- We look at what traded off-SEF in 2018 across Rates markets.

- As a result of the CFTC’s proposed rule, we look at products that are mandated to clear.

- We find that most off-SEF volumes are in short-dated FRA and OIS products.

- For Fixed-Float traded off-SEF, 75% of it is forward starting.

Introduction

We are always grateful when our work is quoted. This time, it is the CFTC who have looked at one of our 2016 blogs, and cited the following:

“Clarus [found] that approximately two-thirds of the fixed/float USD interest rate swap market is traded on SEF. Examining the one-third of interest rate swaps that are being traded off SEF, Clarus found that ‘‘[g]enerally speaking, everything off-SEF is bespoke.’’

The old blog that they refer to has always been popular. Seeing as it has now found its way into a recent proposed rule-making by the CFTC, I thought it would be a good time to update the analysis!

In terms of the rule making itself, there is already a great overview up on the Clarus blog here. In today’s blog, I will concentrate on updating our original analysis – although I cannot help thinking of the numbers through the lens of “what if everything that had to be cleared also had to be transacted on-SEF?” and “should we really be changing how a SEF is allowed to transact trades”?

Clearing Mandatory

In response to this latest rule making from the CFTC, Clarus have added a “Clearing Mandatory” filter to our data products. The following analysis has therefore been run only on products subject to the Clearing Mandate. This makes it relevant for the current rule making proposal.

Clearing Mandated Rates Activity

Given the rule-making involves the MAT process, I thought we would lead with a breakdown of MAT vs Non-MAT and their execution methods – SEF or off-SEF. The charts look at all trades subject to the Clearing Mandate (i.e. across 13 currencies).

![]()

Showing;

- The split by Notional and DV01 of trades subject to the Clearing Mandate. This covers Fixed-Float, FRAs, Basis and OIS – i.e. all Rates products.

- On a notional basis, just 9% of Clearing Mandatory volumes are executed on-SEF and are “MAT” products.

- 1% are MAT products executed off-SEF – let’s assume these are trades with end-user exemptions, inter-affiliate trades or just bad data.

- 54% of volumes (by notional) are being voluntarily executed on-SEF.

- 37% of volumes are executed off-SEF.

This picture looks considerably different when measured on a DV01 basis.

- 33% of risk is made up of MAT products executed on-SEF.

- The non-MAT products that are executed on-SEF sees their proportion drop considerably to 32%. We will look at these in a future blog.

- 36% of risk is executed off-SEF – almost identical to the notional measure. These are the volumes we will analyse today.

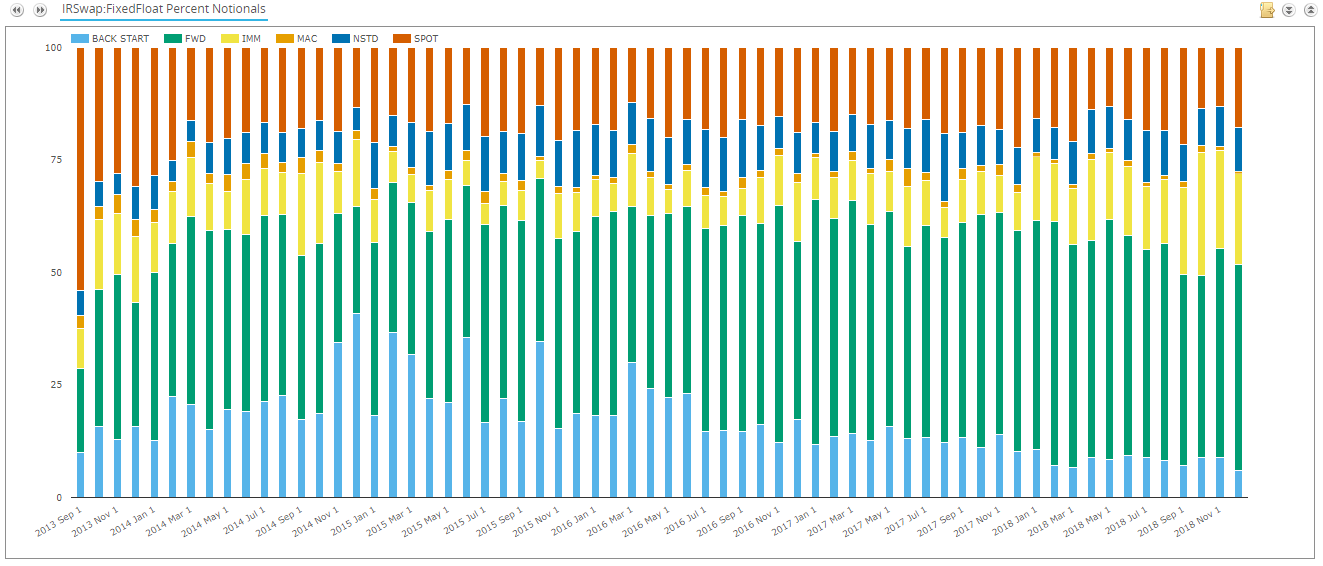

What still trades Off-SEF in USD Fixed-Float?

Our old blog looked at USD Fixed-Float swaps only. So let’s update that chart first, looking at the types of USD Fixed-Float swaps that trade off-SEF. We see the following (in notional terms):

Showing;

- 48% of off-SEF USD Fixed-Float notional is traded as a forward-starting swap. Including IMM swaps increases this to 65%.

- 17% is traded as a Spot swap (let’s assume in non-MAT maturities).

- 8% is back-starting. Notably, this has shrunk since our blog in 2016. Maybe as more compression moves on-SEF?

- 9% are “non-standard” swaps. So either upfront fees, zero-coupons, monthly or with a flag recognising “other price effecting terms” associated with it.

- The rest is split by IMM and MAC.

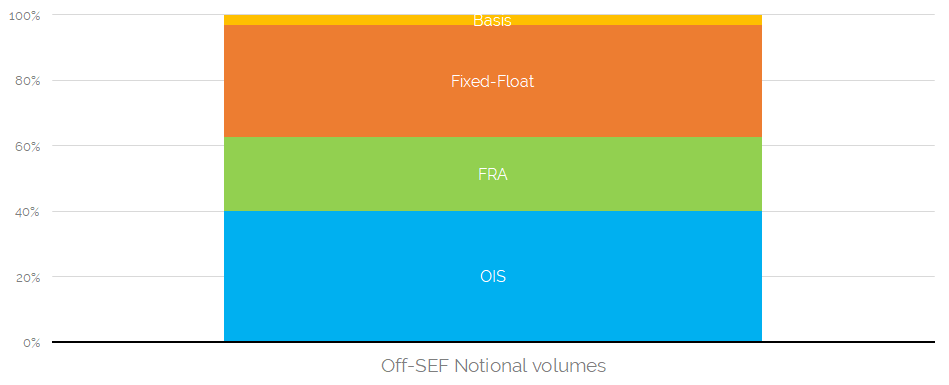

What Products are traded Off-SEF?

Turning our attention to the broader Rates market, let’s take a look at the products that trade off-SEF across all 13 currencies subject to the Clearing Mandate.

Showing;

- 40% of volumes are in OIS.

- In fact, FRAs and OIS make up 63% of off-SEF volumes by notional.

- From SDR data, we find that 93% of FRA and OIS are one year or less in maturity (measured by notional). This means that the vast majority of notional volume transacted off-SEF is therefore in short-dated risk.

- 37% is in Fixed-Float and Basis. We analyse the Fixed-Float volumes later in this blog.

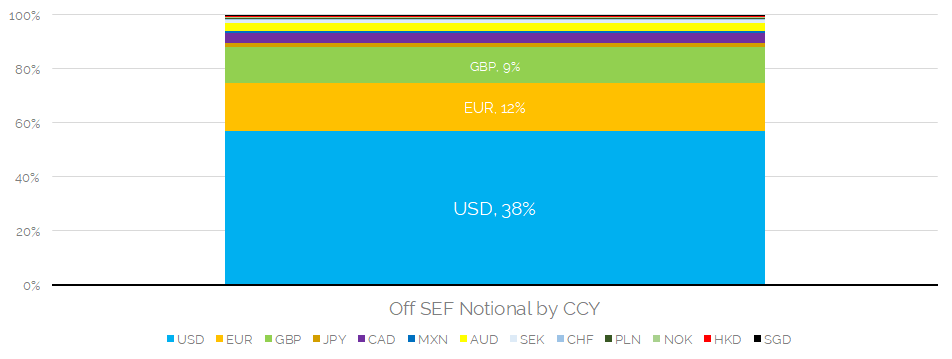

What Currencies are traded Off-SEF?

Looking in more detail, I wanted to know the break-down by currency. Looking on a notional-basis and across all Rates products subject to the Clearing Mandate (Fixed-Float, FRAs, OIS, Basis):

Showing;

- USD is the most prominent currency with 38% of volumes.

- 61% of volumes are made up of the top four currencies – USD, EUR, GBP and CAD.

- That leaves a very long tail of the remaining nine currencies making up less than 2% each of the total off-SEF traded notional.

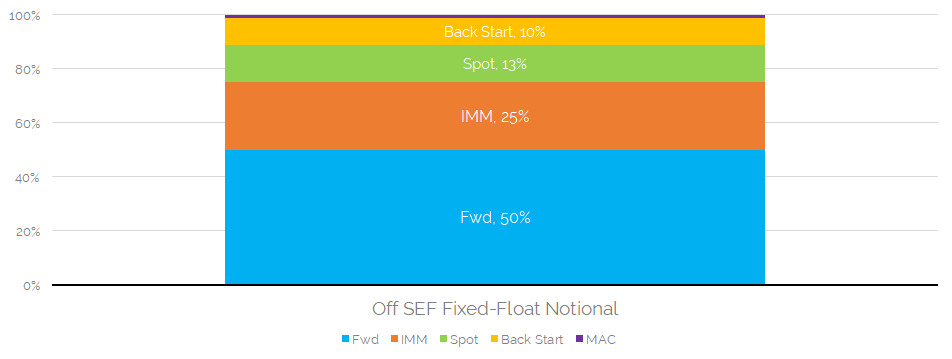

Which Fixed-Float Products are traded Off-SEF?

It is also interesting to consider the mixture of Fixed-Float products that are traded off-SEF. Looking across all of the currencies subject to the Clearing Mandate, is there any difference to the distribution compared to the USD off-SEF market we looked at previously?

Showing;

- Even more forwards here! 75% of notional traded off-SEF is either a Forward or an IMM (this is 65% for USD Fixed-Float).

- 13%, are Spot-starting.

- Just 10%, are back-starting. This must show the preference for on-SEF compression these days?

Part One Summary

I’ve run out of words, space, time and charts to complete the exercise of looking into the data behind the CFTC’s proposal. Next time, I’ll look at voluntary SEF trading, which SEFs had volumes in 2018 and analyse more of the trading on D2C SEFs.

For now, suffice to say that;

- Only 31% of risk is currently traded off-SEF.

- Of this, much of the notional amounts are in OIS and FRA products, which are short-dated in nature.

- Most of the Fixed-Float swaps that are traded off-SEF are forward-starting.