Free Trials, Analytics, Data and More

We now offer self-registered free trials for a number of new products. This is something we have always done for our Data products. A pre-requisite is that a product has to be so well designed that a user can access and starting using, without having to read a user guide and he/she can use with […]

FX NDF Package Transactions

Today, I looked at packages of FX NDF trades on the SDR, expecting to be able to find some basic packages, or even just logical groupings of trades such as: FX NDF Swaps. These would have a near & far leg, and the price differs by some forward points. Par Forwards. These are a structure […]

VM Big Bang – Impact on FX Markets

The six month reprieve from UMRs expired 1st September. We look at trading in uncleared markets in the past six months to see if anything changed. The number of uncleared IRS trades has shrunk by 50% as the regulations took hold. Products with no cleared alternatives continue to trade bilaterally. Volumes have continued to be […]

Swaps Data Review: Credit Derivative volumes

My Monthly Swaps Data Review for Risk Magazine was published on Friday. This looks at volumes of Credit Derivatives in the 4-month period to July 2017, showing: Global Cleared Volumes CDS Index represents 86% and CDS 14% of volume ICE Clear Credit is the largest CCP with 75% of the volume iTraxx Europe is the […]

MIFID II Transparency will leave us in the dark

We run the SSTI and LIS thresholds over US SDR data. We anticipate that over 80% of EUR swaps will not be subject to pre-trade transparency. Post-trade transparency will not be much better. 75% of the risk traded will remain dark for up to four weeks. We are intrigued to see what the APAs will […]

FRTB Non-Modellable Risk Factor Analysis

The FRTB Internal Model Approach requires risk factors to be checked for modellability Non-modellable risk factors are then subject to stressed capital add-ons Modellable and non-modellable is determined by applying a specific test Clarus has the Data and Analytics to perform such a test We make this available in our FRTB for Excel product Making […]

APRA – Margining for non-centrally cleared derivatives

It is almost two years since I wrote about the Final US Rules on Margin for Non-Cleared Swaps. How time flies and since then we have seen implementation of this rule in the US and equivalent rules and regulations in many other jurisdictions. Today I will look at the Australian regulation recently made final by […]

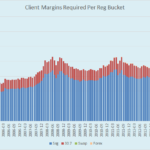

FCM Rankings & Concentration: Q2 2017

We have Q2 data for Clearing Brokers, showing any changes in the US clearing landscape. Let’s dig into the data, starting with our count of FCMs by various metrics: Showing 63 firms registered (down 1 from Q1 2017), and 56 firms with any Client Requirements. Other headline metric is total client required margins, which trended […]

Curve Trading in USD Swaps

Curve trades account for around 10% of volumes reported to US SDRs. We identify these package trades by matching timestamps and risk equivalence of the two legs. Benchmark curve switches trade every single day in decent size. We look at the USD Curve Trade market during 2017. Curve Trading Call them Curve Trades, Spreads or […]

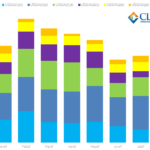

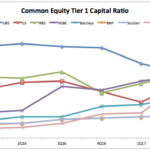

Capital and RWA for European Banks

Following on from my recent Capital Ratios and Risk Weighted Assets for Tier 1 US Banks article I wanted to look at the equivalent metrics from European Banks. Background One of the lessons learned from the Great Financial Crisis was that Banks were generally under capitalised commensurate to their risk exposure, leading to new Basel III regulations […]