb 9-13 to a high of JPY 20.5 trillion in the week of Mar 23-27.

A weekly average year to date of JPY 14 trillion (USD 118b) or a daily average of JPY 2.8 trillion (USD 23b).

From JSCC public reports we can also see that daily trade counts are in the 150 to 500 range.

So while reasonable volume, certainly lower than what we see in USD SEFs for USD IRS year to date: an average weekly volume of $487 billion or a daily average of $97 billion.

Meaning that the US volume is 4 times larger.

Unless brokerage is materially higher in Japan, it is unlikely that there is room for 8 players in the market.

Of course there are other products and asset classes, in particular FX is a large market in Japan.

Only time will tell.

Summary

In Japan ETPs will commence on 1 Sep 2015.

Large Financial Institutions and plain vanilla JPY IRS will be covered.

Order Book, RFQ to 3 firms and both Electronic and Voice execution.

Pre-trade and Post-trade changes transparency are the key changes.

At least eight firms plans to launch ETPs.

Current JPY Cleared IRS volume is a quarter of USD On SEF IRS.

This volume is unlikely to support the profitability of eight firms.

Thanks Amir. Useful summary. So no mandatory execution at all just regulation of SEFs? Another example of Japanese regulations being commonsense and practical and avoiding going on a mission with questionable rationale (along with not mandating client and non-Japanese banks to clear).

Non-Japanese banks are clearing anyway as a price of access to the onshore market. Clients will clear as soon as the bilateral IM mandates are there.

The only problem is that Japanese banks are limited in their ability to hedge down their bilateral portfolios with other Japanese banks by the dealer clearing mandate. (There should be an exemption for such trades when the two parties are subject to bilateral IM).

All in all a pretty intelligent approach to fulfilling the G20 commitment whilst minimizing unintended consequences of inhibiting systemic risk reduction compared with the more zealous and as a result more misguided markets regulators approaches in the EU and US.

Best

Jon