- Eurex have recently seen increased volumes in both €STR and EURIBOR futures.

- ICE have seen continued traction in €STR futures with their incentive programme yielding about a 27% market share so far.

- CME continue to see most of the Open Interest in €STR futures.

- The exact requirements of an Active Account in Europe are currently being worked out.

Almost exactly a year ago, the EU proposed:

Requiring market participants subject to a clearing obligation to clear a portion of the products that have been identified by ESMA as of substantial systemic importance through active accounts at EU CCPs.

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52022PC0697

The unknown in the past 12 months has been how the EU will define the “Active Account Requirement (AAR)“. In the past few days, we have had announcements from both the European Parliament and the European Council regarding the Active Accounts. It seems we may finally have some clarity in Q1 or Q2 next year.

European Parliament

The European Parliament press release includes the following text on Active Accounts:

- The requirement to clear at least a proportion of trades through the active account should be phased in gradually.

- An account is considered active if;

- It posts initial and daily variation margins;

- Has in place the necessary IT connectivity, internal processes and legal documentation;

- Can demonstrate that its functioning would not be affected in the event of a significant and sudden increase in clearing activity.

European Commission

The European Commission negotiating position runs to 144 pages and includes the following on Active Accounts:

- A number of derivative contracts should be cleared in the active accounts.

- Contracts with different maturities and different sizes should be cleared through the active accounts.

- All new trades of the respective counterparty in the derivative contracts can be cleared in the account (CB: if a counterparty has above EUR6bn notional outstanding);

- i. different classes of derivative contracts (CB: IRDs in EUR and PLN plus EUR Short Term Interest Rates are explicitly named, but the text states “up to a limit of three classes”);

- ii. maturity of the trades (CB: up to four maturity ranges, TBD by ESMA);

- iii. trade sizes (CB: up to three trade size ranges, TBD by ESMA).

- Duration of the reference period (CB: 1-6 months depending on whether you have more than or less than EUR100bn outstanding).

- ESMA will review after 24 months and annually thereafter.

EUR CCP Market Share

The European Commission referenced ClarusFT data as part of their “collection and use of expertise” resources:

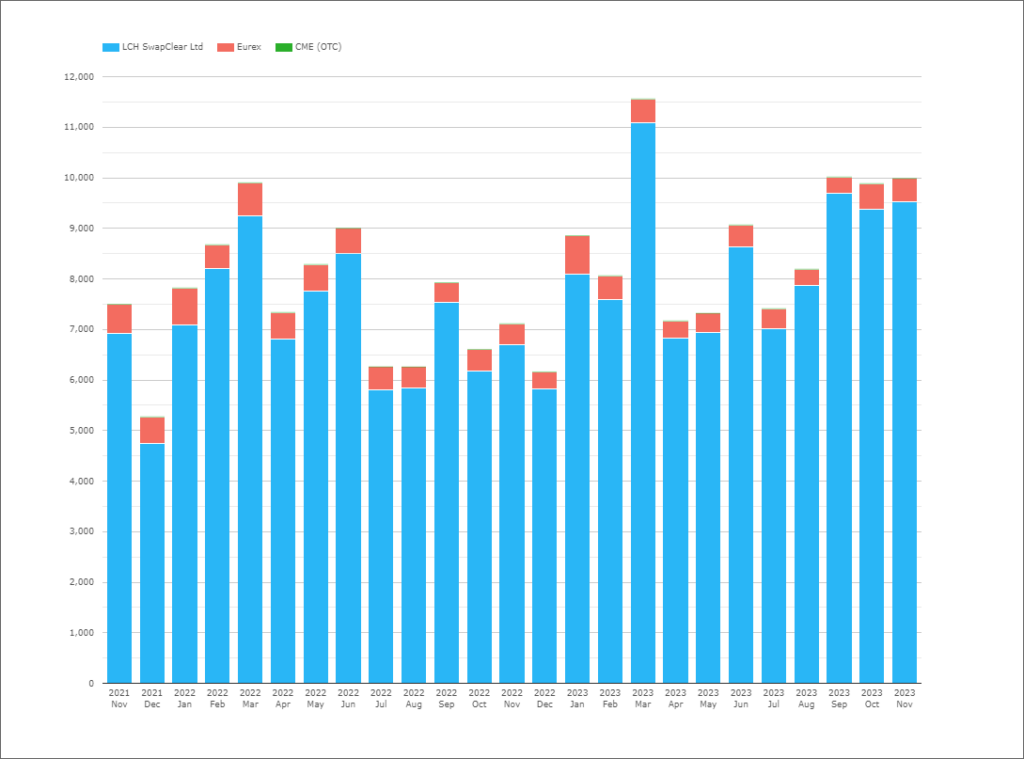

Let’s therefore refresh the data for CCP market share in EUR IRDs.

IRDs: EUR Rates Market Share – All Products, DV01

Our readers must by now be familiar with our preferred measures of market share. In case not, please refer back to some of our previous blogs.

Showing;

- DV01 removes any distortions from large notional, short-dated trades therefore we can include all Rates products here – IRS (vs Euribor), OIS (vs €STR), FRAs.

- DV01 is a fair measure of market share in terms of risk traded across all EUR rates products.

- EUR Rates markets are now larger than USD – this is the first time I have seen this for many years.

- Eurex market share has declined slightly from the middle of 2021.

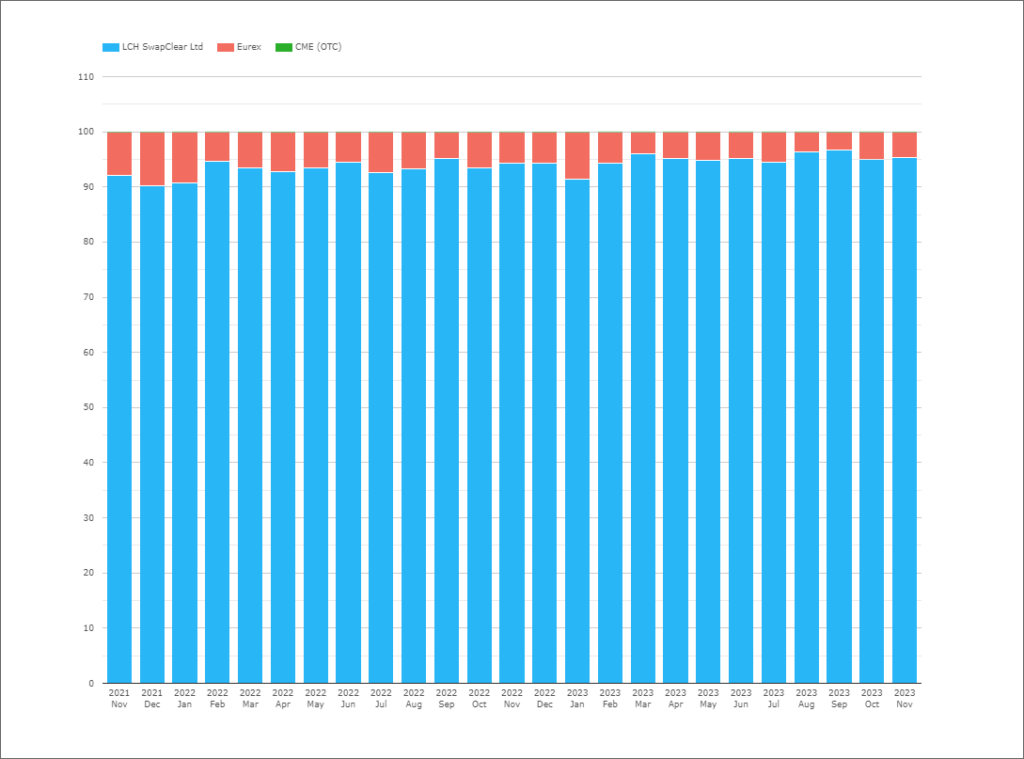

- The next chart shows the market share:

Showing;

- Eurex had a 9-10% market share of all EUR Rates products (in DV01 terms) in Dec 21/Jan 22.

- Since that high point the Eurex market share approached 9% once more, in January 2023.

- September 2023 saw the lowest market share for Eurex, at 3.2%.

- It has since recovered recently to 4.5-5%.

- LCH SwapClear continue to enjoy a 95%+ market share.

Amir covered similar data in his blog 3Q23 CCP Volumes and Share in IRD. The same blog noted that the Eurex market share is lower in OIS than IRS.

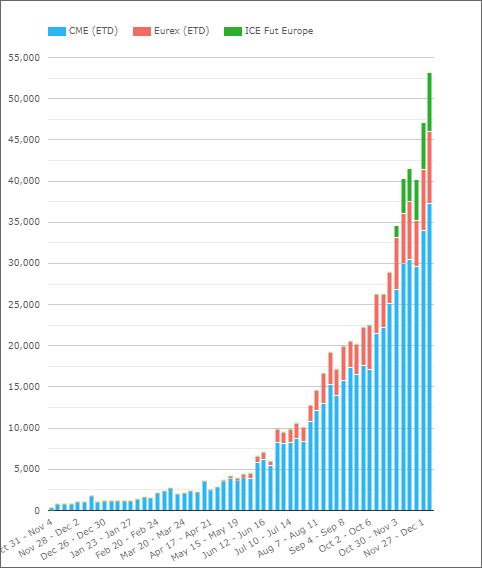

Futures: EUR Rates Market Share in Short Term Interest Rates

If nothing much seems to be changing with the OTC swaps data, the same cannot be said for Short Term Interest Rate futures. Since I wrote the last blog just one month ago, the fledgling €STR dashboard is already showing some interesting data:

- The last blog noted how well ICE was doing within just a few days of the launch of their market making programme.

- Since that point, I would note that there are new aspects in the data:

- Eurex volumes have increased significantly, getting as high as 60% market share.

- CME market share is around 20% – but 70% of Open Interest is still in CME €STR.

- ICE volumes have been a bit up and down, but they have seen a 27% market share since the launch of their incentive programme.

- Speaking of Open Interest, it looks like ICE is quickly catching up Eurex in €STR, but that CME continues to lead the way:

I also read this week that the RFR Working Group in Europe has been disbanded – see here. I have no idea what that means for the future of EURIBOR, but in the context of this blog it is the overall “Short Term Interest Rate” product that is a “class of derivative” for the purposes of the Active Account. We are therefore also interested in tracking EURIBOR futures.

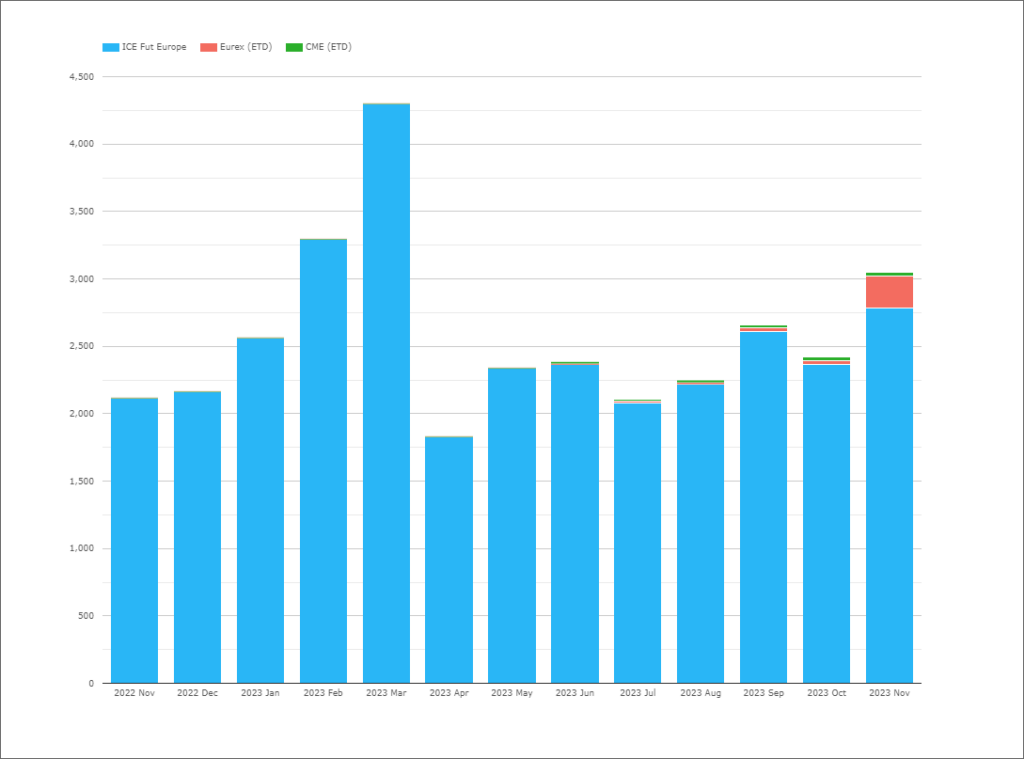

And it looks like Eurex is making a fresh push into EURIBOR futures. See below from CCPView:

Showing;

- Eurex with a 7.7% market share in November from less than 1% previously.

- This against a backdrop of increasing volumes in EUR STIRs.

- November 2023 saw the second largest volumes, outside of a roll month, in 2023.

- The data shows that volumes are really healthy – ICE seeing two of the largest volume weeks of the year in the past two weeks.

- Open Interest in EURIBOR futures has now also risen to the highest levels for at least the past three years. It looks like bets on Rate cuts next year are leading to a large increase in EURIBOR activity.

- Something is certainly happening here and the data will be interesting to monitor:

- Given the success of Eurex in FRAs, are the volumes in EURIBORs related?

- Is the Eurex EURIBOR volume true “new” volume or trading as spread to ICE, hence elevating overall volumes?

- An interesting one to monitor….

In Summary

- The Active Account Requirement is being fleshed out in European political and regulatory circles in the coming months.

- We assumed that all the focus would be on OTC derivatives in EUR…

- ..and in the on-going developments in €STR market share.

- However, there are new developments in EURIBOR futures which are now worth monitoring.

- The data is going to be make interesting reading in 2024.