Please scroll down/click here for the latest updates. This blog covers both Monday October 19th and Friday October 15th in the SOFR market.

LCH SOFR Auction

With the LCH SOFR auction now a matter of hours away, we thought it would be worthwhile updating on the activity in SOFR markets.

Yesterday was an all-time record in SOFR activity, all of it after the LCH updated their auction sizes.

For reference, the auction sizes are now expected to be:

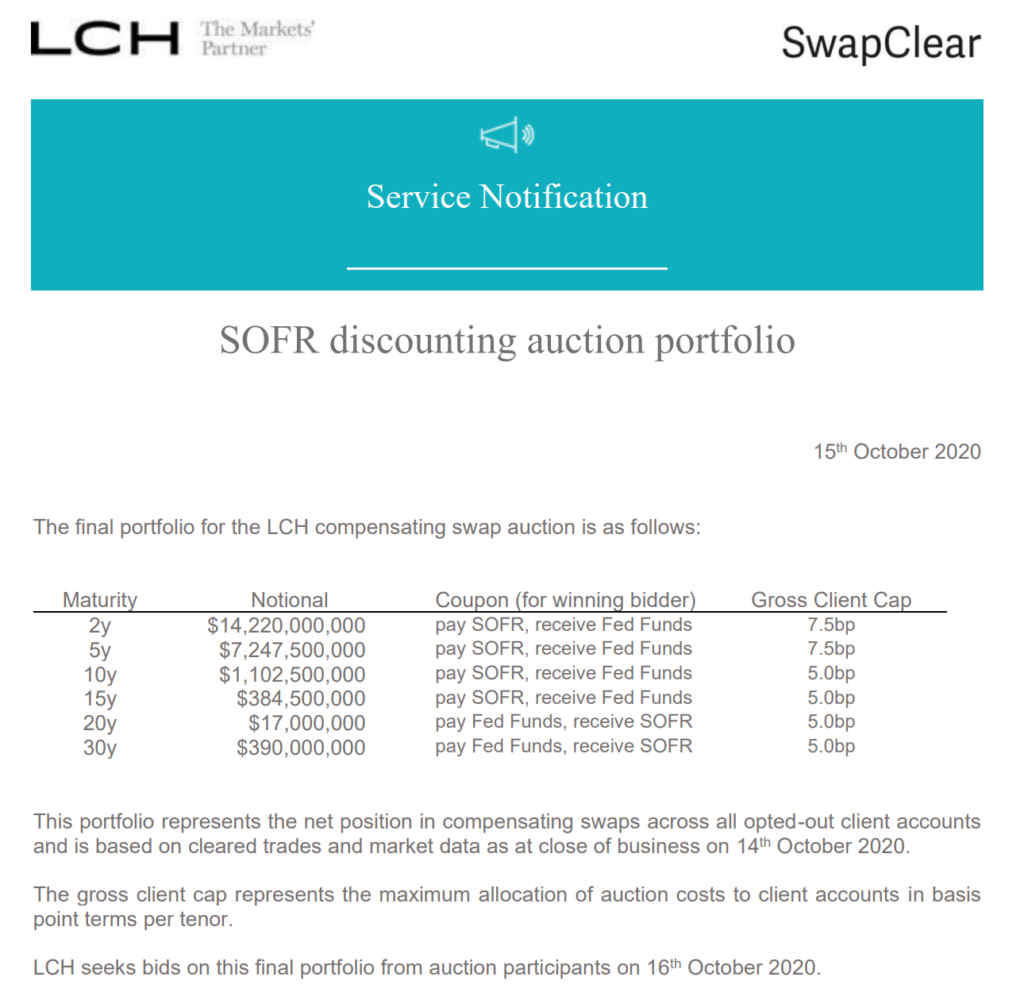

From a DV01 perspective, we calculate the following gross positions:

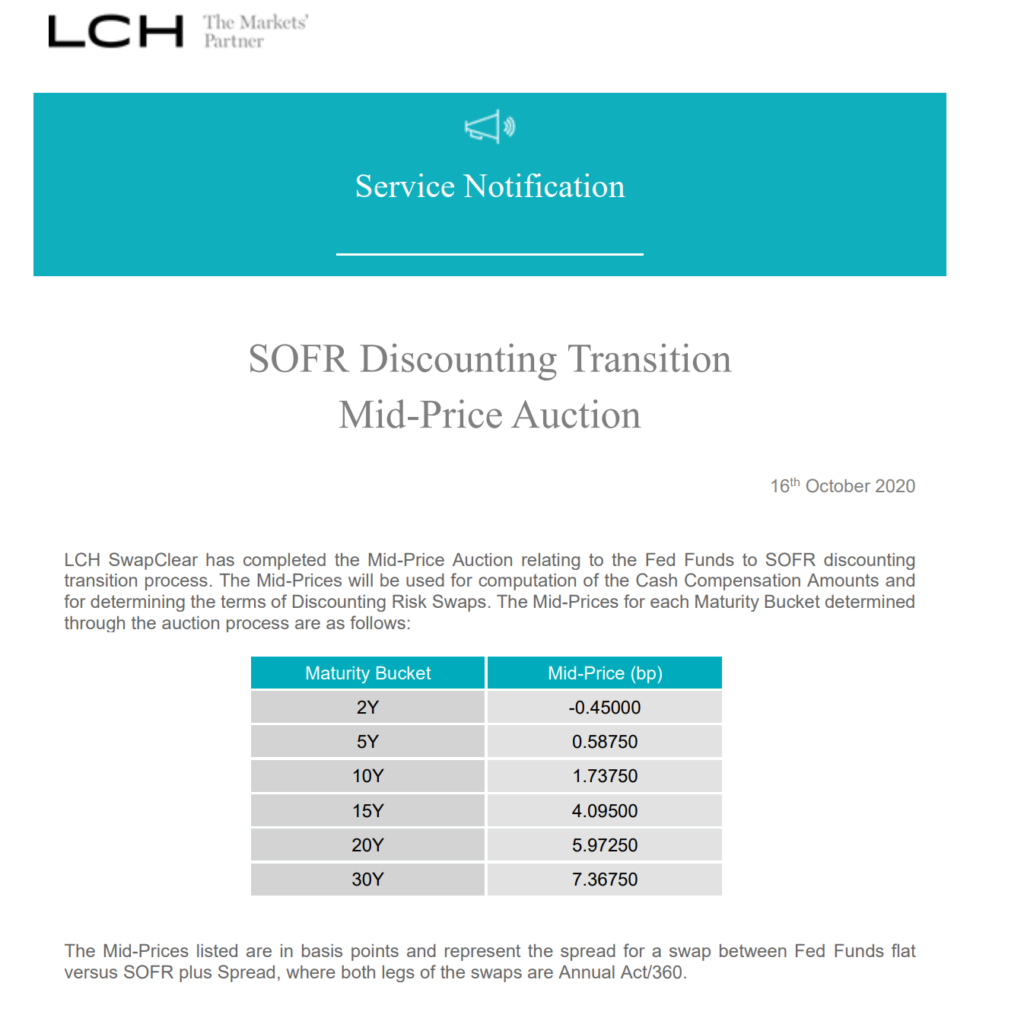

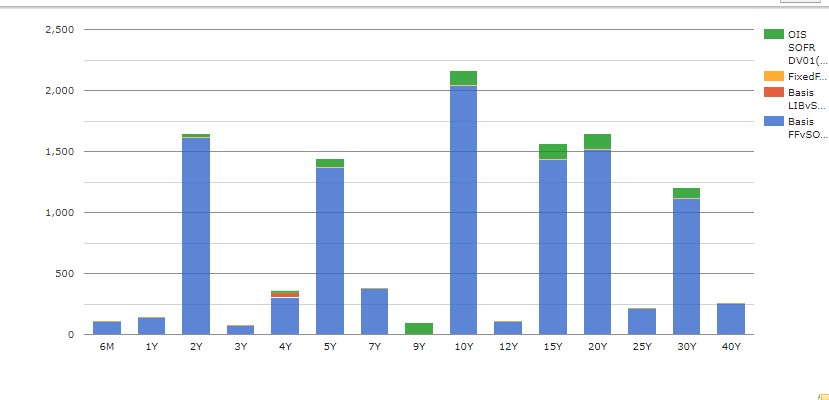

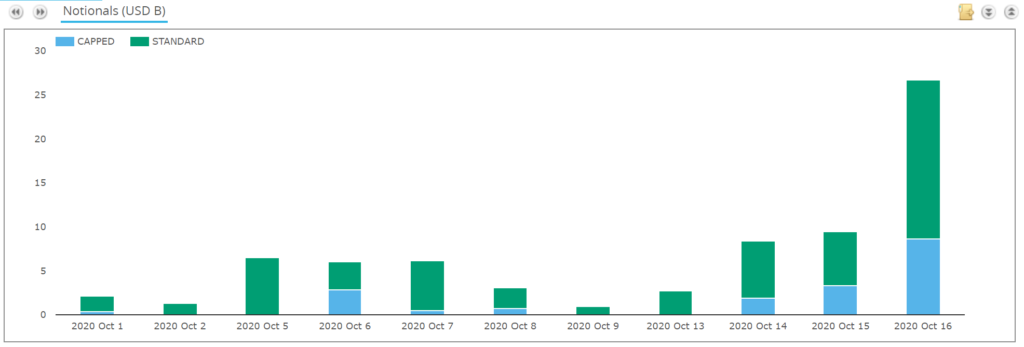

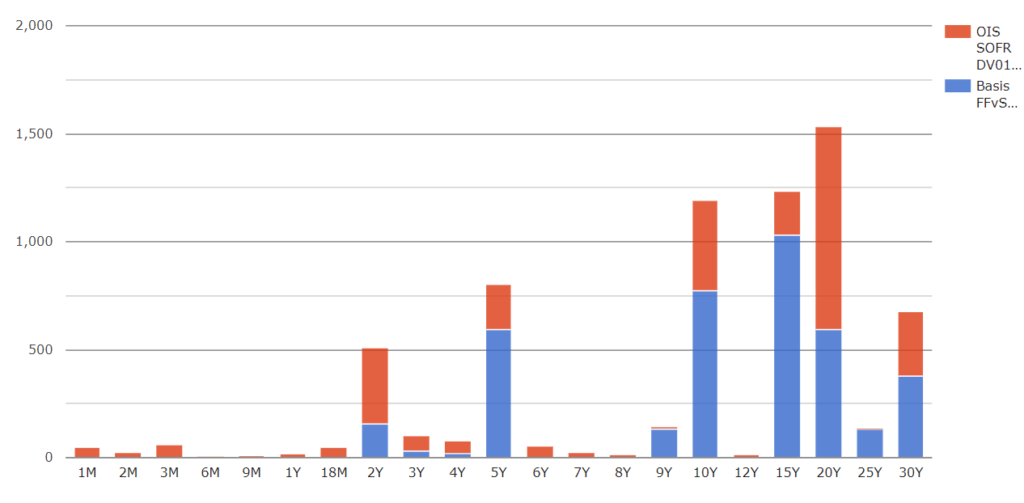

SDR Activity 15th October 2020

That $9m in gross SOFR DV01 is significant (albeit in basis swap positions Fed Funds vs SOFR). Yesterday, Thursday October 15th saw the largest amount of SOFR risk ever reported to SDRs on a single day.

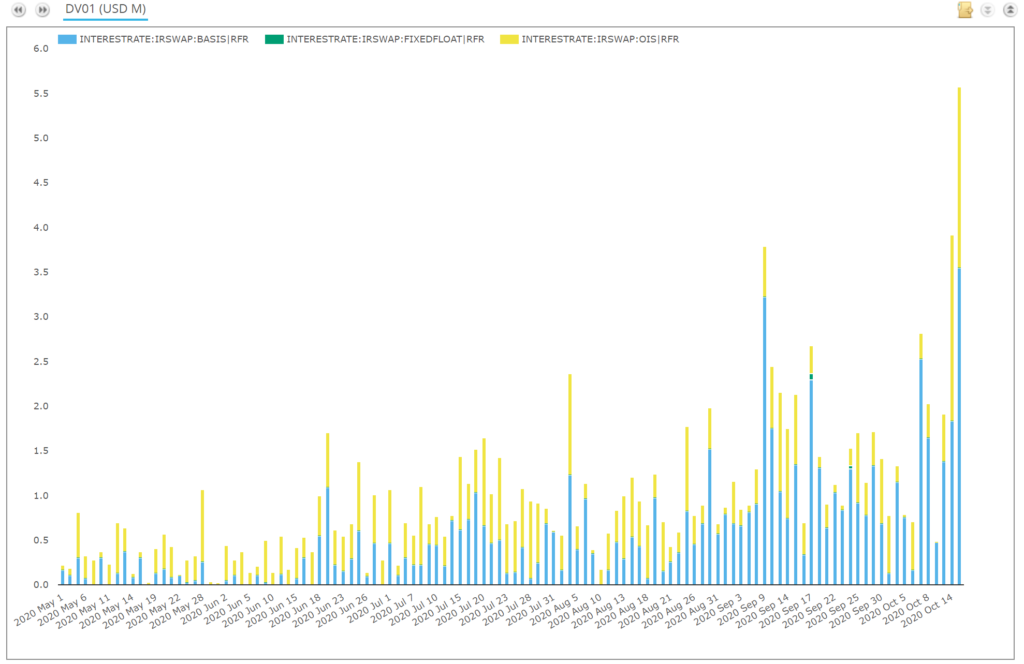

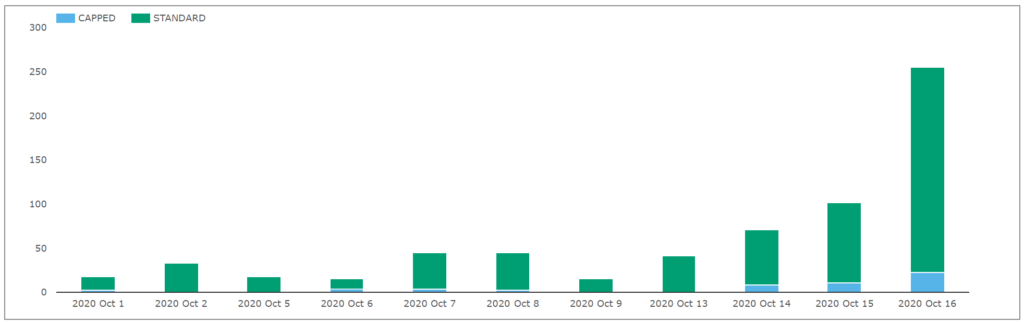

The gross DV01? $5.6m, or about 61% of the auction size. This also included 11 trades above the capped size, so this is only an insight into the minimum amount of risk traded. There were over 102 trades reported yesterday, also an all-time high.

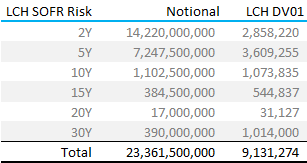

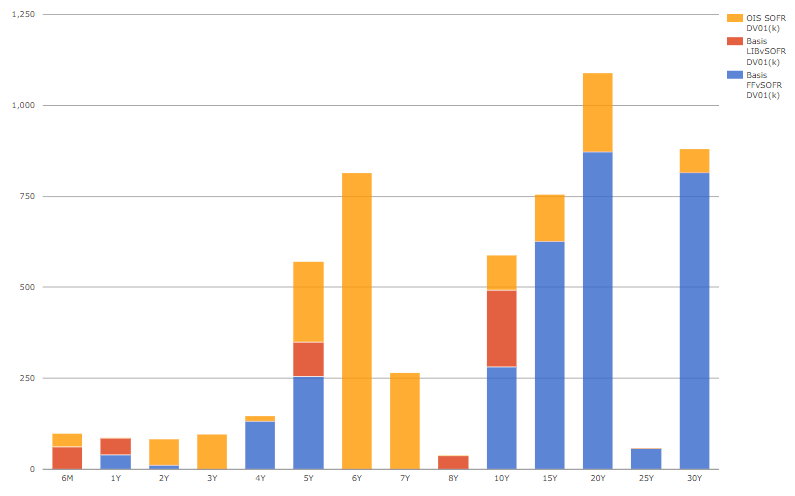

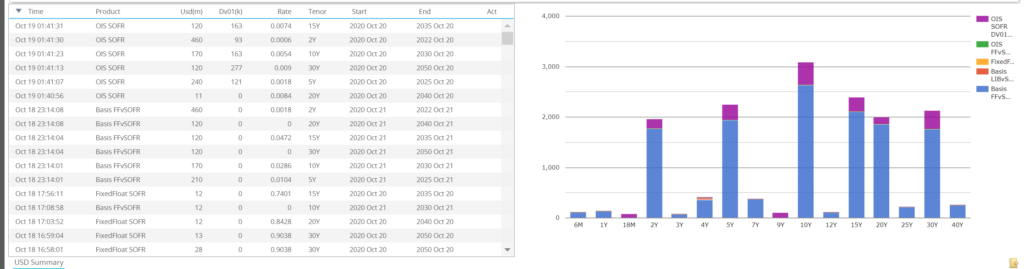

Using SDRView Pro, we can see the exact split of SOFR activity by product type and maturity in real-time. From yesterday:

Showing;

- Activity in SOFR was really concentrated in the long-end.

- 60%+ of SOFR DV01 transacted was 10Y or longer.

- Interesting to note that there was a lot of outright SOFR activity in 5Y, 6Y and 7Y tenors. I thought this was all basis risk?!

- Our expectation that most activity would be in 5Y is falling short.

- However, interesting to note that most of the block trades were ~6Y maturity and at an off-market coupon of 3.3%. Looks strange, right? Difficult to interpret these ones:

We’ll keep our eye out on the activity and periodically update this blog over the coming hours/days.

Good luck to the USD market today!

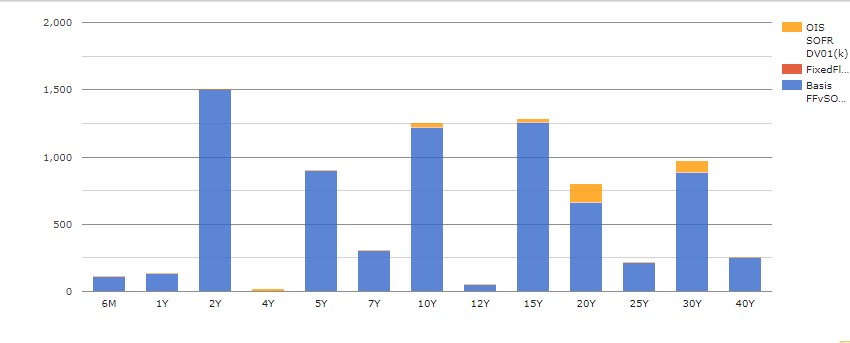

SDR Activity 16th October 2020

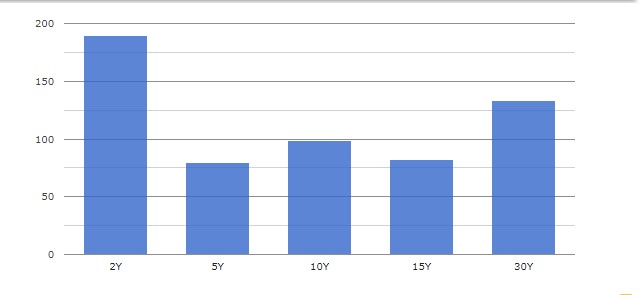

As at 12:38 London time, we see 11 FF v SOFR Basis Swaps reported with a total gross DV01 of $580k in the following tenors.

13:45 Ldn Time 16th October 2020

I guess something is happening? Loads of activity:

- 32 trades now

- $1.8M gross DV01

- $2.4bn notional

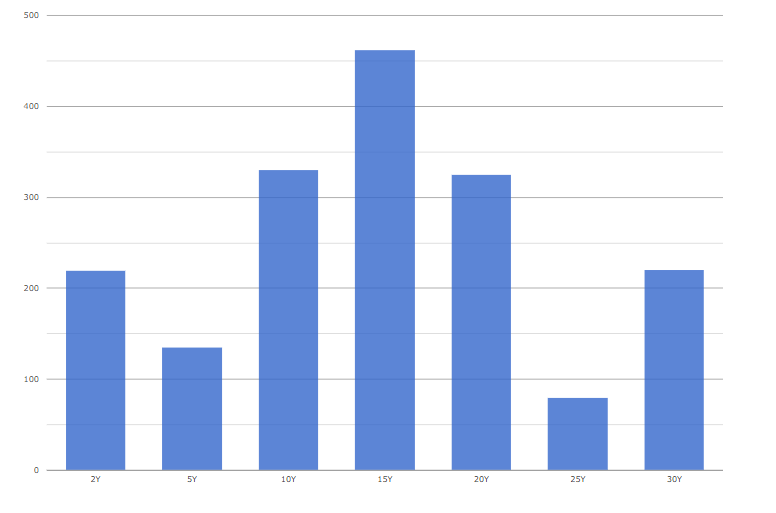

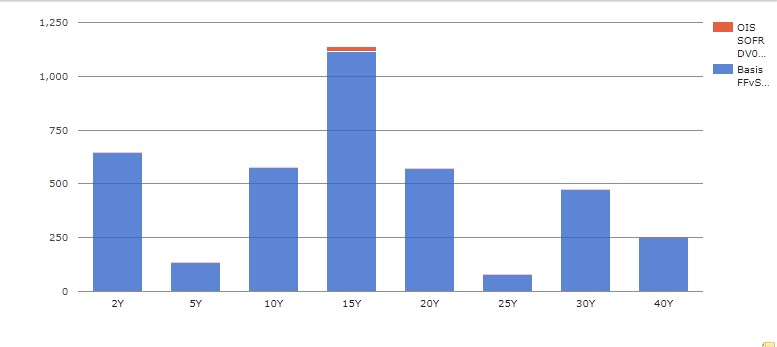

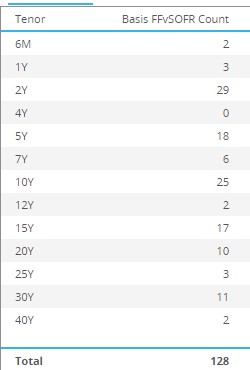

The maturity split is below. Why is 15Y so active?

ALL in Fed Funds vs SOFR basis. Nothing outright has traded.

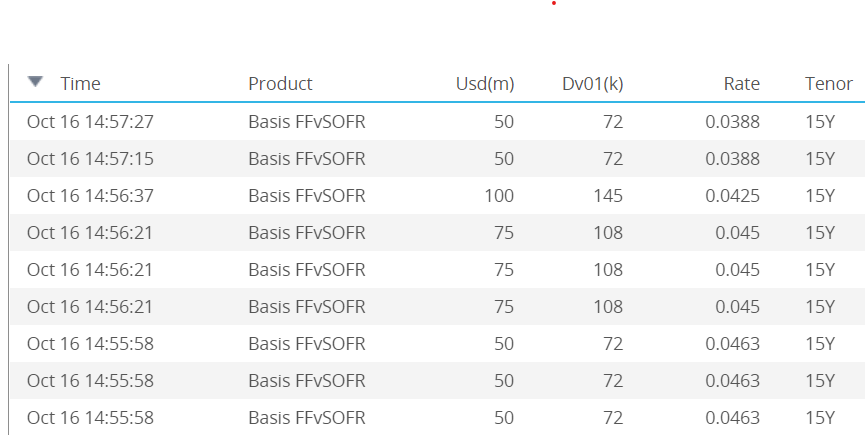

14:00 LDN Time 16th October 2020

Well, this is odd. 5 15Y trades all reported very close together, but in a range of 0.75 basis points. That is quite some spread for a basis trade in a short period of time. And why is 15Y the focus?!

14:35 LDN Time 16th October 2020

And the results are in! Bravo LCH for providing so much transparency over this process:

14:58 LDN Time 16th October 2020

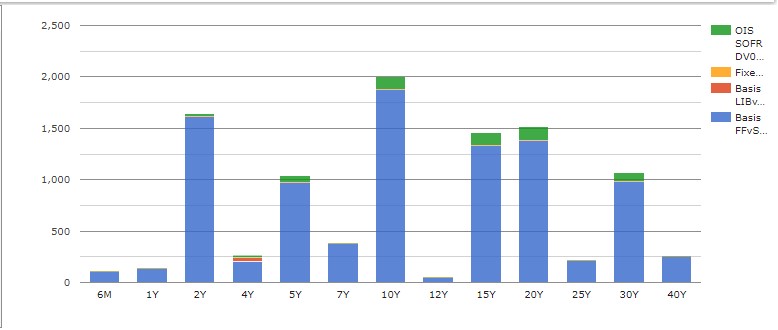

And SDRView now shows 64 Basis Swaps with $5.5 billion gross notional or $3.9 million DV01.

15Y is by far the largest tenor traded, while we also see two trades in 40Y.

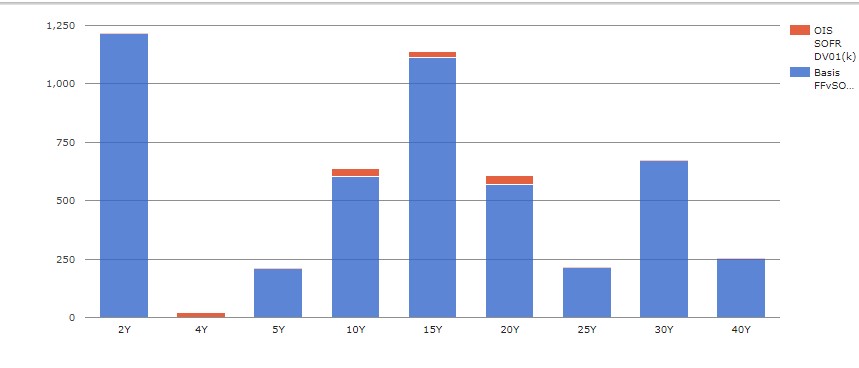

15:35 LDN Time 16th October 2020

Lots more 2Y trades now overtaking 15Y in DV01 traded.

Total gross notional now $8.6 billion and total DV01 $4.85 million.

16:24 LDN Time 16th October 2020

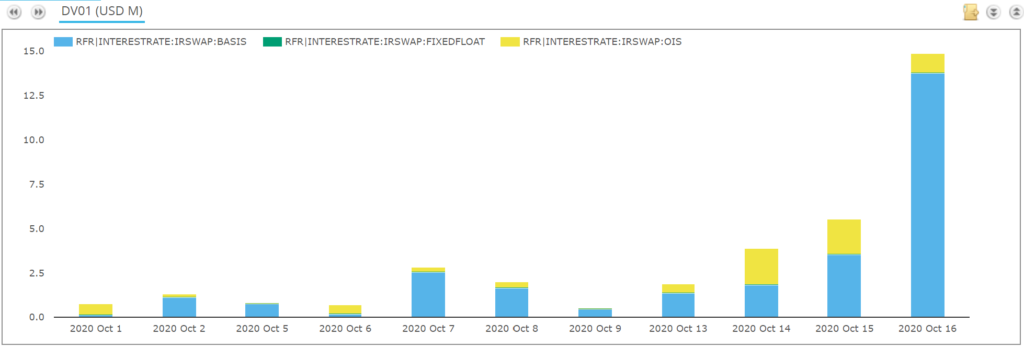

Going great guns now, 105 basis FF v SOFR trades, $12.6b notional, $6.2m DV01, definitely a record day.

17:15 LDN Time 16th October 2020

5Y and 10Y picking up.

128 Basis Swaps, $16.7b notional, $7.5m DV01.

Trade counts:

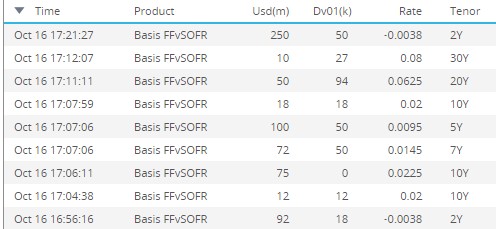

Pricing consistent with the earlier LCH Auction mid shown above.

A few recent trade shown below with prices in percent, so 30Y is 0.08% or 8bps, meaning FF v SOFR+8 bps is the par rate.

18:21 LDN Time 16th October 2020

160 Basis Swaps, $19b notional, $9.5m DV01.

10Y the largest with 36 trades and $1.9m DV01.

19:15 LDN Time 16th October 2020

177 FF v SOFR Basis Swaps, $20.8b notional, $10.7m DV01.

21:55 LDN Time 16th October 2020

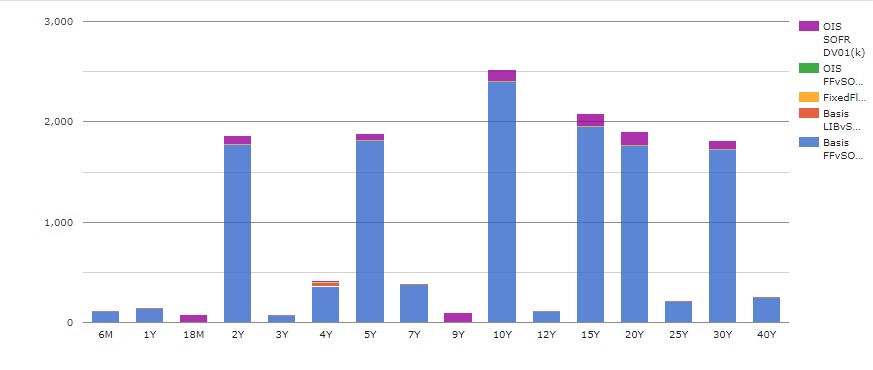

Last update for the day at 4:55pm NYC and what a day for SOFR.

We will do a proper summary on Monday.

For now, the key stats are:

- 216 basis FF v SOFR Swaps traded

- $24 billion gross notional, $13 million gross DV01

- Each of the LCH Auction tenors (2,5,10,15,20,30) with > $1.7m DV01

- 10Y with 44 trades, 2Y with 38, 5Y with 35 trades

- 10Y with $2.4m DV01, 15Y with $1.95m, 5Y with $1.8m DV01

Monday October 19th 09:15am LDN

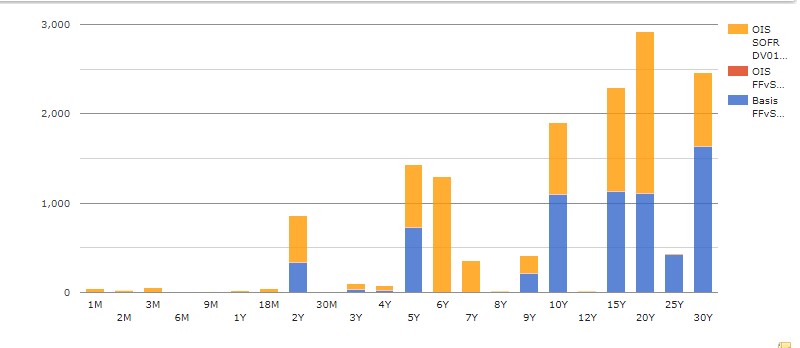

What a day Friday turned out to be in the SOFR market. For some context, we know that the days running up to the SOFR big-bang at LCH were record days. And yet 3-4x more SOFR risk traded on Friday than ever before:

Showing;

- $14.88m DV01 traded on Friday. The previous record was $5.57m on Thursday.

- This is the gross DV01 reported to US SDRs, so underestimates the total due to block trades reported at their capped thresholds.

- Friday saw 22 blocks trades amongst 255 total trades.

- And for those who care about such things, the total notional was $26.74bn, $9bn of which was related to block activity.

When you recall that the final size of the LCH auction was $9.1m DV01/$23.4bn in notional, it is truly impressive that the full size of the auction transacted in a single day.

In terms of block activity, I cannot see a single 30Y block trade reported. That means, as we expected, that the LCH auction swaps themselves have not been reported yet.

The total gross amount of SOFR risk traded on Friday was therefore about double what was reported to the SDRs. Impressive stuff. I also find it impressive that so many block trades transacted, showing that there was real liquidity to move size.

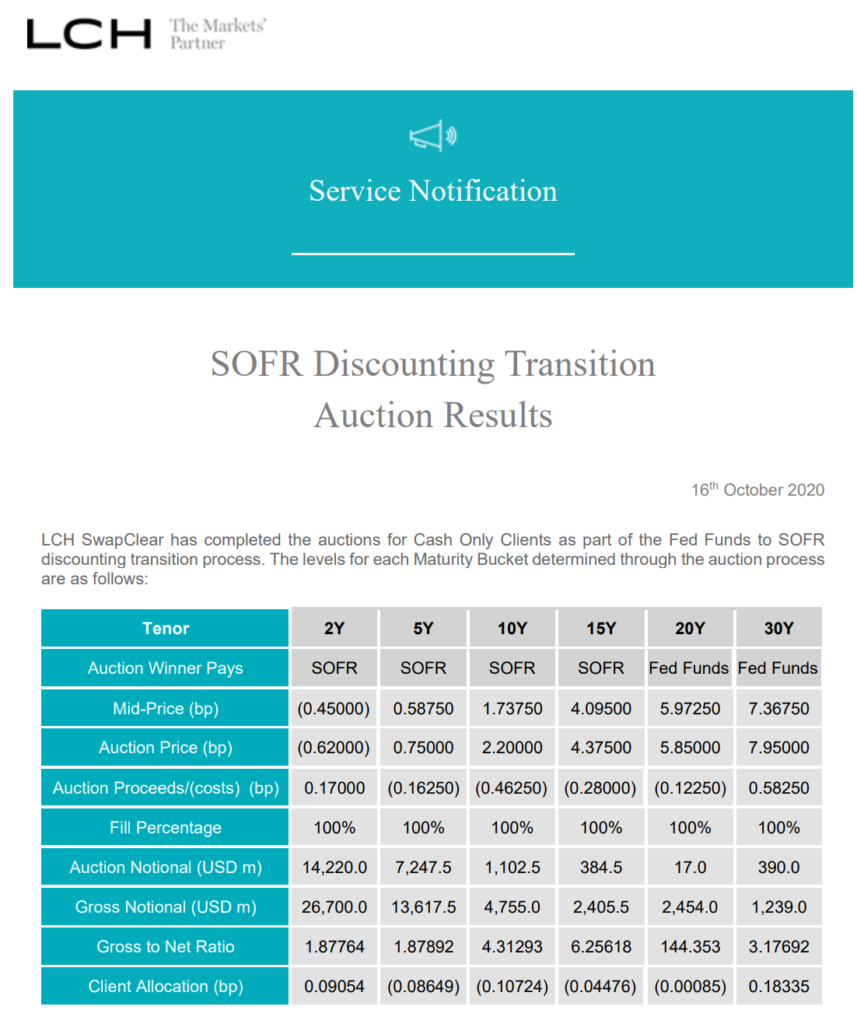

Finally, LCH have provided full details of the auction results here. The overall transacted prices are revealed:

Such transparency is highly commendable. Well done LCH.

Today will see the CME SOFR auction. As far as I am aware, we do not know the size or direction of this auction. We do know from the auction protocol document that the process will kick-off at 9am New York time. So all eyes on screens to see what kind of activity we have today!

And if you want to follow all of the action today, subscribers can see all SOFR swaps via SDRView Professional in real-time. Everyone else will have to wait for us to periodically update this blog!

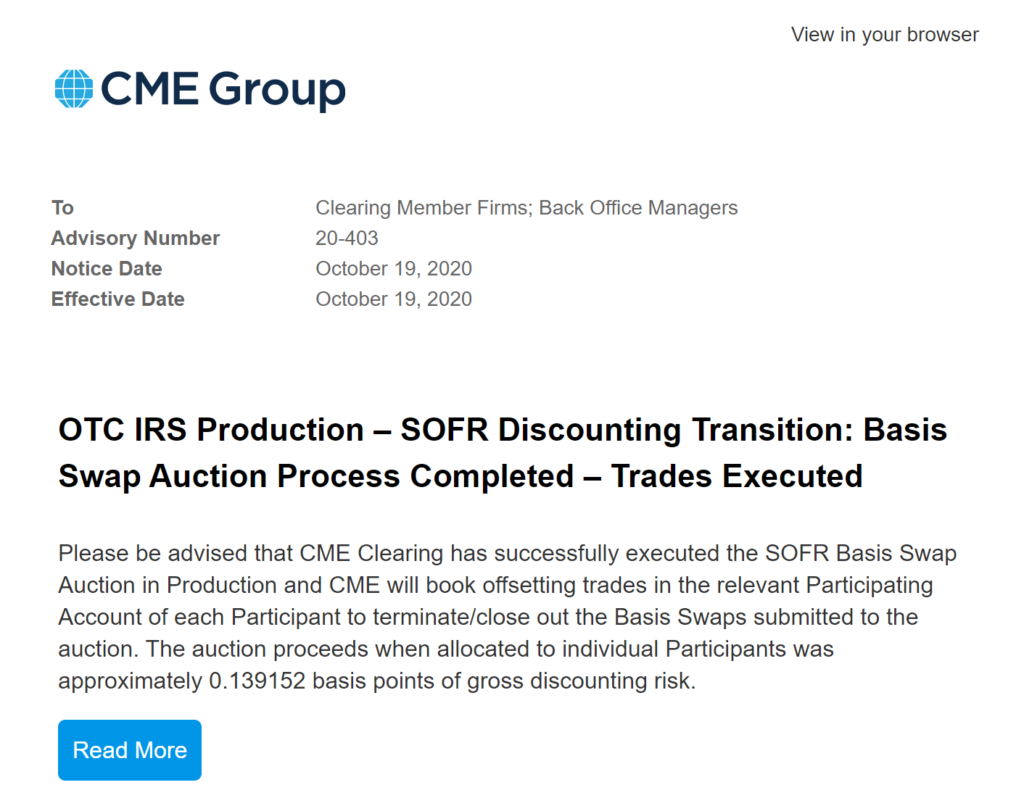

16:15 LDN Time Monday October 19th

About ten minutes ago we received confirmation that the CME auction has now completed:

We still have little idea as to how large the auction was, so we will have to wait for those rumours to surface. However, the state of the SDR so far today probably gives us a pretty good idea.

- 180 swaps (!)

- $6.6m DV01

- $17.9bn notional

It is noticeable how many outright OIS SOFR trades have been reported. From my understanding, these may be a direct pass through of how the CME swaps were booked because clients were given the option to receive the basis swaps as either a single Fed Funds vs SOFR basis trade or as two outright OIS trades. Maybe the outright SOFR OIS trades are finding their way straight to the SDR as clients actively trade out of them? Still, it is a noticeable difference to Friday when most of the trades were in basis.

The most noticeable aspect of trading today has been the collapse in the basis in 30Y. The LCH auction cleared at 7.95 basis points versus a market mid of 7.4 basis points. And yet the 30Y trades today have headed only one way – lower. We started the day at 7.75 basis points, and yet last traded at 5 basis points! That is quite remarkable.

It would suggest that the CME auction was not as large as the market anticipated, therefore the expected amount of paying interest in the long-end hasn’t transpired today.

Of course, we still have another half a day of trading activity to come today. For reference, the shorter points of the curve have not moved as much, with 10Y only 0.75 basis point lower.

17:05 LDN Time Monday October 19th

The SOFR trades continue to hit the SDR at quite a pace. Packages of small trades, with identical tenors and timestamps, are hitting the SDR fairly regularly. I guess these are account-level trades allocated to clients and traded en-masse after the allocation.

There are certainly a high number of trades today, running at 242 now, versus 255 on Friday. However, the amount of risk is lower, hitting $8.8m DV01 just now.

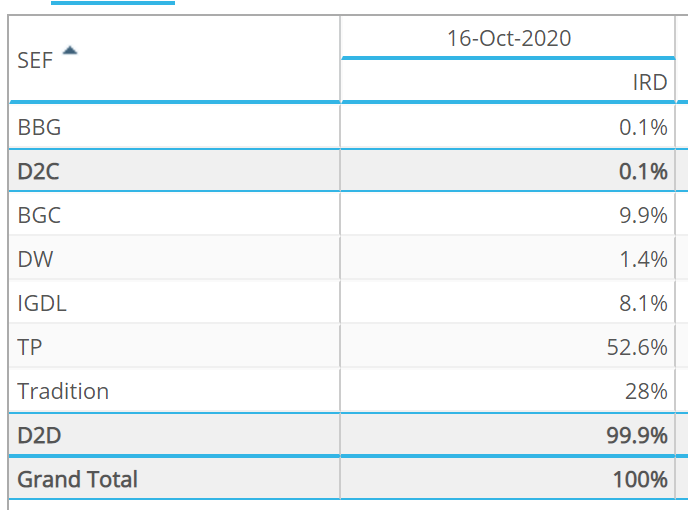

For interest, SEFView has now published Friday’s figures. Looking at USD Basis products, we can see the approximate market share of the IDBs on Friday for the SOFR transition products. Well done Tulletts and Trads!

20:35 LDN Time Monday October 19th

An update from SDRView as we near NY close:

- 250 Outright OIS SOFR Swap, $19.8b notional, $8m DV01

- 146 Basis FF v SOFR Swaps, $6.8b notional, $6.7m DV01

- 20Y the largest tenor, followed by 30Y, 15Y, 10Y

- (3 trades reported incorrectly as OIS FF v SOFR instead of Basis)

Great to see some activity in the long end of the curve.. Would be exciting to see what liquidity it ends up creating

Any idea on net FEDFUNDS v SOFR. I would have expected there would have been a preference for the interbank to keep their risk in FEDFUNDS and clients risk in SOFR.

Keep up the blogs Chris. How much SOFR trading post this migration would be interesting to see.

Hi Ben, thanks for the comment, apologies for slow response. I agree that a sizeable portion of the market may stay on Fed Funds due to the complications in switching bilateral CSAs from Fed Funds to SOFR and agreeing the pricing differential without a trusted third-party to value the portfolio. However, if big dealers start negotiations with their bilateral customers and start to charge the discounting differential between SOFR-based hedges and Fed Fund CSAs, the correct motivations will be there for clients to properly engage and start moving bilateral CSAs to SOFR. This is very much a second (or even third-) order effect of the transition. I expect most to want to wait until we see liquidity definitively shift out of LIBOR-based products first. The ISDA-Clarus RFR Adoption Indicator for the November 2020-March 2021 period I think will be interesting to watch in the coming months.