FX Options Trading On SEFs

In this article I will look at FX Options trade volumes as reported to US Swap Data Repositories and volumes published by US Swap Execution Facilities. This analysis highlights the following: Vanilla FX Option volume averages 24,000 trades a month in the largest 10 currency pairs EUR/USD is the most active pair with up to […]

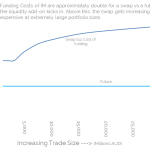

AUD swap market: Concentration risks from the Clearing Mandate

We present a uniquely Clarus view of the AUD IRS markets Our analysis of the regulatory landscape, bond issuance data and swap market flows suggests that many Swap Dealers will end-up in Add-On territory for OTC swaps clearing at CCPs This means that swaps become incrementally ever more expensive to trade relative to futures From a liquidity point of view, […]

TriOptima Compression at CME

CME recently put out a press release on their first TriOptima multi-lateral compression cycle, stating $2.2 trillion in gross notional reductions with 44,933 line items removed. (The full press release is here). So I thought it would be interesting to look at the significance of this. CME IRS Open Interest Using CCPView, we can look at CME […]

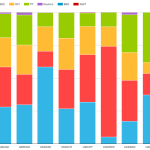

SEFs in Japan: ETP Data

Japan has joined the SEF party with their own flavor of trading venues known as Electronic Trading Platforms (ETP’s). ETP’s launched last week on Tuesday, September 1st. Amir had written about them back in April. Some rules have since been tweaked, and of course we now have some data. Lets have a look at everything. […]

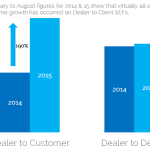

Is an All-to-All SEF Market about to arrive?

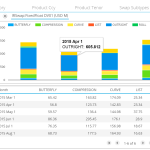

We combine SEFView and SDRView to strip out Compression flows from D2C SEFs. This allows us to make interesting comparisons between the Dealer to Client (D2C) and Dealer to Dealer (D2D) markets. D2D USD volumes have stagnated year-on-year. D2C volumes have exploded higher by 190%. This is before we even start talking about EUR swaps…. […]

Webinar on MAC Swaps & Swap Futures

Please join us and CME on Wednesday, September 9th at 11:00am EST, for a discussion and Q&A on MAC swaps and swap futures. Registration here.

China’s Black Monday and Volatility of Swap Margin

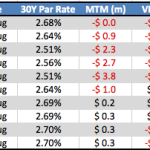

We all know that the Shanghai Composite Index has seen massive volatility with the media dubbing August 24th as China’s Black Monday with the Index falling 8.5% and then a further 7.6% on the 25th. So I thought it would be interesting to look at how a USD Interest Rate Swap trade performed over this […]

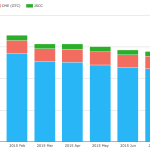

August 2015 Review – What Summer lull?

Our loyal readers know the form by now, so let’s kick straight into our monthly review of all things Swap and SEF-related. The highlights: American markets successfully fought off the Summer lull, aided and abetted by significant volatility in the second half of August. SEF Volumes were 50% higher than last August in USD swaps. […]

Swap Default Funds at the CME & LCH

CME this week changed their minimum contribution to the default fund. My initial reaction was that this change was designed to encourage smaller firms to self-clear their IRS business. It got me investigating default funds and the entire financial safeguards at CME and LCH in more detail. Default Waterfall After reading through the CME rule […]

Post-Trade Transparency in CDS Index

The recent IOSCO report on Post-Trade Transparency in the Credit Default Swap Market, certainly makes interesting reading and in this blog I will provide a short summary of the report as well as looking in more depth at the data now available for CDS Index. IOSCO Report The report focus is on regulatory systems that mandate disclosure of […]