Last month, news broke that Shanghai Clearing House was to launch FX Options clearing on August 1. The news inspired me to check for any data that might be out there. Sadly, as of today, there doesn’t seem to be any hard data to back this up. However I remained inspired enough to take a general perspective on the status of clearing in Asia.

Who Are the Asian Clearing Houses

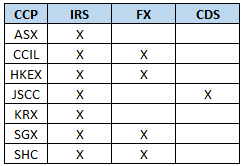

First we need to recap the 7 Asian OTC Clearing Houses, and what general OTC asset classes (within Rates, FX and Credit) that they are clearing:

More specifically, here is a list of what each CCP is clearing within these asset classes:

ASX (Australia):

CCIL (India):

- Single Ccy IRS (INR)

- FRA (INR)

- FX Forwards (USD/INR)

HKEX (Hong Kong):

- Single Ccy IRS (CNH, USD, EUR, HKD)

- Single Ccy Basis (EUR, USD)

- Non-deliverable IRS (CNY 7-day repo)

- NDF (USD vs CNY, INR, KRW, TWD)

JSCC (Japan):

- Single Ccy IRS (JPY, USD, EUR, AUD)

- Single Ccy Basis (JPY, USD, EUR, AUD)

- CDS Index (iTraxx Japan)

- CDS Single Name (12 large Japanese corporates)

KRX (Korea):

- Single Ccy IRS (KRW)

SGX (Singapore):

- NDF (USD vs CNY, IDR, INR, KRW, MYR, PHP, TWD)

- Single Ccy IRS (USD & SGD)

- Non-Deliverable IRS (MYR, THB)

SCH (China):

- Single Ccy IRS (RMB)

- FX Spot, Forwards, Swaps

- FX Options ?

Mandates

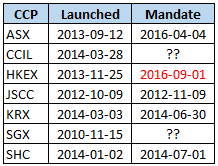

Before looking at the data we can get our hands on, we aught to remind ourselves how long each CCP has been offering OTC clearing services, as well as when their country introduced the clearing mandate. Here is what I could find:

Interesting to note:

- I couldn’t find evidence that India has mandatory IRS clearing yet (though FX settlement seems to be mandated)

- HKEX was pushed out earlier in the year, and is due to start in a months time

- Japan was first to mandate it, and took the approach of “we’ll mandate clearing a month after the JSCC offers it”

- Will Singapore ever mandate it, or is that considered not bank-friendly?

Data

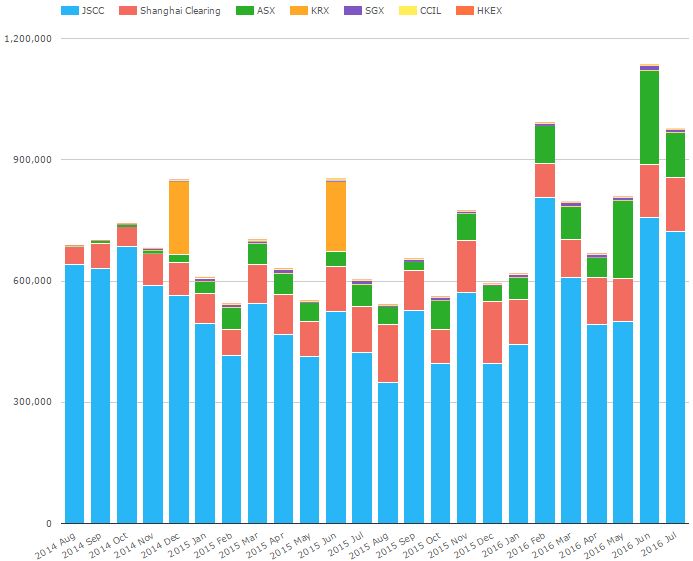

Onto the data. Let’s first look at monthly Trade volume per CCP:

Few things to note when looking at this:

- JSCC has by far the largest chunk of activity. I suspect this is due to local regulations that require banks to clear at a local (Japanese registered) CCP. Though I recall LCH recently has been given such credentials as well.

- Shanghai is significant, though I cant speak to their local mandates. However if you assume everything is RMB, then banks have nowhere else to go besides SHC.

- ASX probably now larger than SHC (in recent months)

- KRX is tough to figure out, as they are not transparent with their daily or monthly trade volumes, so a bit of a mystery.

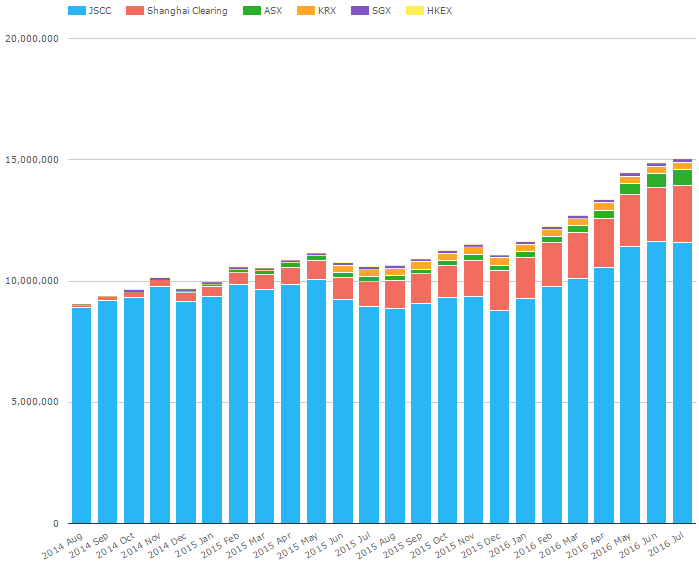

Then at Open Interest:

Just over 15 trillion USD worth of open interest.

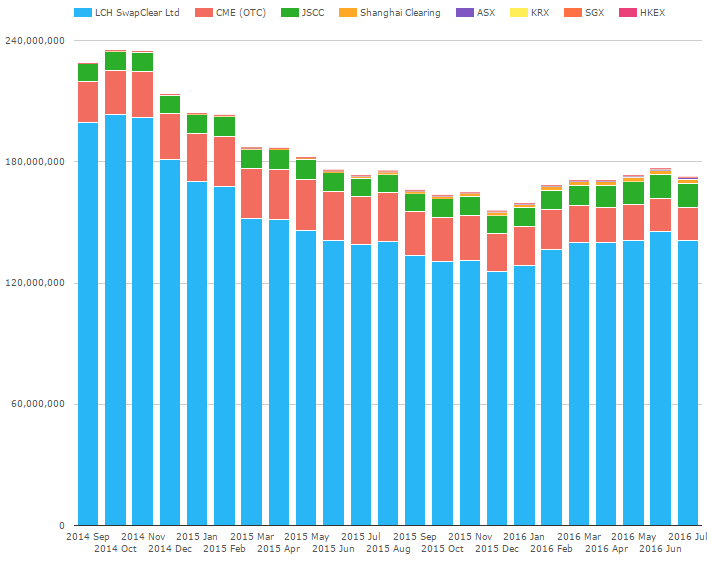

To get a sense for the scale of this open interest, lets introduce LCH Swapclear and CME clearing into the mix:

This shows that the 15 trillion of open interest in Asian CCP’s is a still just a fraction of the roughly 172 trillion now cleared globally.

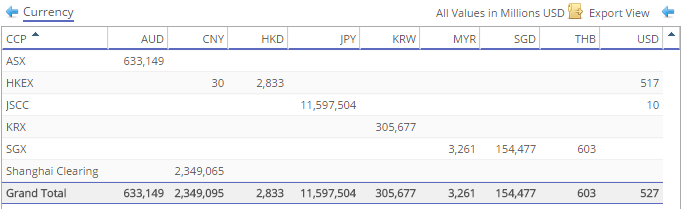

Lastly, lets look at the open interest per currency.

This shows what I expected: that outside of some tiny rounding errors, each CCP is clearing almost entirely their local currency.

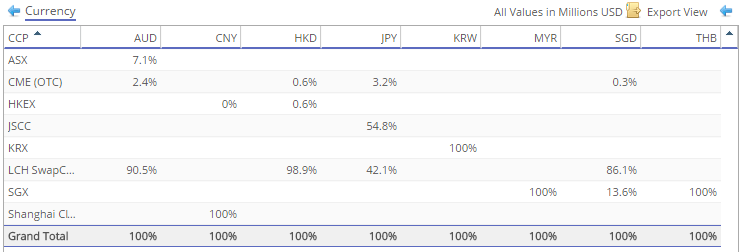

Which begs for one final table of data. If we now look at each CCP’s percentage of cleared Asian currencies:

We can glean:

- LCH has a strong showing in the national currencies that they clear (AUD, HKD, SGD)

- In currencies that are not clearable at LCH (CNY, KRW, MYR, THB), the local CCP has the grand sum

- Exception being JPY, which is majority cleared at JSCC

Summary

I had hoped to grab some FX Option clearing data from Shanghai and reminisce of the troubles the industry has had in offering options clearing. Sadly, either there is no activity or the clearing house is not telling the world about it (at least in English). As a precedent, SHC launched IRS clearing in January of 2014 but did not report statistics until August of that year, so perhaps we just have to wait for the hard data.

On the way, we learned a few things:

- 4 of the 7 jurisdictions have mandatory IRS clearing of some nature already. HKEX will be the 5th soon. India and Singapore remain question marks.

- Japan, China, and Australia see the most daily swap activity in the region

- Predominantly all of the swap activity in Asian CCP’s are in their local currency

As for FX and Credit, or Europe and Latam, that will have to be another blog for another day.