MAC Swap Trading

Tod last took a look at MAC swaps in 2016. Has anything changed since? (Spoiler: not much!). But there is certainly some activity over at ERIS. What are MAC Swaps? A brief reminder that a MAC swap is a particular flavour of forward starting interest rate swap, starting on an IMM date (third Wednesday of […]

Our Response to the ESMA Trading Obligation Consultation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. As we stated back in June, we have concerns about the quality of the data used to determine the Trading Obligation. We have therefore offered to make all of our SDR data available to ESMA as part of our response to the […]

Array Formulas in Excel

We explain how to work with Array Formulas in Excel. Master the Three Finger Salute CTRL+SHIFT+ENTER. CTRL+/ is an amazingly effective shortcut. It is always easier to expand an array than shrink it. Consistent formatting provides an obvious visual cue when working with arrays. SIMM for Excel SIMM for Excel is an add-in that performs […]

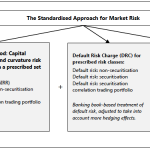

FRTB – Simplified Standardised Approach

The BCBS recently published a Consultative document on a ‘Simplified alternative to the standardised approach to market risk capital requirements” and in this article I will look at the detail of this. Standardised Approach (SA) BIS provides the following diagram to summarise the Standardised Approach. (For a re-cap of the SA see FRTB – What […]

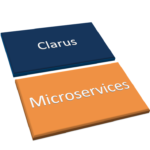

ISDA SIMM™ IN PYTHON

The Clarus Microservices API makes it very easy to compute ISDA SIMM™ from Python The input data required is a CRIF file contain risk sensitivities What-if trades can be easily added to determine the incremental change in margin We provide a Sandbox within our API Reference page for you to try the API methods Before moving […]

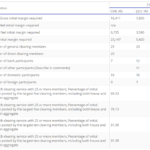

CCP Disclosures: How much does it cost to run a trading business?

The latest batch of CPMI-IOSCO CCP disclosures are out for Q1 2017. We look at Initial Margin across Rates and FX. The Top 10 banks post $14bn across three CCPs. This gives us an insight into the cost of funding a trading business. The split of IM illustrates the intrinsic cost of CCP basis. Initial […]

Swaps Data Review: CCP and SEF Volumes

My Monthly Swaps Data Review for Risk Magazine was published on Friday. This looks at volumes of G4 Swaps in the first six months of 2017, showing: Strong growth at LCH and JSCC OIS volumes significant in USD, EUR and GBP JSCC volumes in JPY Swaps exceeding LCH in 2017 SEF volumes show D2C continuing […]

CCP Disclosures 1Q 2017 – What the Data Shows

Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures and in this article I will highlight what the data shows, similar to my article on 4Q 2016 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more […]

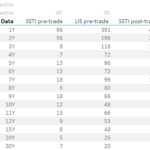

MIFID II: What Should Transparency Look Like?

We replicate the transparency calculations published by ESMA, using SDR data on EUR Swaps. EUR swaps are the second largest IRS market, and yet do not benefit from real-time trade level reporting. Our data shows that most of the EUR IRS curve is “liquid”, with ADV >€50m. SDR data calibrates realistic pre-trade transparency thresholds at €50k […]

ISDA SIMM For Excel

SIMM for Excel performs ISDA SIMM™ Initial Margin calculations from Excel. Free 14-day trials are available for all financial firms. Reconcile ISDA SIMM calculations. Perform pre-trade analysis of your bilateral trades quickly, simply, reliably. The functions calculate Initial Margin across a whole portfolio. Users can also create CRIF sensitivities from trade-level details. Functions That Won’t Kill Excel Our […]