- Counterparty Credit Risk should be closely monitored by all market participants.

- SACCR is a great tool to use, even if you are not required to do so by regulators.

- The SACCR model benefits from simplicity and credibility whilst still being a risk-sensitive model that is light-years ahead of gross notional measures.

- End-users of bilateral derivatives are potential users of SACCR.

- ISDA have also highlighted how data analysis tools, such as a SACCR model, could be implemented by regulators to monitor bilateral exposures using existing regulatory reporting data.

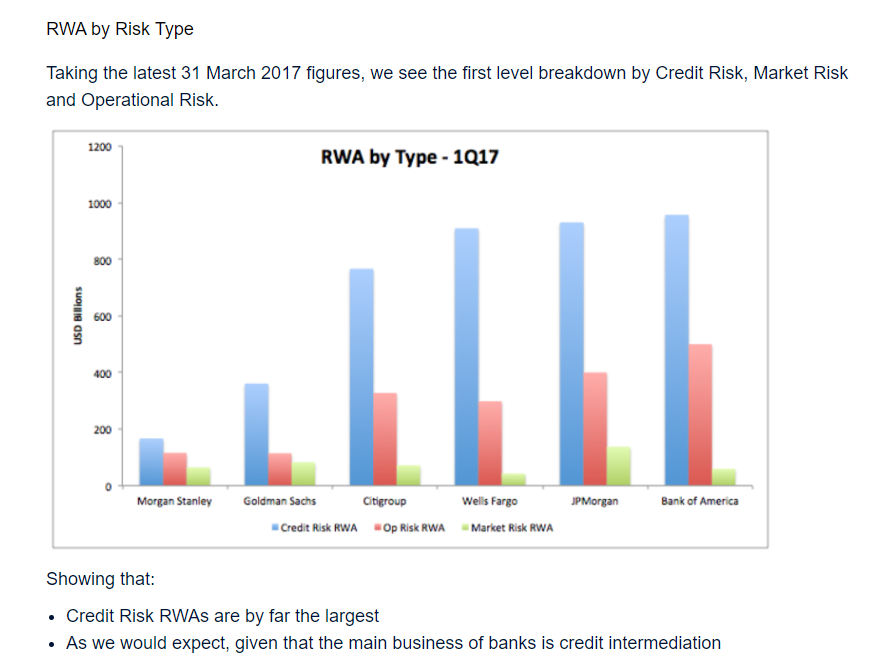

Risk Weighted Assets

Counterparty Credit Risk is typically the largest contributor to Risk Weighted Assets (RWAs) for banks. This Clarus blog covered RWAs way back in 2017 when looking at Basel III disclosures. It is highly unlikely to have changed in the intervening six years:

In today’s blog, we don’t want to necessarily talk about banks – although they are still welcome to read on (and use our software 😛 )! This blog focuses on end-users, and thanks to new paper from ISDA, on regulators.

End-users are expressly NOT in the business of credit intermediation, and hence do not typically have an explicit regulatory requirement to monitor Credit Risk Weighted Assets. However, most do monitor their counterparty exposures because it is prudent to do so! Why would anyone choose to run a risk-neutral package of 10Y10Y swaptions (for example) against two dealers when you are just creating credit exposures on both trades? It makes far more sense to remove those credit exposures when the market risk is neutral.

Whilst a lot of activity is now cleared, please remember that pretty much all FX and Equity derivatives are still bilateral, as well as swaptions and cross currency swaps in Rates. See “What is left Uncleared” for some data on just how large bilateral exposures still are.

SACCR to the Rescue

Before the introduction of SACCR (and in particular before I started writing blogs on it!), I always thought that the standard regulatory models used to monitor counterparty credit risk were too basic to be of any use in monitoring real exposures (see Current Exposure Methodology here). The old models looked at gross notional (no netting), current mark to market (minus any collateral held), and gave a static risk weight based on the maturity of the underlying trade.

Simple, yes. Sophisticated – certainly not.

It therefore made very little sense for a client to monitor their exposure to a bank using the old Current Exposure Methodology. Whilst this methodology was employed for banks for regulatory purposes (i.e. a necessary evil), it had very little business applicability.

Fast forward to a SACCR world. We now have a risk-sensitive measure of exposures which recognises netting. SACCR is also highly dependent upon how a trade is collateralised. This is good! It is therefore a standardised model that can be used to monitor general credit risk in a portfolio.

Why Do We Care?

Using SACCR, even when you don’t have to, is a sensible step because:

- It is a standardised model – meaning that it is transparent, well understood and easy to implement.

- It is credible – developed and calibrated by the BCBS (Basel Committee).

- It is symmetrical – end-users can understand dealer exposures, meaning that both sides of a trade understand the motivations for novations, portfolio maintenance and optimisation.

Implementing SACCR

SACCR is so simple that we typically start our clients with a Proof of Concept that is conducted in Excel. That allows business users to explore the outputs and understand the sensitivity of the outputs to things like ISDA master agreements, margin arrangements and posting thresholds. This provides a great platform to allow users to understand what SACCR is all about.

This prototyping also inadvertently points out that there is no need to have a whole quant team running proprietary credit exposure models. SACCR tends to motivate “good behaviour” – as outlined above, portfolio maintenance and optimisation all reduce SACCR exposures.

The key aspect here is that SACCR is risk sensitive. Yes, it can be hard to calibrate risk appetite – just how much EAD should you have at risk versus a dealer? – but that is a problem with any model implementation. SACCR is certainly much simpler than running any hist-VaR type of model.

We simply take the primary economic terms at a trade level:

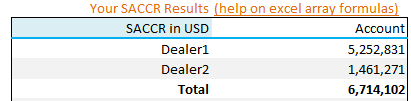

Combine this with input for the margin agreements (static data that covers frequency, minimum transfer amount and independent amount/Initial Margin posted) and SACCR already calculates the Exposure at Default across each “hedging set” for each netting agreement included:

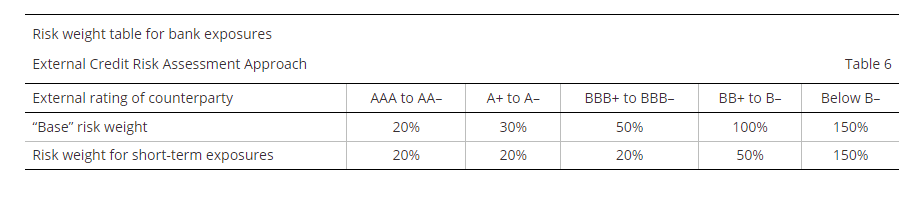

Depending on your calibration preferences, these EADs can then be directly converted into “Credit Risk Weighted Assets” using standard Basel III risk weights:

Or any risk weights that you choose to incorporate. Again – we are great advocates for simplicity at this step!

Scalability

One particular use case is pretty neat here. Regulators, armed with counterparty information, can monitor not only market risk but also counterparty credit exposures using reg reporting data (because they have counterparty information that is not present in the public data). Whilst unlikely to be a complete representation of a counterparty relationship, it is a great way to monitor changes in exposures over time.

As ISDA have just put it, these exposures are “Hidden in Plain Sight“. It is surely a step most regulators would take given sufficient budget and resources to do so:

All Asset Classes and No Greeks

Much of the beauty of SACCR lies in its simplicity. There are no “greeks” to calculate, even for non-linear products. Regulators (Basel) have calibrated the risk weights and they use a simple flat vol to calculate effective deltas for option portfolios.

SACCR also covers all asset classes. No worries over running one model for Rates/FX and others for different asset classes (looking at you Commodities)!

Using a trade-level input file is as simple as you can get. SACCR could be run on “deltas” as well (transposing into standardised instruments). And whilst it is tempting to think that ISDA SIMM does something similar with Greeks, you have to remember that ISDA SIMM is not calibrated in terms of risk weights to deal with counterparty credit risk per se. It is focused on market risk.

Beyond Prototyping

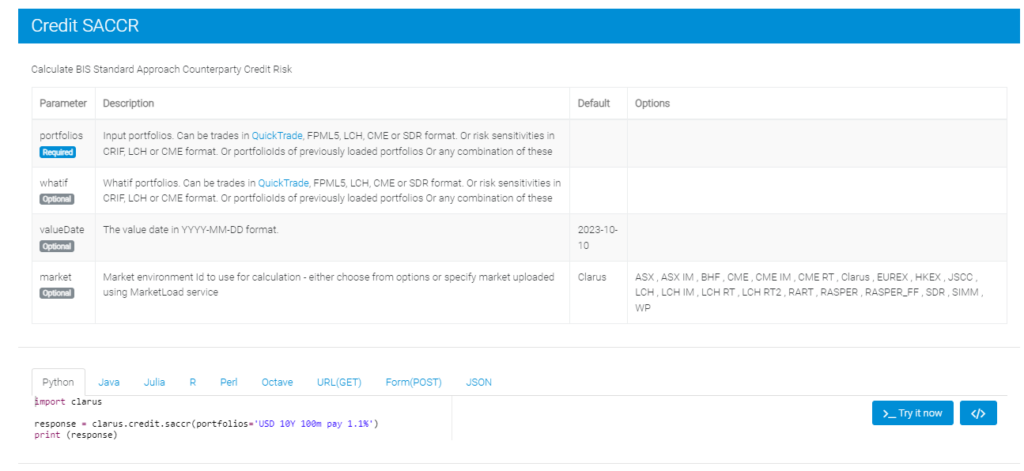

It is important to get a good feel of how SACCR behaves for a couple of well-understood portfolios before unleashing it across a whole business. For portfolios running to more than a few thousand trades, moving away from Excel, even for a prototype, makes sense. Our microservices allow our clients to do exactly that. Employing the same process, it is simply a change of interface (to Python, R, Java, Perl etc) to run SACCR analytics on your trade-level portfolios:

This is then a highly scalable solution for large portfolios. Running on the same “supermodel” SACCR, it can be integrated in any number of ways – into existing systems, standalone reporting, dashboards etc. And it would fit perfectly into ISDAs proposed use-case for regulators to start monitoring derivatives exposures in a more standardised and holistic manner.

In Summary

- Counterparty Credit Risk continues to be the largest contributor to Risk Weighted Assets in bilateral markets and should be closely monitored by all market participants.

- Methods to calculate and monitor counterparty credit risk do not have to be limited to banks.

- End-users and regulatory supervisors can now benefit from a risk-sensitive model, SACCR, to monitor counterparty credit risk.

- SACCR benefits from simplicity, credibility and symmetry.