- Spreadovers account for roughly 35% of all USD risk traded on-SEF.

- In D2D USD swap markets, Spreadovers account for about 70% of volumes.

- This makes them by far the most important packages traded in USD.

- Almost all Spreadovers are transacted on a SEF.

- We look at D2D SEF market share in USD swaps.

History

We last looked at Asset Swaps back in May 2017 and looked in detail at USD Spreadovers in January 2017. That means we’ve got 18 months of history to catch up on in this blog, so read on to find out what’s been happening.

What is a Spreadover?

First off, we define a Spreadover:

- A spot starting USD swap.

- Standard semi-bond conventions (3m Libor vs fixed leg of 30/360 semi-annual payments).

- Has a benchmark maturity date (exactly 5y, 10y, 30y etc from spot).

- The swap leg is cleared.

Spreadovers are a highly standardised product that almost exclusively trades in the interbank market.

How Important are Spreadovers?

The answer to this question, broadly speaking, depends on which area of the market you are talking about.

Off-SEF Trading

All Spreadovers are traded on-SEF. We identify the odd trade done off-SEF, but these account for less than 1%.

SEF Trading

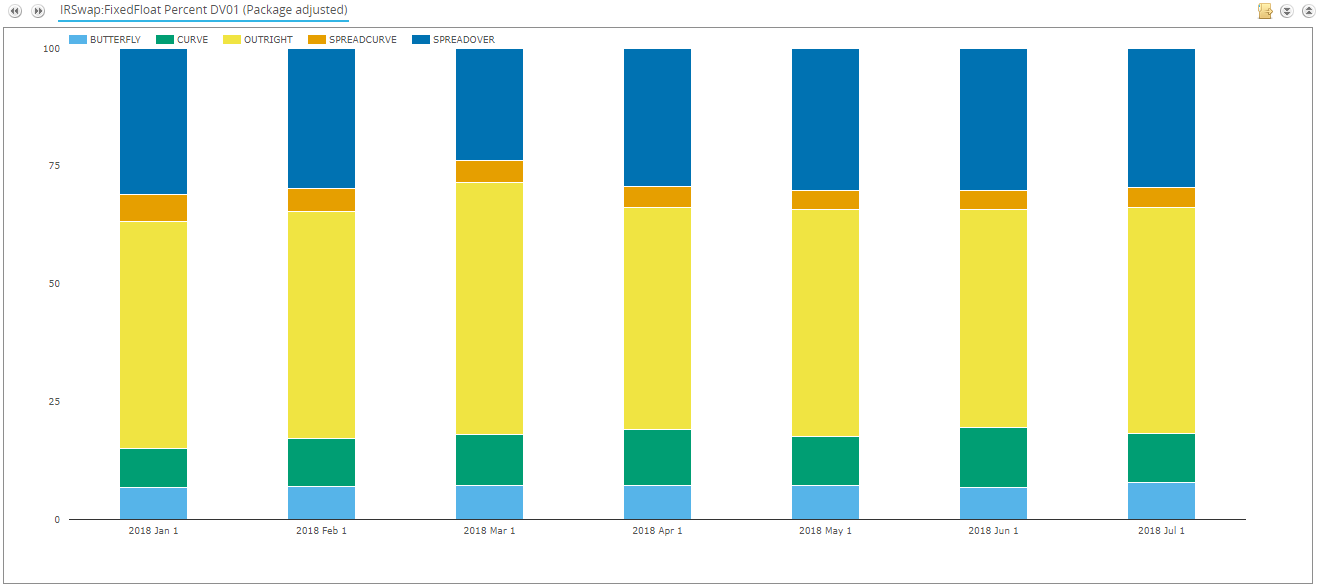

If we look at SEF trading across both D2C and D2D venues, we see the following split for spot-starting USD swaps:

Showing;

Showing;

- The percentage of risk (as measured by DV01) traded each month per package.

- We split spot starting swaps into either Outrights (i.e. a single leg), curve trades (aka a maturity spread), a butterfly or some kind of Spreadover (either a single Spreadover or a Spreadcurve trade which involves more than one Spreadover transacted concurrently).

- Spreadovers (including Spreadcurves) make up 34% of total risk traded. They are by FAR the most important type of package traded when we look on a DV01-adjusted basis.

- In comparison, curve and butterfly trades make up 10% and 7% of risk respectively. They are much less active than Spreadovers.

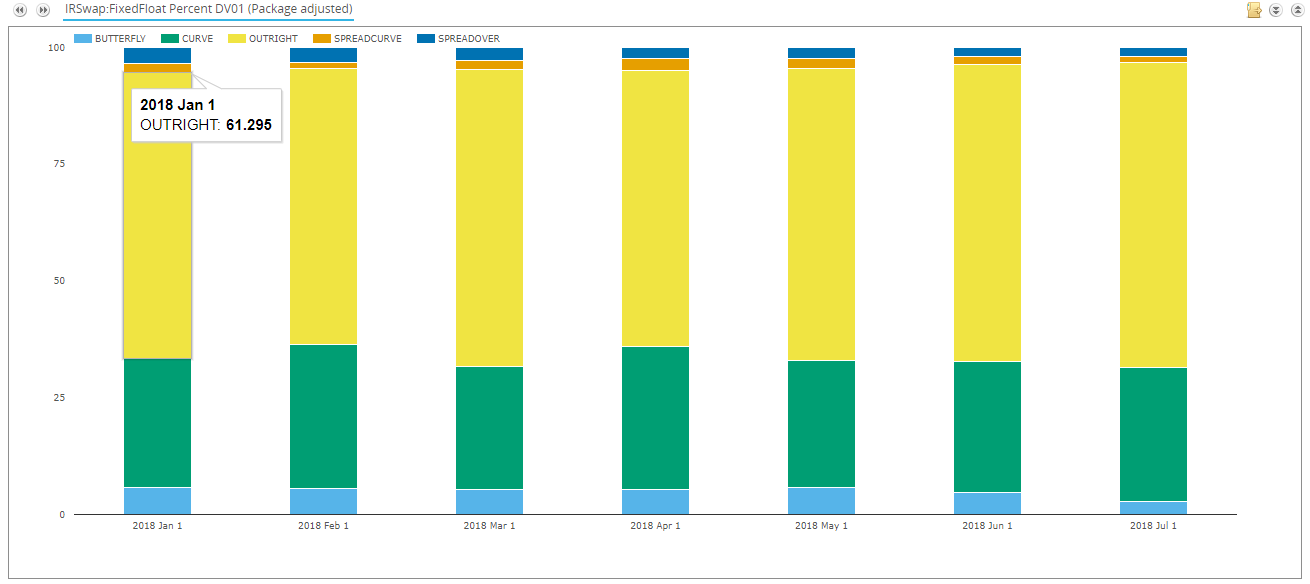

Dealer to Customer Trading

In the D2C space, Spreadovers are not very active. For all Spreadovers identified in the SDR, we see less than 7% (and normally more like 2%) traded across the Bloomberg SEF.

The exact split of packages across the Bloomberg SEF is shown below. It is markedly different to the D2D market (see next section):

Showing;

- On Bloomberg (which we consider typical of all D2C SEFs) most trades are outrights – nearly 65%.

- Almost no Spreadovers trade (less than 2%).

- However, Curve and Butterflies are frequently traded – accounting for over 30% of Bloomberg volumes.

Dealer to Dealer Trading

This is really the natural home for Spreadovers, and therefore is a huge component of the multilateral, Dealer-to-Dealer SEF World. We use our SDR data to approximate how much.

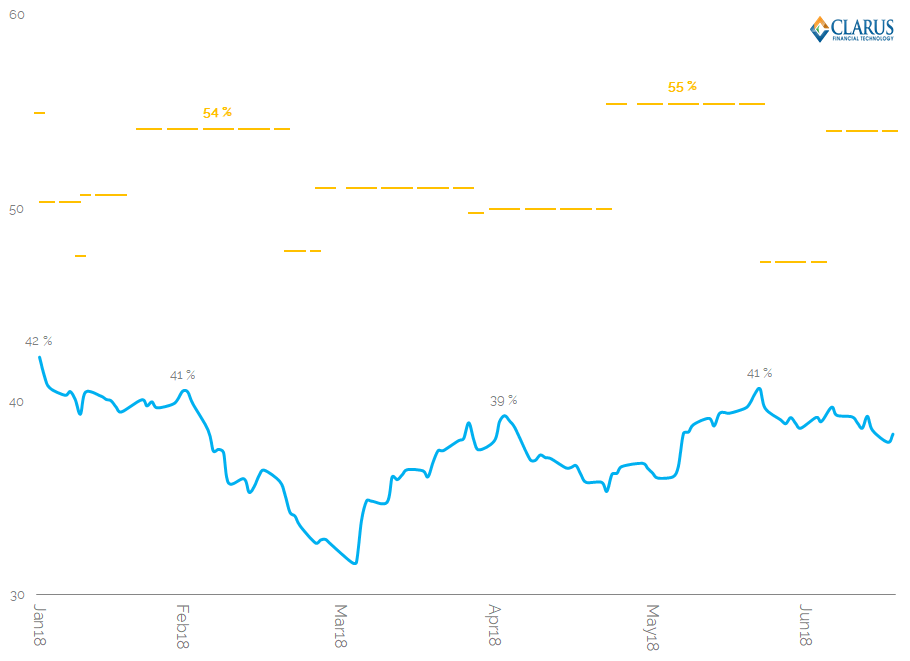

Using a distilled view of the D2D SEF trading activity (spot starting, ex BBG, ex block trades), we can see how important Spreadover trading has been during 2018. On a daily basis, here is the percentage of risk that has traded as a Spreadover each day:

Showing;

Showing;

- Daily percentage of SDR activity that is a Spreadover.

- The chart shows a rolling 20 day average, plus the maximum daily percentage during the past 20 days.

- Around 40% of risk is regularly traded as a Spreadover.

- There is a clear seasonality to this chart. The peaks above 40% all coincide with typical issuance season of new bonds – January and February, then around Easter and finally in June before the Summer lull.

- There are days that Spreadovers can account for as much as 55% of risk traded – the orange bands show the 20 day peaks.

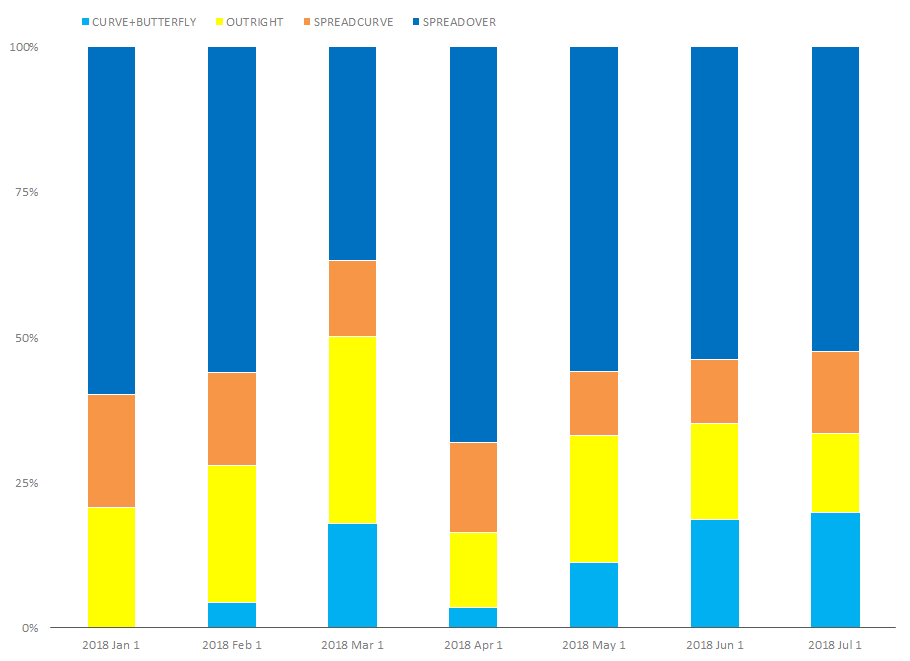

The above is only an approximation of the D2D SEF space, because we still have small trades (below D2D minimums) and a lot of Tradeweb trades included – most of which would be outrights as per Bloomberg SEF.

I therefore went one step further, and actively tried to remove all Tradeweb activity – using a combination of SEFView and SDRView data. When I do this, I get the below split by package for D2D trading of USD swaps:

Showing;

Showing;

- In 2018, 69% of all D2D SEF volume has been a Spreadover!

- Spreadovers have even accounted for 84% of risk during some months.

- This data really highlights a significant difference to the D2C markets, where we see 65% of risk traded as an outright and none as Spreadovers. That is almost completely reversed in D2D SEF markets.

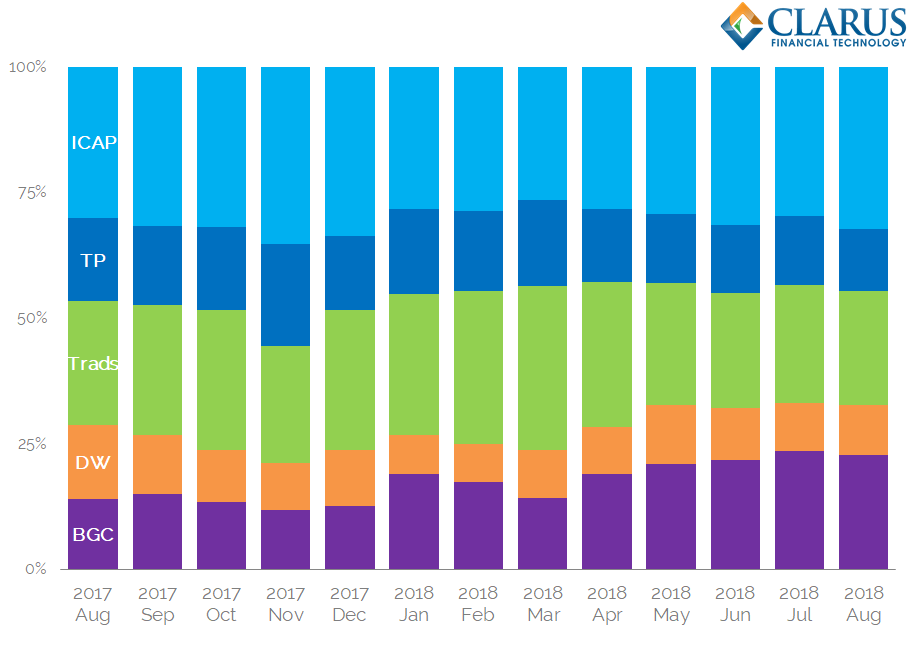

SEF Market Share (All Strategies in Major Tenors)

We do not directly identify Spreadovers in our SEFView data, but we can look at market share across the D2D SEFs in the major tenors:

Showing;

- Market Share per D2D SEF for vanilla USD IRS across the following tenors: 5y, 10y and 30y.

- Market Share is shown as a percentage of USD DV01 traded.

In Summary

- Spreadovers are the most important packages traded in USD.

- They enable efficient risk transfer between cash bonds and derivatives and are almost exclusively executed on D2D SEFs.

- SEF data shows that ICAP have the leading market share in USD swaps.