At the December 2018 SONIA Working Group, Darrell Duffie (Stanford University), presented a way of compressing existing LIBOR contracts into SONIA contracts. I think it is worth reviewing the suggested methodology.

I also put forward a slight alternative that draws heavily on the work of Duffie. This idea is meant for discussion purposes, so please feel free to comment underneath or get in touch to talk more.

Working Group

It is well worth having a read of the minutes of the December 2018 Working Group on Sterling Risk-Free Reference Rates. The two main topics of conversation were Term Rates (see John’s recent post) and Compression auctions. They also make tantalising reference (well, tantalising to me….) to the upcoming Cross Currency Swap standards for XOIS (OIS vs OIS). However, I do not think these have been made public (yet).

Compression Auctions

Duffie presents a proposal to translate as much of a LIBOR portfolio into SONIA as possible at a point in time auction. It is envisaged that there could be a series of these auctions, and that they would be run by a CCP (or an agent but the focus is on cleared trades for now).

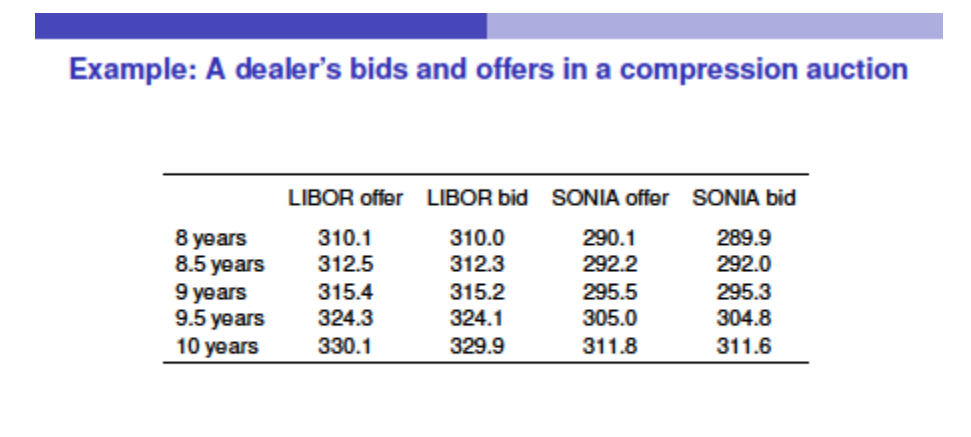

For the auction, market participants would:

- Submit Bids and Offers for LIBOR and SONIA swaps across the whole curve – e.g. 1 year through to 50 years.

- Submit their whole cleared portfolio for potential compression based on these levels.

- The size of the legacy portfolio therefore defines the sizes of the Bid and Offer rates that are viable – hence the idea that this is “Compression” as opposed to true “risky” trading.

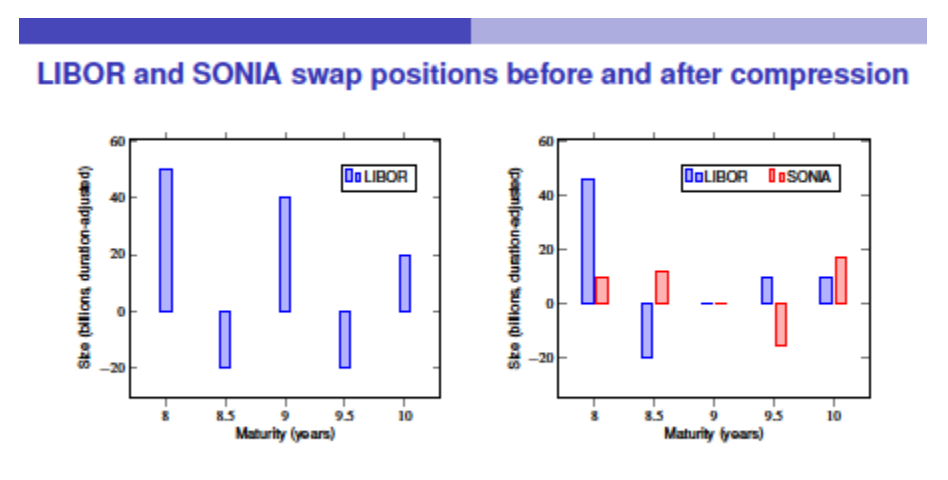

The result of the auction would:

- Allocate LIBOR and SONIA swaps in given maturities where the BID/ASK levels have crossed between two (or more) counterparties.

- Any changes in risk would be subject to individual participants’ risk tolerance in each maturity bucket.

- The size of the trades would be dictated by pre-existing outstanding positions at the clearing house, subject to the defined risk tolerance.

The operator of the auction (e.g. the CCP) would:

- Maximise the amount of LIBOR swaps being ripped up (in gross notional terms) by minimising the resulting outstanding notional of LIBOR swaps after the auction.

- Minimise the total gross notional of LIBOR and SONIA swaps post-auction.

Trying to Keep Everyone Happy

Trying to Keep Everyone Happy

Who would be happy with this auction and what are the risks?

From the off, I should state that I believe this is a good idea and will help the market tackle the potential problem of legacy portfolios. Specifically;

- Dealers, who are used to making markets, will be comfortable with the format.

- Dealers represent the vast majority of outstanding swaps notional (at least one side), therefore it makes sense to ensure this community is well represented in any of the auctions.

- Dealers are comfortable with risky compression, where they do not compress trades with exactly matched dates.

- Anyone uncomfortable with risky compression can impose very strict risk tolerances to ensure they do not have an unwanted change in position.

The downsides are small in comparison:

- Most market participants would be uncomfortable sending in “two-way” quotes. However, the design looks to be flexible enough that they could just send in the side of the price they want to trade on.

- Counterparties are not all filled at the same rate.

- Counterparties do not know the price of their trades (particularly if submitting two-way prices) until after the auction.

Is There a Better Way?

Drawing heavily on the ideas presented, I do wonder if it would be beneficial to set the auction prices before the event. This is common in FRA volume matching runs, where the whole market knows the levels that they will trade at before they submit their volumes. It would then be a simple case of either:

- Submitting your whole cleared portfolio versus the counterparties in the auction to define your volumes or;

- Specifying the volumes that you want to trade versus the defined market levels.

Typically, market participants should want to specify the volumes when the market levels are known beforehand. This may be due to risk management reasons – e.g. they have an offsetting uncleared position – or maybe because they feel the curve calibration of the auction levels is different to their own.

FRAs vs OIS

To provide a “perfect” hedge for legacy LIBOR swaps, the following could be performed:

- Project all LIBOR fixings per date until the end of a portfolio for each LIBOR tenor per currency (i.e. LIBOR 1m, LIBOR 3m, LIBOR 6m etc).

- Transact an offsetting FRA (or single period swap) versus that fixing risk for every single date.

- Transact an equal and opposite OIS (single period) that starts on the fixing date.

The FRA and the OIS are transacted at market-levels, which therefore defines the size of the LIBOR-OIS spread at each date in the future.

This mechanism is a much more precise methodology than a bulk compression auction, which groups risk into e.g. six month buckets.

FRA vs OIS Auction

Could the market ever be in a position whereby these “perfect” hedges could be executed en masse? Let’s consider cleared positions:

- The CCP knows the fixings of all members for all dates in the future. They probably already provide this information via their in-depth daily reporting.

- The CCP provides end of day marks for both LIBOR and RFR swaps.

- The CCP could therefore define the input levels to the auction as their “closing curves”.

- These could be sent T minus one to key market participants (both buyside and sellside) to garner consensus on their accuracy.

- A volume matching auction can be conducted on date T to transact FRA vs OIS hedges for all interested parties.

- The CCP can automatically net and compress all resulting FRAs versus Swap fixings to ensure that gross notional is compressed post-auction.

This methodology could be particularly effective once we know the precise calibration criteria for the ISDA fallback.

It may be easier from an infrastructure perspective as it would look and feel like existing processes, and market participants would just have to consume new swaps into their existing systems. This sounds easier to me than going through an ISDA protocol and changing the projection of risk on legacy LIBOR swaps onto RFR curves.

Remember that in a SACCR world, leverage ratio is governed by net notional to the CCP, not gross. Therefore the multiple OIS single period swaps that would be traded do not have a negative impact on bank capital requirements.

In Summary

I’ve now seen the Darrell Duffie presentation given to both the Swiss RFR group and the UK RFR group. It is undoubtedly a good idea.

We present a potential modification to the design to enable less risky compression, and with added price transparency. It is just food for thought at the moment, but these ideas may gain more traction as the demise of LIBOR becomes ever more likely.

“The FRA and the OIS are transacted at market-levels, which therefore defines the size of the LIBOR-OIS spread at each date in the future.”

How is this defined? Each dealer probably has its own view on that spread for each date, depending on models and interpolations etc… chances are this daily fixing “market” is not uniquely defined, right?

Thanks for the comment, and you are quite right that the forward estimation of the levels is not uniquely defined. Fortunately, most pricing models are now standardised in the market, so I believe that we could efficiently find an equilibrium price, much as we see in FRA matching services today.