Clearing Houses have published their latest CPMI-IOSCO Quantitative Disclosures:

- Initial margin for ETD at $480 billion is up 3.5% QoQ and 3% YoY

- Initial margin for IRS at $314 billion is down -5% QoQ and -7.5% YoY

- Initial margin for CDS at $60 billion is flat QoQ and down -13% YoY

- In 1Q24 a number of CCP quantitative disclosure show record highs

- Highlighted are BME, CC&G, CCIL, CDCC, CFFEX, CME, DTCC, Eurex, …

- Please continue to read for all the details

Background

Under the CPMI-IOSCO Public Quantitative Disclosures, CCPs publish over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing and more.

CCPView has over 8 years of these quarterly disclosures for 44 Clearing Houses, each with multiple Clearing Services, covering the period from 30 Sep 2015 to 31 Mar 2024. This disclosure data provides insights into trends over time at one CCP and comparisons between CCPs.

Let’s take a look at the latest disclosures.

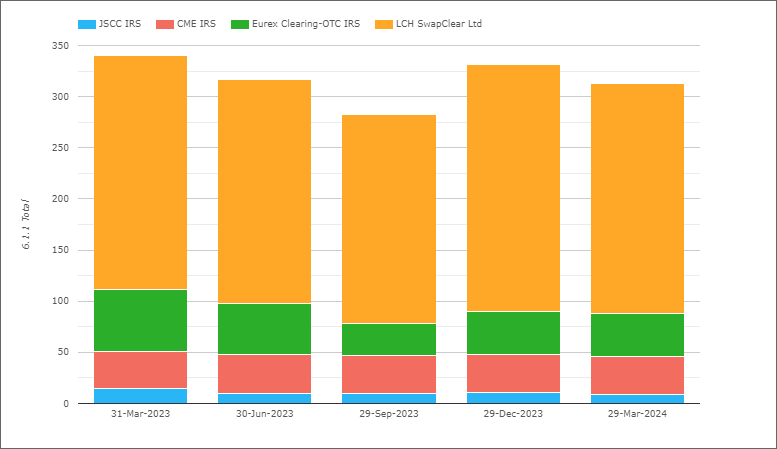

Initial Margin for IRS

- Total IM at these four CCPs was $314 billion on 29-Mar-2024

- Down $18 billion or 5% QoQ and down $25 billion or 7.5% YoY

- LCH SwapClear with $225 billion or £179 billion on 29-Mar-2024

- Down 5% QoQ and 3% YoY in GBP terms (Down 7% QoQ & 2% YoY in USD terms)

- Eurex OTC IRS with $41.8 billion or €38.7 billion

- Up €1.1 billion or 3% QoQ and down €16 billion or 30% YoY (in EUR terms)

- CME IRS with $37.4 billion, flat QoQ and Up 4.5% YoY

- JSCC IRS with $9.4 billion or Y1,426 billion, Down 10% QoQ and 26% YoY (in JPY terms).

Total IM for IRS at $314 billion is down from the all-time high of $339 billion on 31-Mar-2023.

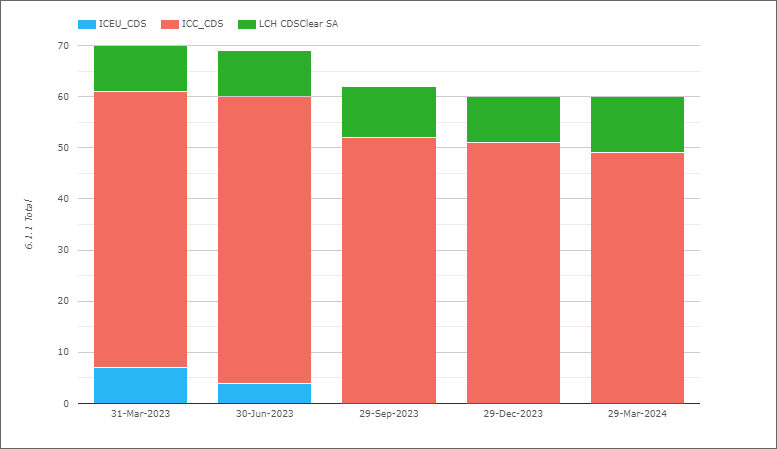

Initial Margin for CDS

- Total IM at the two CCPs was $60 billion on 29-Mar-2024

- Flat QoQ and down $9 billion or 13% YoY

- ICE Credit Clear with $49 billion

- Down $1.7 billion or 3% QoQ and down $4.3 billion or 8% YoY

- LCH CDSClear with €9.9 billion

- Up €1.9 billion or 24% QoQ and Up €2 billion or 25% YoY

- ICE Europe Credit now closed

With ICE Europe Credit now shut down, there are greater netting benefits for member and client accounts at 2 CCPs as opposed to 3, which goes some way to explaining the lower level of CDS IM at $60 billion from the $69 billion a year earlier.

Initial Margin for ETD

- Total IM for these CCPs was $480 billion on 29-Mar-2024

- Up $16b or 3.5% QoQ and Up $15b or 3% YoY

- (Note the chart shows higher totals as Eurex includes OTC IRS IM, which I exclude)

- CME Base with $205 billion, up 1% QoQ and up 8% ($16b) YoY.

- OCC with $102 billion, up 13% QoQ and up 36% ($27b) YoY.

- ICE Europe F&O with $74 billion, down 6% QoQ and down 22% ($21b) YoY.

- Eurex with $48 billion, up 8% QoQ and down 16% ($9b) YoY.

- ICE US F&O $17 billion, up 7% QoQ and 8% YoY.

- JSCC OSE Listed ETP with $16 billion, Up 17% QoQ and up 13% YoY

- SGX-DC $8.5 billion, up 7% QoQ and up 17% YoY

- HKEX HKCC with $5.9 billion, down 6% QoQ and down 23% YoY

- ASX CLF ETD $4.2 billion, up 14% QoQ and down 14% YoY

IM at all CCPs of $480 billion is the highest in the time series shown, with CME, OCC, ICE US, JSCC and SGX each materially higher YoY.

Other Disclosures of Interest

Next let’s do a quick scan of 29-Mar-24 disclosures, highlighting those with significant changes.

- BME (Borsa Mercados Espanoles) – 5.3.4 Number of days during the look-back period on which the fall in value during the assumed liquidation perdod exceeded the haircut on an asset was 4, up from 2 and the highest since 30-Sep-2020

- BME Financial Derivatives – 6.2.15 House IM PreHaircut was €1.23 billion, up from €1.1 billion and the highest on record

- CC&G Equities – 6.1.1. Total initial margin required was €5.6 billion, up from €3.4 billion, a record high

- CC&G Equities – 4.4.3 Estimated largest aggregate stress loss (in excess of IM) that would be caused by the default of any single participant in extreme but plausible market conditions, MeanAverage over the previous 12 months was €815 million, up from €678 million, also a new high

- CCIL Securities (Outright & Repo) – 6.8.1 Maximum aggregate IM call on any given day over the period was $2.4 billion, up from $1.7 billion, a new record high

- CDCC (Canadian Derivatives Clearing Corporation) – 6.5.1.1 Number of times over the past 12 months that margin coverage held against any account fell below the actual marked-to-market exposure of that member account was just 3, down from 46, 57, 64 & 90 in prior quarters, which is a significant drop and a good outcome.

- CDS (Canadian Depository for Securities) – 4.4.3 Estimated largest aggregate stress loss (in excess of IM) that would be caused by the default of any single participant in extreme but plausible market conditions, PeakDayAmount over the previous 12 months was $1.4 billion, up from $540 million, a new record high, the prior being $980 million in 31-Mar-22

- CDS– 4.4.5 The amount in 4.4.3 which exceeded actual pre-funded default resources (in excess of IM) was $912 million, the only time it has been above zero, except 30-Jun-22 when it was $20 million.

- CFFEX (China Financial Futures Exchange) – 6.6.1 Average total VM paid to the CCP by particpants was $375 million, up from $275 million and the highest on record, the prior high being $332 million in 31-Mar-22

- CFFEX – 6.7.1 Maximum total VM paid to the CCP on any given day was $1.6 billion, also a new high

- CME Base – 4.1.4 Prefunded aggregate participant contributions required were $7.5 billion, up from $6.7 billion, a new high

- CME Base – 4.1.8 Committed aggregate participant commitments to address an initial participant default were $20.5 billion, the first time they have exceeded $20 billion, the prior high was $18.3 billion in the previous quarter and I think these are the highest of any Clearing Service except DTCC GSD, which clears US treasuries.

- DTCC GSD – 4.4.7 Estimated largest aggregate stress loss (in excess of IM) that would be caused by the default of any two participants in extreme but plausible market conditions, MeanAverage over the previous 12 months was $3.2 billion, up from $2.7 billion, a new record high

- Eurex Clearing – 4.4.7 Estimated largest aggregate stress loss (in excess of IM) that would be caused by the default of any two participants in extreme but plausible market conditions, MeanAverage over the previous 12 months was €6.2 billion, up from $5 billion, a new record high

- …..skipping down to N…

- Nasdaq Financial Markets – 6.1.1 House net IM required was $2.4 billion, up from $2.1 billion and a new high, while Total IM required of $3.9 billion is less than the $4.5 billion in 30-Jun-23 or the high of $5 billion on 31-Mar-21

- ….. we could go on …..

There are a lot more Clearing Services and Disclosures but I will stop there and leave it to those of you with CCPView access to analyze further changes.

As well as a Web UI, we also offer an API to programatically access this data.

IOSCO Quantitative Disclosures

CCPView has disclosures from 44 Clearing Houses, each with many Clearing Services, covering Equities, Bonds, Futures, Options and OTC Derivatives with over 200 quantitative data fields each quarter and quarterly figures from September 2015 to March 2024.

If you are interested in this data, please get in touch.

Thank you Amir for these wrap documents – it reminds me to keep a watch on the sector

Cheers