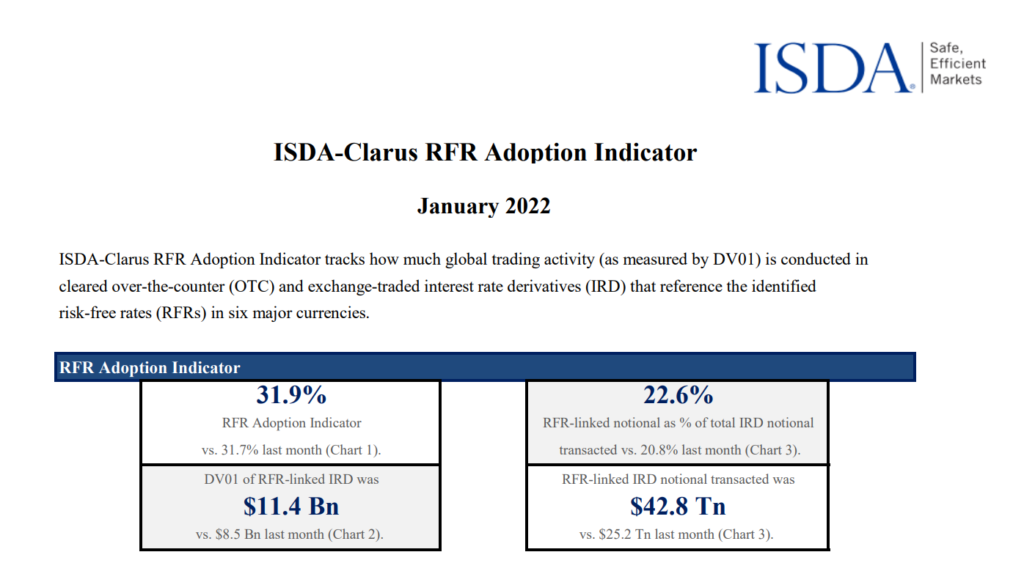

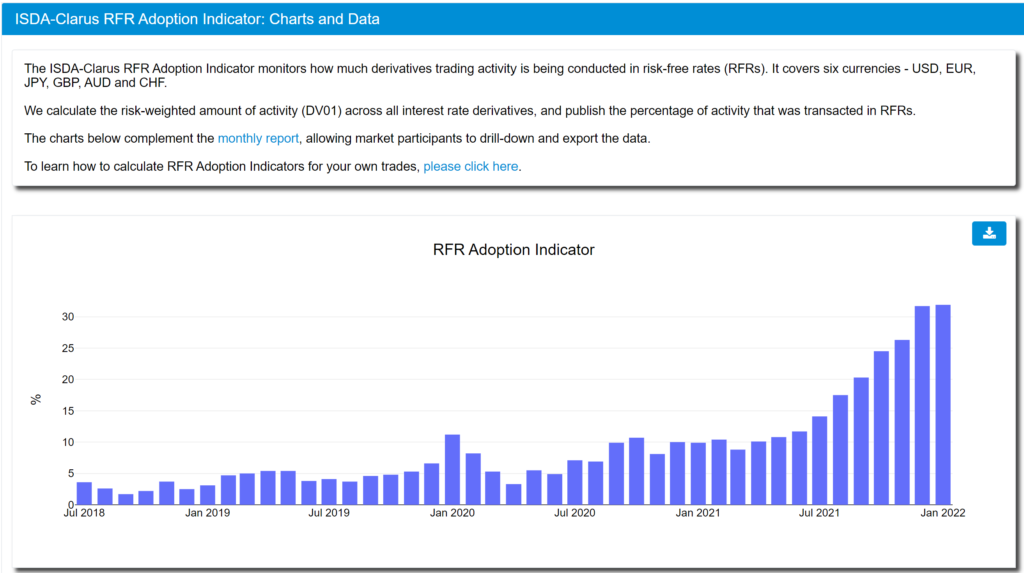

The January 2022 ISDA-Clarus RFR Adoption Indicator has now been published. It delivers a few really important lessons about the underlying markets (and data).

The headlines include:

- A virtually unchanged headline adoption rate of 31.9%, versus 31.7% for the previous month. The full time-series is available at rfr.clarusft.com:

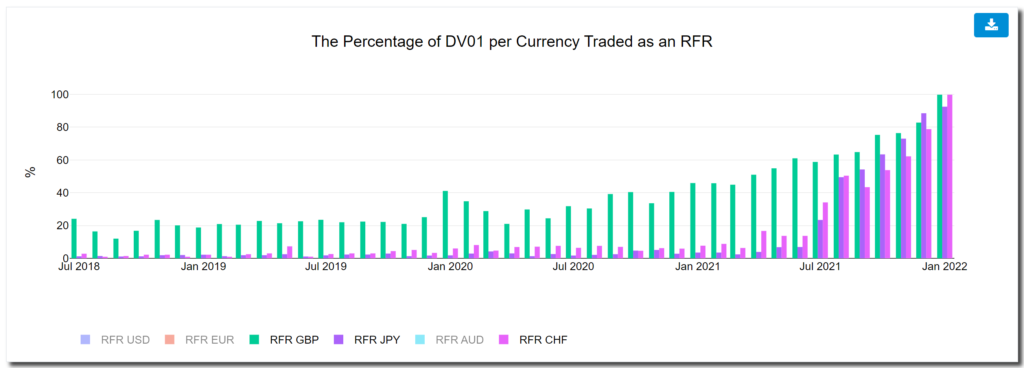

- 99.8% of all new GBP and CHF risk was traded versus the RFR. Mission accomplished in terms of transition in these markets.

- 92.5% of all new JPY risk was traded versus the RFR (TONA). It will be interesting to see where this equilibrium ends up. Will TIBOR (“onshore” LIBOR in JPY markets) end up a larger or smaller proportion than 10% of this market long-term?

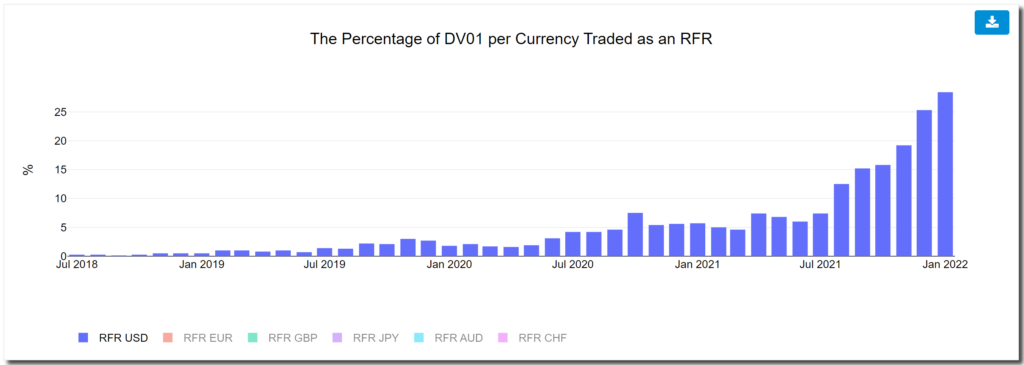

- SOFR adoption at 28.4% of all USD risk traded was a new high, adding 3 percentage-points to the last print in 2021.

- €STR adoption declined slightly to 14.5%, which is somewhat of a surprise given what has happened in Cross Currency Swap markets in particular.

If we have such good, compelling news in each underlying market (EUR aside), why did the overall Adoption Indicator not increase by more?

The USD Market Remains Key to Transition

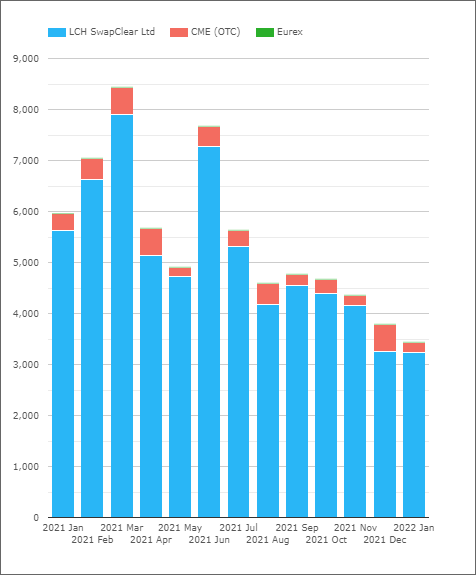

As ever, the devil is in the detail. Check out the amount of USD LIBOR risk cleared at LCH SwapClear:

Showing;

- The USD DV01 of vanilla fixed float swaps in USD cleared at LCH SwapClear each month.

- The gradual decrease is a really positive sign for transition.

- January 2022 was a really busy month for USD Rates, but the amount of USD LIBOR risk cleared did not increase this past month. That is a great sign!

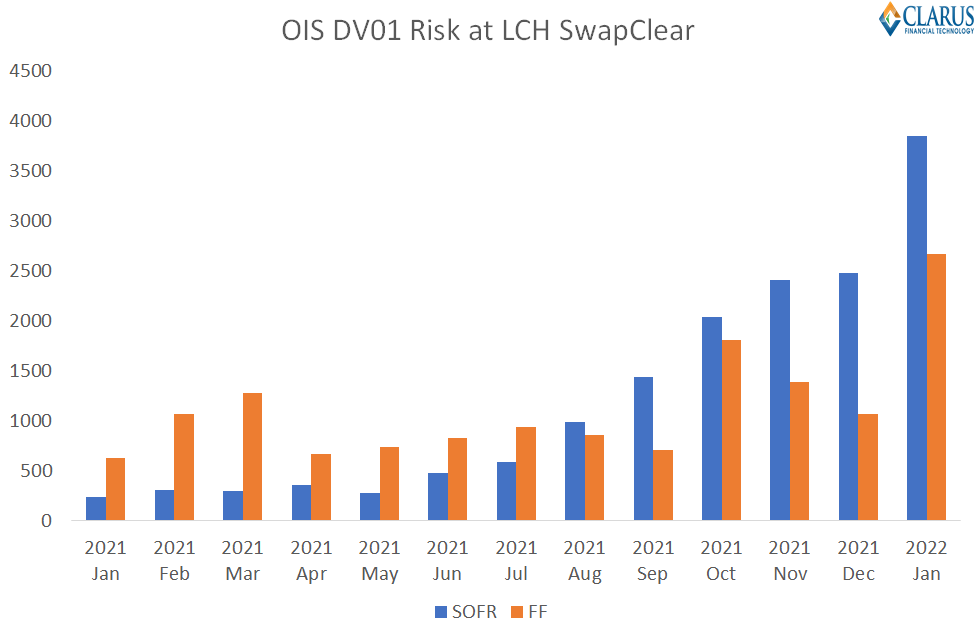

What we did see was a massive increase in the amount of OIS risk cleared at LCH. But this was not all in SOFR. Old habits tend to die hard, and Fed Funds (FF) had a huge month:

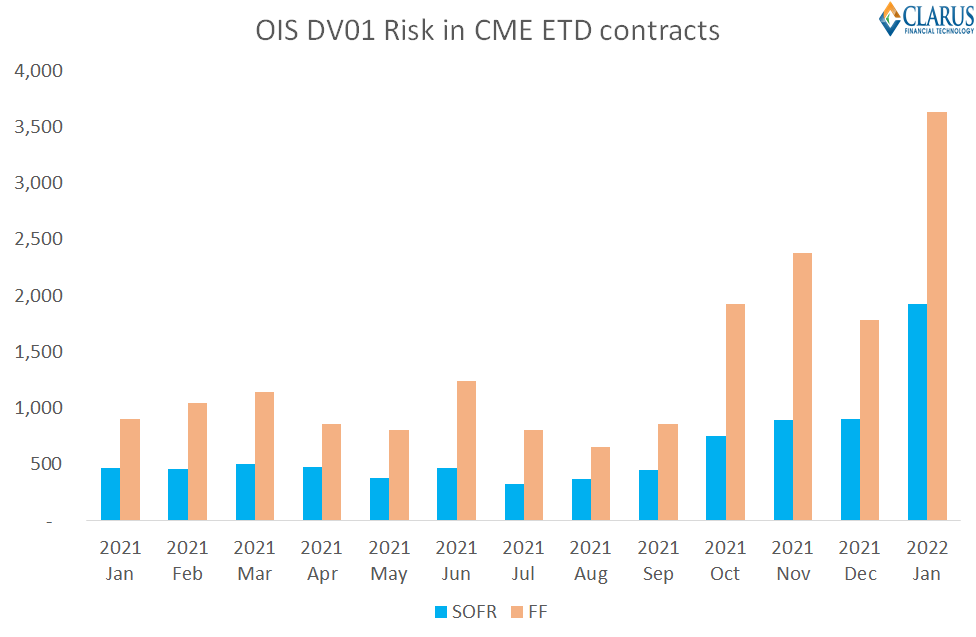

And of course, this wasn’t limited to just LCH. CME and the futures contracts traded there saw a very similar phenomenon:

What does this mean for the data?

- SOFR had a massive month. The total DV01 of SOFR linked contracts across OTC and ETD contracts increased to $6.1bn DV01, a record month and an increase of $2.2bn on the previous month.

- (That monthly increase is as much SOFR risk as traded in the entire month of September 2021 for context).

However, Fed Funds trading probably benefitted from being a more mature market. With the Fed “in play”, Fed Funds contracts saw a lot of trading:

- Fed Funds risk transacted more than doubled between December 2021 and January 2022.

- At least $6.3bn DV01 of Fed Funds risk transacted across OIS at LCH and Fed Funds futures at CME.

- The huge increase in Fed Funds activity (+$3.5bn DV01 month on month) was large enough to “counteract” the increase in activity we saw in SOFR.

- Interesting to note that SOFR is a much larger OTC OIS market than Fed Funds now.

- However, in ETD markets, Fed Funds remains a much larger market than SOFR.

All said, because the USD market is so large, and because a significant amount of Fed policy-related trading happened in Fed Funds, this served to severely limit the growth in the headline RFR Adoption Indicator.

All of this, despite GBP, CHF and JPY turning out virtual 100% numbers!

That’s a good lesson about just how large the USD market is.

In Summary

- Total DV01 executed versus an RFR was $11.4bn, higher by 34% versus last month and therefore an all-time high by over $2.3bn in DV01.

- January 2022 was an extremely busy month in Rates trading, particularly in USD markets.

- As a result, Fed Fund contracts saw a significant increase in activity.

- This means there was a marginal increase in the RFR Adoption Indicator to 31.9%.

- SOFR adoption hit a new high of 28.4%.

- Virtually all of GBP, CHF and JPY risk is now traded versus an RFR.

Chris, great update as always. Two points / questions I’d like to ask:

(i) When you say “old habits die hard” with regard to Fed-Funds volumes (i.e. derivatives including swaps, not the spot overnight market), you imply that you expect FF derivatives to be gradually replaced by SOFR derivatives: why do we have that expectation? As long as US banks fund themselves partially in the Fed-Funds market (which I assume they will always do), there will be need to hedge the funding risk via Swaps and other derivatives. There will always be appetite for unsecured overnight funding: why should it all dry u pin favor of secured SOFR? I don’t see how Fed-Fund will die out, especially as it’s still the rate that the FED targets…

(ii) Euro-Dollar futures (i.e. LIBOR futures) volumes still dominate SOFR futures by a factor of 3: worth mentioning in update, as THAT to a large extent still explains the relatively low adoption indicator for the USD markets…

Thanks for the questions Jan! On Fed Funds, I wrote a blog a while back showing that 90% of volumes come from the FHLBs (https://www.clarusft.com/usd-fed-funds-and-the-fhlbs/). That doesn’t seem healthy to me. Coupled with SOFR being chosen as the RFR, it seems likely that speculative and hedging activity tied to the outlook of monetary policy will sit in a market with a more diverse range of participants – such as SOFR. It will be interesting how the two continue to co-exist.

On the Eurodollar futures, that is certainly the biggest outstanding question. Let’s see where the February numbers come out later this week….