- All we wanted for Christmas were new block sizes in the SDR data….

- …unfortunately that won’t be happening this year 🙁

- 50% of notional will continue to be above the reporting thresholds.

- With the industry continuing to push back against the new calibration.

Back in June 2023, I covered the new block sizes that were due to come into effect on 4th December 2023. In case you missed them, please take a look before reading today’s blog:

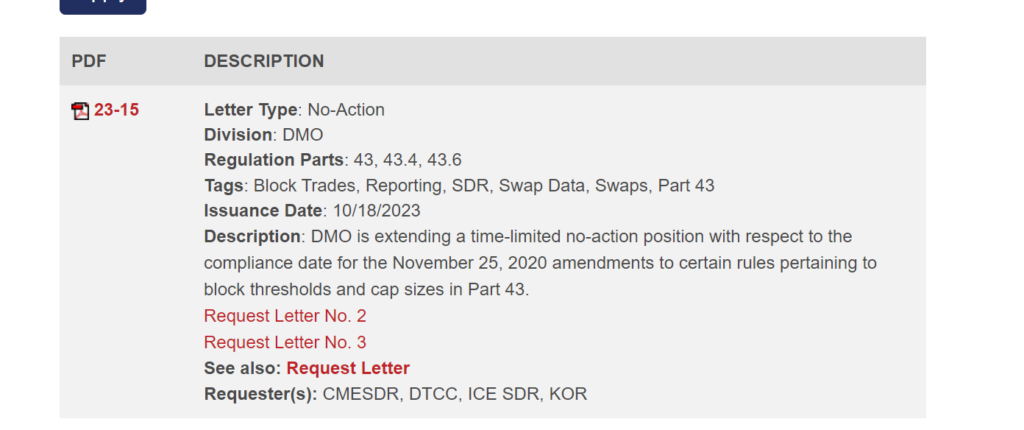

However – in what appears to be new news – the CFTC issued a No Action letter late in October to delay the change (again!) to July 2024. I haven’t seen this covered in any of my usual news feeds, so I had to go hunting through the CFTC releases until I found this:

Which states;

Division will not recommend that the Commission commence an enforcement action against an entity for failure to comply with the Block and Cap Amendments before July 1, 2024

CFTC Letter No. 23-15 No-Action October 18, 2023 here

October GMAC Meeting

Really motivated readers could also sit through the two-and-a-half hour recording on YouTube of the most recent GMAC meeting. Or you can take advantage of the fact that I managed to find time to do exactly that this week, and so click on the relevant time-stamped snippet below instead:

In which we discover:

- A sub-committee has recommended an even further extension to a change in the block sizes until December 2024!

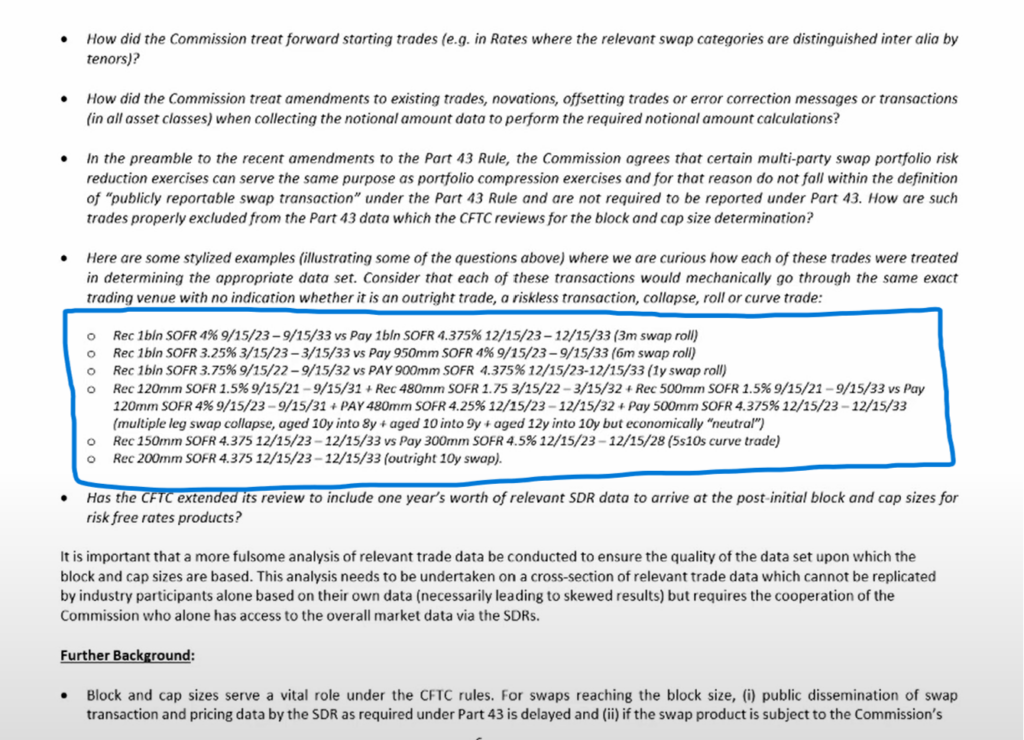

Why? In a nutshell, there are concerns that the block sizes are larger. From the presentation:

- “The new sizes reflect in many cases drastic increases (in multiple cases around 10 times higher)”

- “How did the Commission arrive at a cap size of $2.643 billion for gold when the current block size is around $5 million?”

From the context provided in the slide, it appears that the subcommittee is requesting that the Commission engages with the industry to sanity check their calculations, rather than publishing them and then waiting for feedback. That does sound like a sensible step, although it must surely risk stasis/only hearing arguments for smaller block sizes. A tricky one to balance.

Methodology

Further, it looks like there the industry is gearing up to challenge how the Block thresholds are calibrated. Elsewhere in the presentation, very specific examples are given, with a subtext that these should not be used to calibrate the size of a block trade. I am not sure I exactly agree with this, because it is leading us down a path whereby block sizes would be different for outrights and packages. I don’t think there is any consideration of that in the current Rules, and it would surely make implementation of new block sizes considerably more difficult if it were to be introduced.

The Clarus Quick Take

We find it frustrating that these new limits have been available since April 2023 and all that the industry has managed to do in the past 8 months is push back against them and ask for delays. Transparency is repeatedly recognised as beneficial to the OTC markets. We 100% agree that very large trade sizes should be given additional publication time and execution flexibility, allowing dealers time to hedge the risk (please note “very large“). That does not mean that 50% of notional should be masked or that “RFQ-to-few” should be the default SEF execution protocol just because it has been like that for ten years now.

The limits need to be changed.