Impact Of March 1st VM Regime

The big VM deadline has come and passed. Did trading grind to a halt? Prior to the date, based primarily upon what I had read in news articles, I would summarize my sentiment around the VM implementation as: The industry had not gotten through even half of the required new paperwork Large asset managers being […]

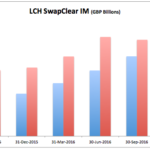

Initial Margin Optimization

Summary: Initial Margin requirements for OTC Derivatives are large and increasing at CCPs IM Optimization is a periodic or trade by trade analysis that seeks to reduce overall IM Clearing members can achieve significant cost and capital benefits Similar techniques can be extended to UMR and ISDA SIMM Client IM is growing much more rapidly than […]

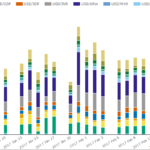

Exploring Energy Swaps On The SDR

Back in August, I had a look at the wealth of commodity data on the US Swap Data Repositories. The general takeaways were: There’s lots of data Much of it is murky. Describing many OTC commodity trades require lots of details that are missing. Case in point, we found the second most active commodity to […]

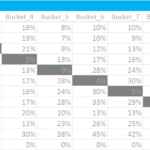

ISDA SIMM™ in Excel – Equity Options

We build an IM calculator in Excel for Equity Options under ISDA SIMM™. The methodology builds on the margin methodology for Swaptions, and uses very similar formulae. We cover all forms of IM. This blog is for the Vega and Curvature Margin. There are subtle differences to the implementation for Rates. UPDATE: We now offer free […]