I’ve been wondering about the success of agency execution firms such as UBS Neo. The headline sales pitch for such a service seems to be:

- One technical integration/onboarding exercise to just one “SEF”, gaining a firm access to the liquidity of all 20+ SEF’s combined.

- A firm does not need to sign up and review/stay in tune with each ones legal documents.

- The SEF member (the agency, not the firm) handles compliance of CFTC record-keeping rule 1.35

- Prices are aggregated from all SEF order books into one master, best bid & offer.

Sounds good to me. Is it working?

BACKGROUND

My background in agency business is foreign exchange prime brokerage, whereby a firm uses a larger firms name and balance sheet to get preferential execution. In this world of FX prime brokerage, the client effectively borrows the balance sheet of a bank by transacting in their name, and subsequently gets the trade via a give-up transaction:

- Client communicates to Bank A (the Clients PB) that they wish to trade

- Bank A extends credit, or has credit already extended to Client

- Bank A executes the trade with Bank X (or Bank A has given Client an ability to trade in the Bank A name on a platform)

- Result of trade is Bank A -> Bank X

- Bank A then executes that same trade with Client, or tells Bank X “hey just kidding, you traded with this Client”

- Commission is charged or a spread is used between Client and Bank A

Assuming you understood all of that, you can forget it, because that is not what is going on at places like UBS Neo. What I have described above seems to be more of what I’ve heard called “Sponsored Access” in swaps.

SPONSORED ACCESS

Sponsored Access in other asset classes allows firms to use a banks infrastructure, membership, and or platform to transact. So the client trades directly on a SEF (any SEF) using their FCM’s membership, and of course then clear the trade via that same FCM. Much like NISA did on Bloomberg SEF using Credit Suisse as their FCM in this press release.

I presume a commission is charged.

And because in this case Bloomberg is a disclosed RFQ, the executing bank would know it was NISA on the other side.

AGENCY EXECUTION

That is different from Agency. Under the agency model, it seems you have two choices to execute and you are not beholden to your agency execution firm to clear through them as well. Your execution options are:

- Call up the agency desk and have them perform an RFQ for you in your name

- Use the aggregated order book to place or hit orders (the order book that is the combination of 5+ SEFs order books)

In either case, the Client’s credit has to be checked. So the Clients FCM explicitly allows the proposed trade to happen, and this is done presumably via the Credit Hub.

The wrinkles however seem to be:

- Using an order book requires your name to be disclosed post-execution. The consequences of this discussed on a previous blog

- You’ll likely get a better price doing an RFQ

- If it’s an RFQ being done, why bother having someone else do an RFQ for you?

WHY YOU GET A BETTER PRICE ON RFQ

It would seem that there are a couple reasons clients get a better price over RFQ:

- Banks simply prefer to give better prices when their name is disclosed up front, as this information is valuable

- Order books just are not terribly deep on the surface

What I mean by that last point is I have come to learn that a significant amount of volume on the IDBs is being done via workup. So the order book will show, say, size of 25 million at the best bid and offer. However as soon as a trade is done at that level for 25m, either party can elect to say they want to do more at that price, at which point the other party, or any participant can join in at that price.

What this means, is that if I am a client looking to execute 100 million, I simply will not find that much at the best bid or offer. Whereas I will of course get a bank to quote any size for me over RFQ.

As an aside, I think one of the reasons banks don’t want clients in an IDB order book is they fear that clients will game the system by resting an order and then going out to shop it around as an RFQ.

BUT WHERE IS THE LIQUIDITY

So it would seem that the primary reason to use an agency to execute trades at the moment is to streamline the connectivity to multiple SEFs. But hold on, where is the liquidity in RFQ’s on SEFs?

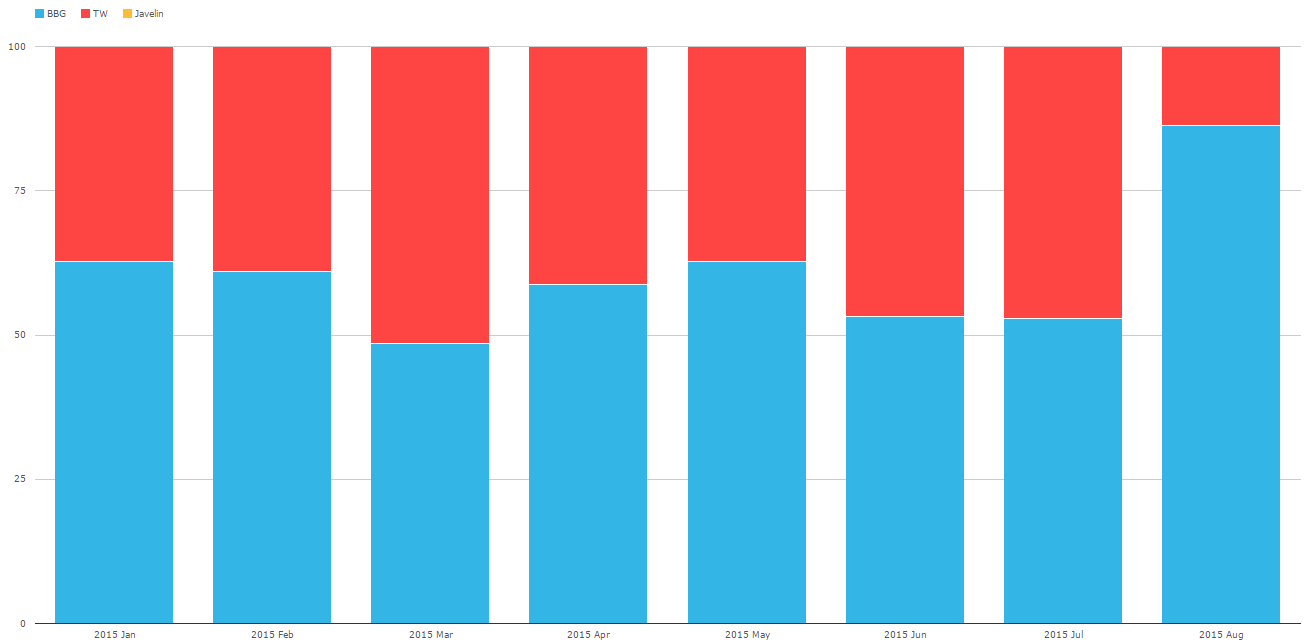

In IRD, among the client SEFs, you can quickly make out that Bloomberg and Tradeweb are the two places to be:

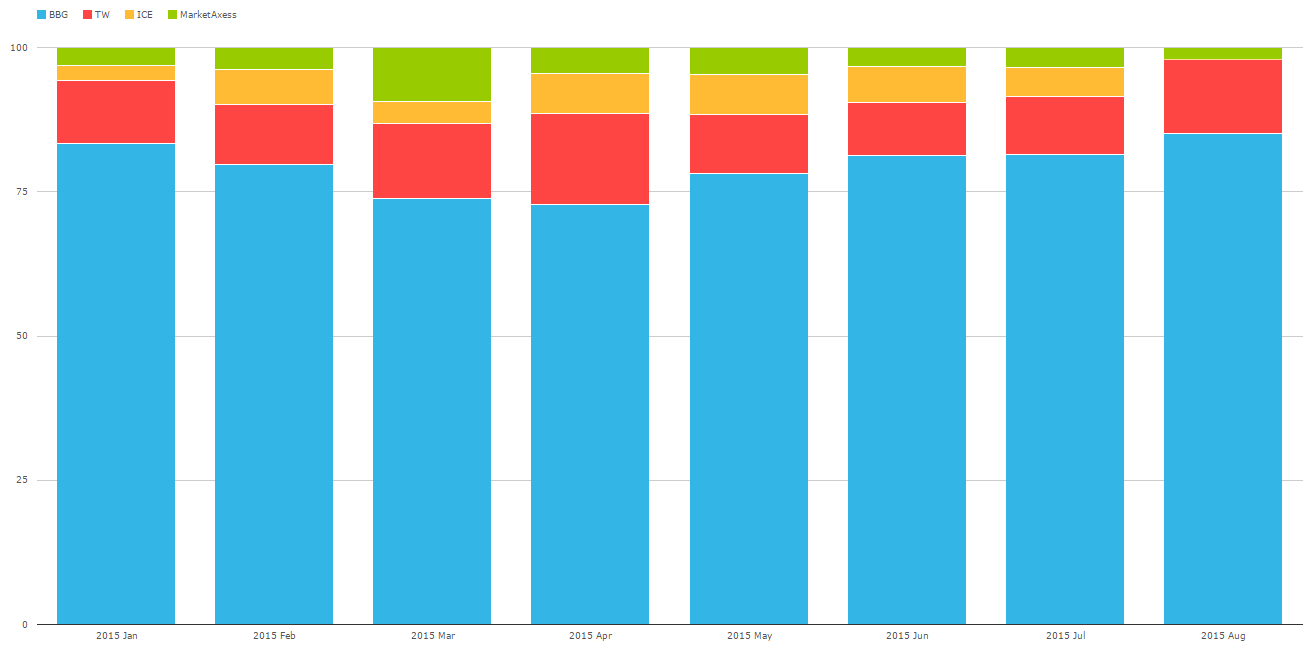

And in Credit, while the picture is slightly more diverse, it doesn’t seem like there is really much choice. Certainly not the “20” SEFs that we hear talked about.

Of course, if we throw D2D SEFs (IDBs) into the mix, those charts change significantly, but that should not be included yet, due to post-trade disclosure.

POTENTIAL UPSIDE FOR AGENCY

If you read through all the CFTC rules and regulations, there is a regulation 1.35 that says that direct SEF members need to have some pretty serious (and tedious) record-keeping practices in place. I believe this involves every firm needing to keep records of chats, text messages, phone conversations, etc. Which I would imagine would be very onerous. However the CFTC granted relief for this a while back and I don’t believe there has been any pressure to remove that relief.

SUMMARY

So really, until the wall between client & dealer markets is dismantled, perhaps via post-trade anonymity, there is just not that much of an argument for aggregation of prices. That, or if the CFTC come out and become more strict on compliance for every firm that uses a SEF under regulation 1.35.

Not sure when either of those days will come.