In this article I will look at a Forward Start Interest Rate Swaps and the Initial Margin requirement for such a trade.

We know from SDR data that Forwards Swaps are a very common trade type and if you are a regular reader of our blog, you will know that they represent the majority of Swap types that are Off SEF. Forward Swaps are also a common client trade as the forward periods are used to match a specific asset or liability.

Our example

Lets start with an example and a chart.

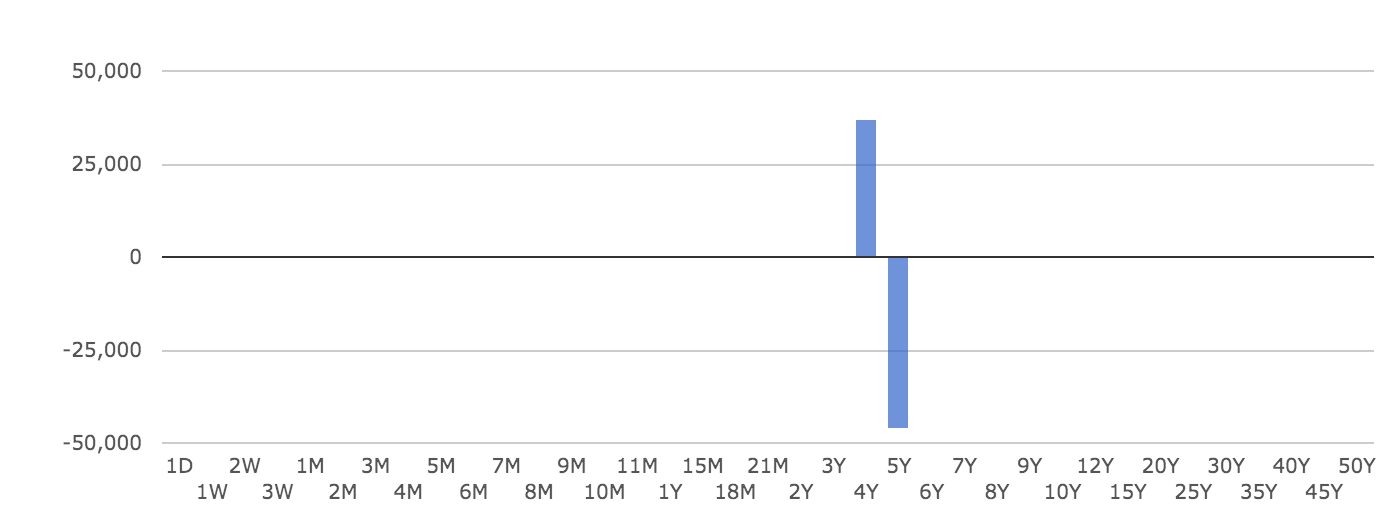

Take a 4Y into 1Y forward , where we receive fixed on $100m notional. So in 4 year’s time, we will receive semi-annual fixed coupons and pay quarterly Libor 3m for a 1 year period and then the swap ends.

The Delta by tenor profile of such a trade is as follows:

So while the net Delta (or DV01) is -$9,000, we can see that that 4Y Delta is +$37,000 and 5Y Delta is -$-46,000.

This suggests that a way we can construct the same Delta exposure as our 4Y into 1Y receive fixed is to pay fixed 4Y and receive fixed 5Y in a spot starting swap. So we will also construct a second example of two such trades to replicate the risk profile of our forward swap.

Initial Margin

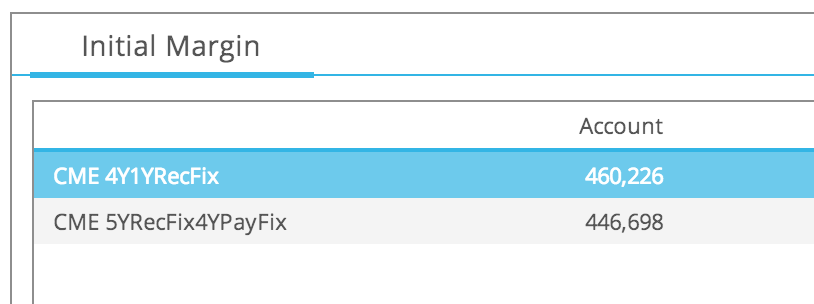

Lets now use CHARM to run Initial Margin assuming clearing at CME for both examples.

Which shows an IM of $460k for the forward and $450k for the two spot trades. Near enough the same.

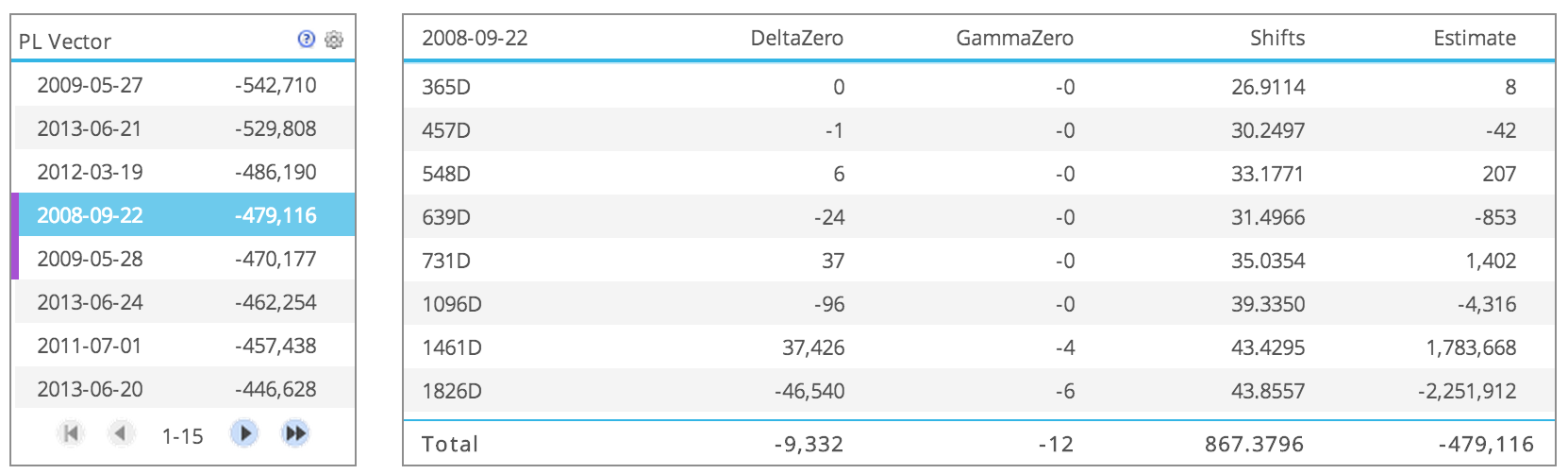

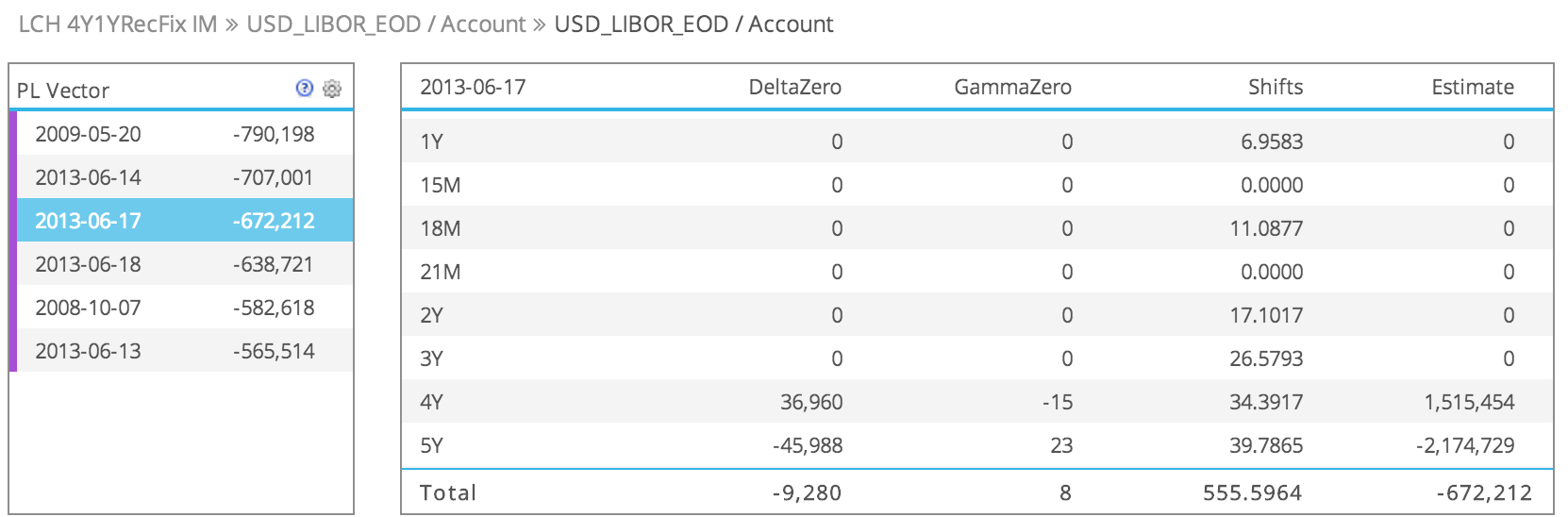

Lets now drill-down in CHARM to see the explanation for the IM.

Which shows that:

- the IM is determined by the 4th and 5th largest loss scenarios

- the fourth is for scenario date 22 Sep 2008 and shows a loss of $480k

- the Delta for 4Y (1461D) is $37k and the shift on this scenario is +43 bps

- the Delta for 5Y (1826D) is -$46k and the shift on the scenario is +43 bps

- each contributes in opposite amounts to the overall loss of $480k

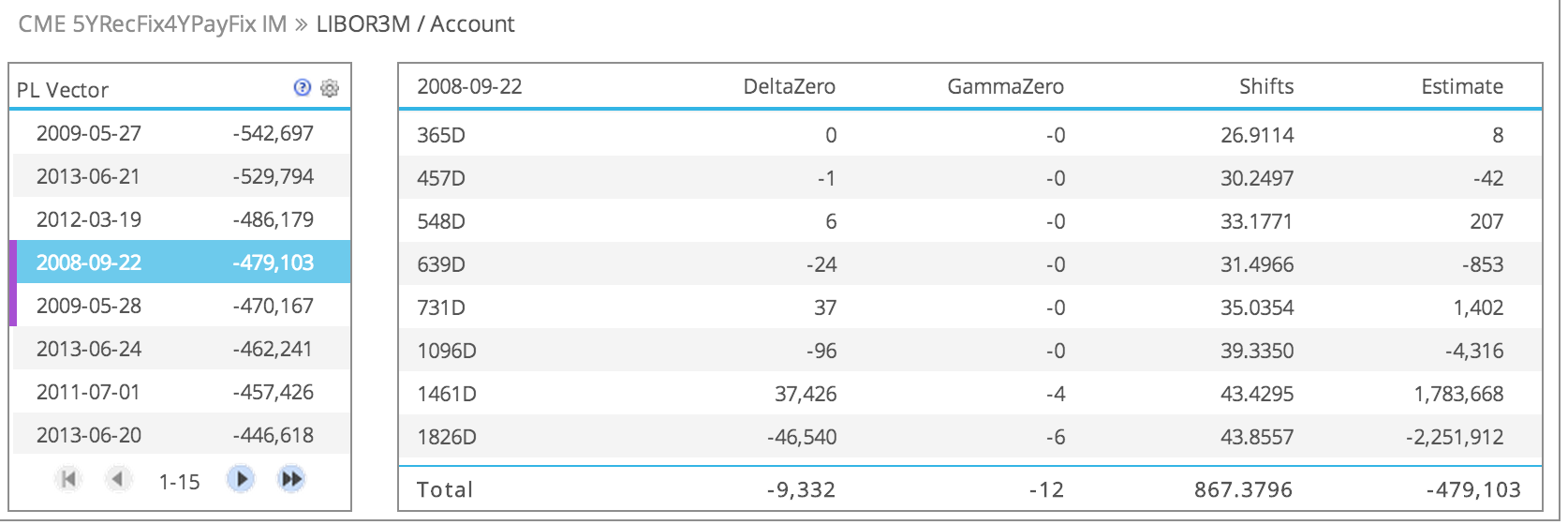

Doing the same drill-down for our two spot trades shows almost identical numbers.

So it is good to know that the two margins are almost identical, as the risk of our forward trade and two spot trades is the same. It would be a real concern if the margins were different.

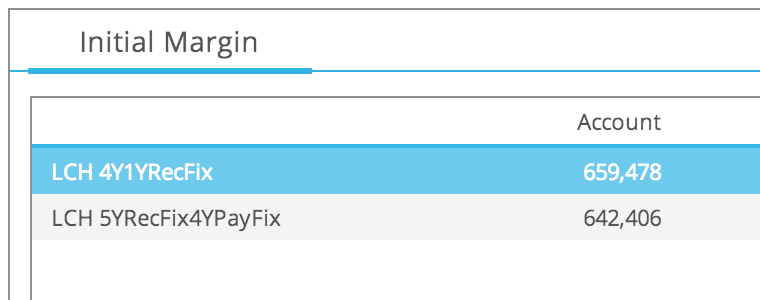

LCH Margin

Lets also run the same examples assuming clearing at LCH.

Again very consistent with each other.

And a little higher than CME, as we would expect given absolute returns versus relative returns in the margin model.

And the drill-down is as we would expect.

IM is determined from Expected Shortfall of the tail scenarios. One of which is explained by the 4Y and 5Y Delta and PL contribution of each to the Loss.

So there you have it, detailed examples of our swaps.

Now a slight digression.

Approximations and Look Up Tables

A common approach in Client Clearing is for Clearing Members to use look-up tables of IM per $1million for standard spot tenors. These look-up tables are often provided to Credit Hubs to implement a clearing acceptance certainty check.

How would that work for our forward start swap?

Well we could look-up an IM for a 5Y Rec Fix Swap and scale to $100 million. (from my recent blog, CME IRS Margin Model Change, we know that this is approximately $2million.)

So we could just use $2 million as a gross IM check. Very conservative and hardly a good use of Clients Margin, when the real figure is $460k for CME.

Well lets improve by using our 4Y and 5Y replication above.

In this case either we then look-up a 4Y Pay Fix or interpolate between 2Y and 5Y (yipes, hang-on). Lets say this gives us $800k for our 4Y Swap. So subtracting from $2million, we get an IM of $1.2 million. Better but still a long way from $460k.

We could construct look-up tables for forwards, but the possible combinations are daunting ….

So not much else to be done but tell the client that this is a crude intra-day acceptance check which is conservative and they need to provide funds to cover this but when the overnight portfolio margin runs it will be handled correctly and they don’t really need the funds just a buffer. 🙂

Or we could simply ignore the automated check failing and manually override to accept the trade to clearing. But we know where manual processing can lead in market stress situations, not a place we want to be in when a panic is on.

So the lesson of our digression?

Clients do lots of forward start swaps and it is far better to margin these correctly in a clearing risk process than use look-up tables.

Summary

Forward Start Swaps are a very common client trade.

In risk terms they can be represented by two spot swaps in opposite direction.

We construct a portfolio with both and use CHARM to run Initial Margin on both, showing that the IM is the same as we would expect. So there is no bias or anomaly in the margin models between Spot and Forward Swaps.

Look-up tables of IM for Spot Swaps are commonly used in a Clearing acceptance process.

We show that this is a crude approximation that leads to over-funding of margin or manual overrides for breaks.

It is far better to calculate IM for forwards correctly.

If you are a client ask your FCMs what approach they use.

If you are an FCM, check you are satisfied with your current process.

Thats it for today, thanks for reading this far.