Clearing Houses just published their CPMI-IOSCO Quantitative Disclosures, lets look at what’s new:

- Initial margin for IRS remains close to record highs

- Initial margin for CDS down 12% from the high

- Initial margin for ETD down 15% from the high

- OCC and Eurex OTC IRS the only CCPs with IM QoQ up > 10%

- ASXCL, ICE Clear NL and ICE Clear SG are new additions to CCPView

- DTCC GSD, largest payment obligation of one participant, $102 billion!

- DTCC NSCC maximum IM call on a day of $17 billion

- And a lot more below

Background

Under the CPMI-IOSCO Public Quantitative Disclosures, CCPs publish over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing and more.

CCPView has 5 years of these quarterly disclosures for forty Clearing Houses, each with multiple Clearing Services, covering the period from 30 Sep 2015 to 30 Dec 2020. This disclosure data provides insights into trends over time at one CCP and comparisons between CCPs.

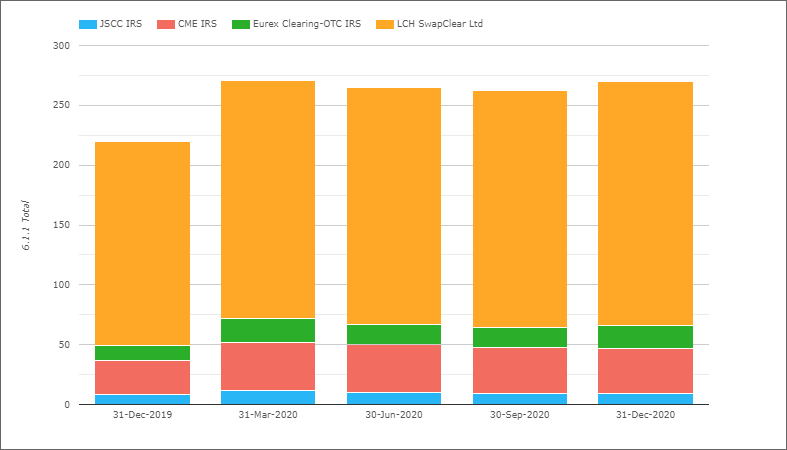

Initial Margin for IRS

- Total IM for these four CCPs was $270 billion on 31-Dec-2020

- Similar to the all time high of $271 billion on 31-Mar-2020

- Up 22% from $221 billion on 31-Dec-2019

- LCH SwapClear with $204 billion or £149 billion on 31-Dec-2020

- Is up 3% QoQ in USD terms, but down 3% in GBP terms

- While YoY, LCH SwapClear is up 19% in USD terms and 15% in GBP

- CME IRS with $38 billion, down 3% QoQ and up 28% YoY

- Eurex OTC IRS with $18.6 billion or €15.2 billion

- Up 14% QoQ in USD terms or 9% in EUR terms

- Up 51% YoY in USD terms or 38% in EUR terms

- JSCC IRS with $9.5 billion or Y977 billion

- Flat QoQ, but Up 16% YoY in USD terms or 10% JPY terms

IM for IRS remaining at the record highs we saw on 31-Mar-2020, the Covid-19 crash quarter. A little surprising that IM has not come down given the lower market volatility, but then again the risk position of members at CCPs on 31-Dec-2020 will not have been the same as on 31-Mar-2020.

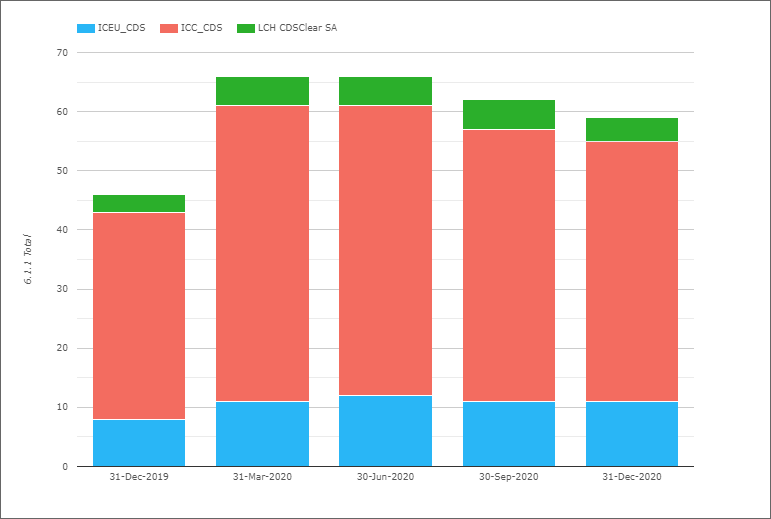

Initial Margin for CDS

- Total IM for these three CCPs was $59 billion on 31-Dec-2020

- Down 12% from the high of $67 billion on 31-Mar-2020

- Up 29% from $46 billion on 31-Dec-2019

- ICE Credit Clear with $44 billion, down 3% QoQ and up 26% YoY

- ICE Europe Credit with $10.8 billion, down 5% QoQ and up 43% YoY.

- LCH CDSClear with $4.4 billion, down 16% QoQ and up 35% YoY.

CDS IM continuing to drift down from the 31-Mar-2020 high.

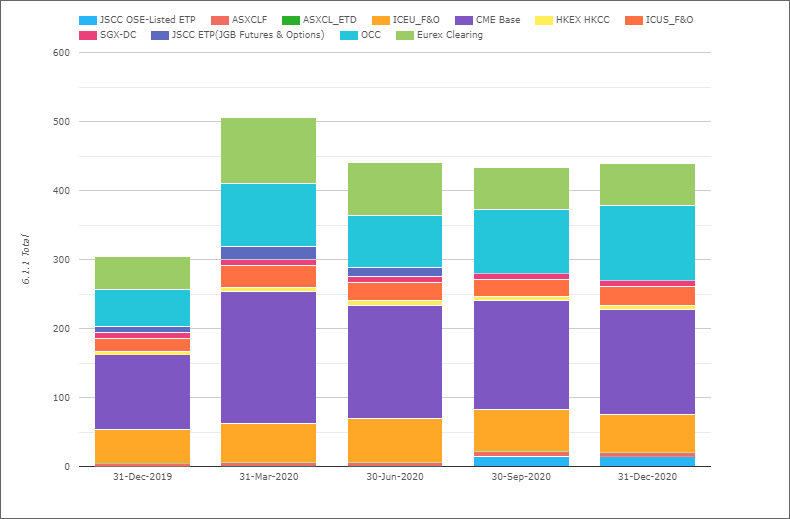

Initial Margin for ETD

- Total IM for these CCPs was $417 billion on 31-Dec-2020

- Flat QoQ, Down 15% from 31-Mar-20 and Up 42% YoY

- (Note the chart shows slightly higher totals as the Eurex Clearing amount in the chart includes OTC IRS IM, which I exclude in my figures here)

- CME Base with $152 billion, down 3% QoQ and up 39% YOY.

- OCC with $109 billion, up 19% QoQ and up 104% YoY.

- ICE Europe F&O with $55 billion, down 9% QoQ and up 16% YOY.

- Eurex with $46 billion, down 2% QoQ and up 21% YOY.

- ICE US F&O $27 billion, up 8% QoQ and up 42% YOY.

- JSCC OSE Listed ETP with $14.3 billion, down 4$ QoQ

- SGX-DC $7.8 billion, down 18% QoQ and up 4% YoY

- ASX CLF $7 billion, up 4% QoQ and up 37% YoY

- HKEX HKCC with $5.8 billion, down 10% QoQ and up 6% YoY

OCC standing out as for the second quarter running it is up by 20% and at $109 billion is higher than the $91 billion reached on 31-Mar-20, with both Client and House IM increasing.

Other Disclosures of Interest

Next let’s do a quick scan of Dec-2020 disclosures highlighting a few with a change tolerance >20% outside the 3 year range of values:

- ASXCLF – 23.1.2 NZ Futures – Interest Rates, Average Notional Value cleared of $11.6 billion is up from $8 billion in the prior quarter

- B3 – 7.3.1 Same day payment, estimated largest same-day and where relevant, intraday and multiday payment obligation that would be caused by the default of a single participant, was $3.6 billion, far higher than the high of $2.4 billion in our history from 31-Mar-2018 onwards

- BME – Repo 6.1.1. Total IM required of $2.1 billion is up from $1.2 billion, while the prior high was $1.7 billion on 29-Mar-2018

- CCIL – Forwards 4.4.3. Peak Day amount in previous 12 months where the estimated largest aggregate stress loss (in excess of initial margin) that would be caused by default of a single participant was $408 million, up from $340 million

- CDCC – 4.1.4 Pre-funded Aggregate Participant Contributions required of C$2.3 billion are up from C$1.4 billion and have been up and down significantly in each of the prior 5 quarters

- CFFEX – China Financial Futures Exchange, 6.1.1 Total IM required of $24.4 billion is up from $19.5 billion, $12.5 billion, $10.4 billion in prior quarters

- CME Base – 6.2.11 Total IM Pre-haircut of Non-Cash Commodities – Gold was $4.2 billion, up from $3.6 billion, $2.6 billion, $1.6 billion and $400 million in prior quarters

- DTCC GSD – 7.3.4 Actual largest intraday and multiday payment obligation of a single participant over the past 12 months, peak day amount was $102 billion, up from $77 billion in the prior quarter and $53 billion 3 years ago. Wow, that is a big number!

- DTCC MBSD – 4.1.4 Pre-funded Aggregate Participant Contributions required of $13 billion are up from $10 billion, $7 billion, $11 billion and $5 billion in prior quarters.

- DTCC NSCC – 6.8.1 Maximum aggregate IM call on any given day over the period was $17.2 billion, far higher than any previous quarter; $8.5 billion in 31-Mar-2020 quarter being the prior high

- EuroCCP NV – 6.5.1.1 Number of times over the past 12 months that margin coverage against any account fell below the actual marked-to-market exposure of the account was 40, up from 34, 30, 28, 4, 5, 5, 6 … in prior quarters. So even after the covid quarter of Mar-20, when there was a large jump, there were further increases in subsequent quarters, which is surprising.

- …..this is the point I realize that I have only got as far as the letter E and there are a lot more CCPs to go, so let’s do the time honored trick and skip to CCPs starting with last letter we have…..

- TAIFEX – Taiwan Futures Exchange, 6.1.1 Client Gross IM required increased to $1.5 billion from $1.2 billion in the prior quarter and $830 million in Dec-2019

- Takasbank of Turkey, BIAS FI, 4.4.10 Actual largest aggregate credit exposure (in excess of initial margin) to any two participants was $1.25 billion, up from $947 million in the prior quarter

The letters from H to S cover a lot of Clearing Houses, but I will leave that to those of you with your own CCPView access.

More Disclosures

CCPView has disclosures from forty Clearing Houses, each with many Clearing Services, so there is a lot more data to look at covering Equities, Bonds, Futures, Options and OTC Derivatives.

With over 200 quantitative data fields and quarterly figures from September 2015 to December 2020, there is a lot of interesting data.

Please contact us if you are interested in CCPView.