- The latest batch of CPMI-IOSCO CCP disclosures are out for Q1 2017.

- We look at Initial Margin across Rates and FX.

- The Top 10 banks post $14bn across three CCPs.

- This gives us an insight into the cost of funding a trading business.

- The split of IM illustrates the intrinsic cost of CCP basis.

Initial Margin Data

Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more are published each quarter with a quarterly lag.

CCPView now has seven sets of disclosures, from 30 September 2015 to 31 March 2017.

I cannot pretend to be an expert on all 200 fields, but anything with “Initial Margin” in the title piques my interest. I tend to find that looking at this data in isolation is not as productive as when we use some context. When put alongside our volume data from CCPView (and SDRView), the value in these new data sources becomes apparent.

Costs of Doing Business

How much does it cost to run a Top 5 Rates trading business? That seems like a question that regulators, incumbents, new entrants and the buyside would really like to know the answer to. I can’t give you a complete answer, but we can put a figure on a portion of it.

So let’s look at the black-hole of costs that can be associated with a trading business. One such black-hole is the cost of funding my Initial Margin each year at a CCP. Regardless of whether I accurately calculate MVA on each trade, I (probably) cannot monetise that amount each year. So let’s treat it as an operational overhead for the purposes of this blog, akin to salaries, IT and compliance costs.

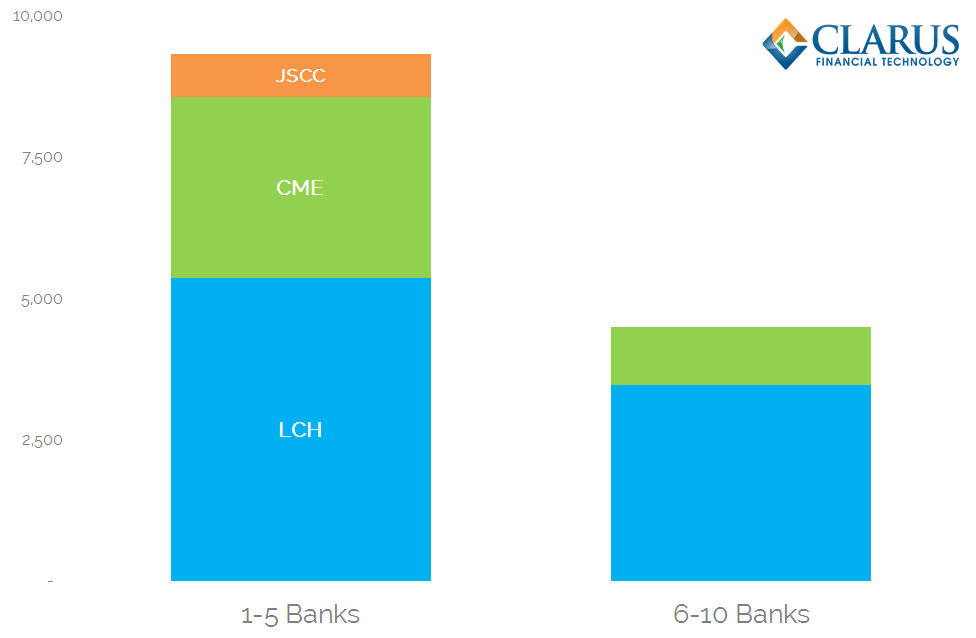

A Top 5 Bank Posts $10bn in Initial Margin

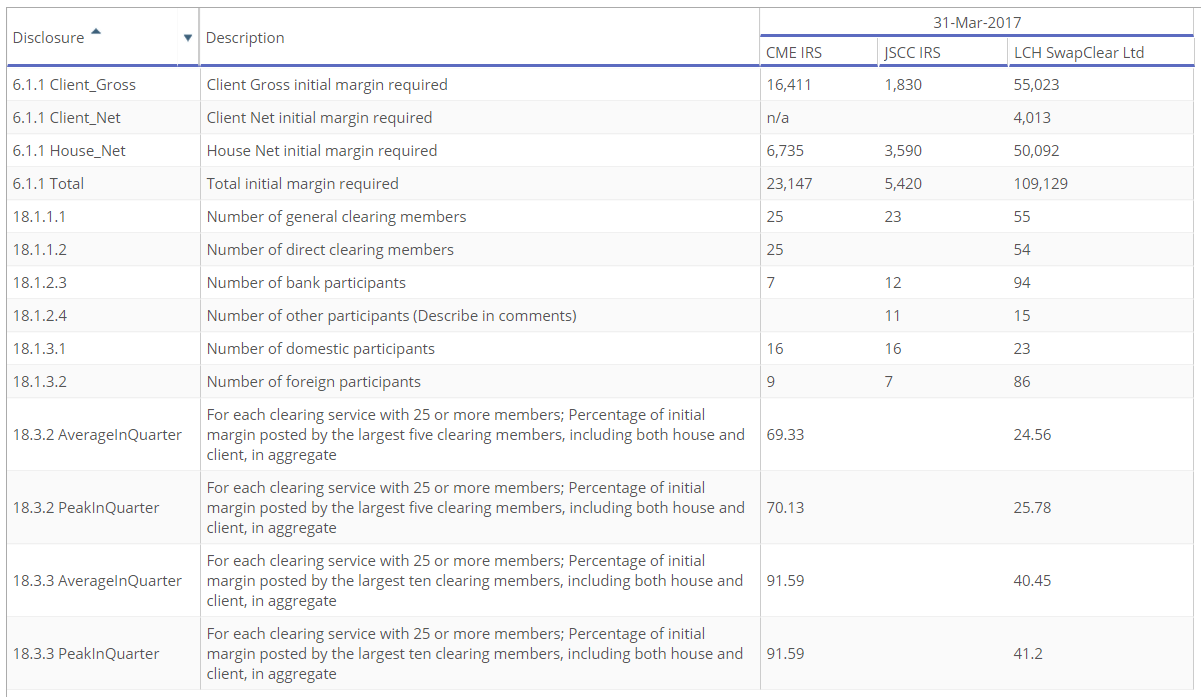

The areas of interest all fit on a single query in CCPView. Have a look at the following data;

Showing;

- Total IM required across CME, JSCC and LCH was $23bn, $5.4bn and $109bn respectively.

- Let’s call it $138bn in funding needs across the industry.

- At LCH, the $109bn is split across 109 Clearing Members. This covers both House and Client clearing, where we can now see there are fewer direct clearing members (54) than those “general” clearing members, by which I assume the disclosure means counterparties accessing clearing via an FCM.

- At LCH, Client margin is now 10% higher than House margin ($55bn versus $50bn).

- At CME, the $23bn in IM must be funded across 50 members, evenly split between house and client clearers.

- Consistent with conventional wisdom, client IM at CME is much higher than dealer IM ($16bn vs $7bn).

- The relatively small amount of $5.4bn of IM required at JSCC is split amongst 23 market participants, 12 of whom are banks, and only 7 are foreign institutions.

We could get some of this information from previous disclosures at the CCPs and by diligently recording who was a member. But it is the following fields that I find particularly interesting:

- The largest 5 Clearing Members at LCH post 25% of the initial margin.

- The next 5 largest Clearing Members post 15% of the initial margin.

- At CME, it is much more concentrated. The 5 largest Clearing Members post 70% of IM.

- The next 5 largest Clearing Members only post 21% of the margin.

Roughly speaking therefore:

- A top 5 swaps bank has to post nearly $10bn in Initial Margin across 3 CCPs. This is across both House and Client business.

- Of this, 57% would be posted at LCH.

- 35% is at CME.

- The remaining 8% is at JSCC.

- Remember this is across all currencies and all “IRS” products. This is in stark contrast to the relative market shares by volume.

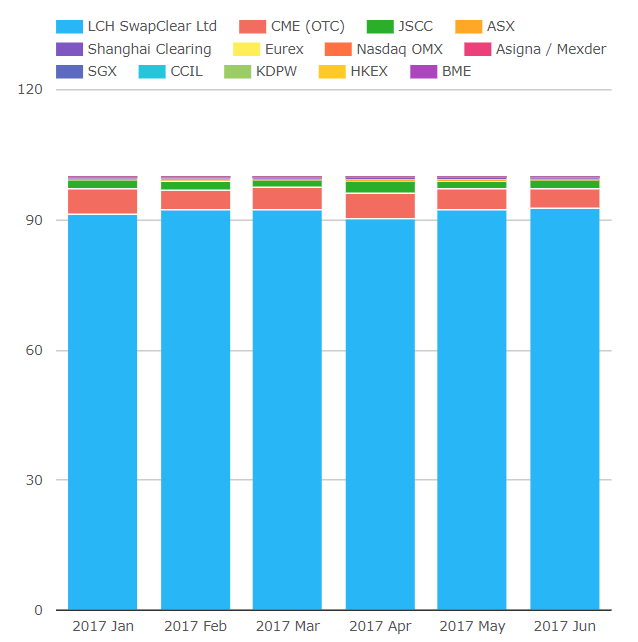

Below shows how dominant LCH is in terms of volumes traded:

- LCH has had a ~92% share of volumes traded every month this year.

- We could safely assume that as a top 5 bank, you also transact over 90% of your cleared volumes at LCH.

- And yet, LCH do not consume over 90% of your margin requirements according to the disclosures. They account for only 57%.

These IM disclosures hence shed a light on how large the costs of splitting a book across multiple clearing locations can be. Multilateral netting really does rule! Hence the prevalence of CCP Basis costs, as Tod recently highlighted.

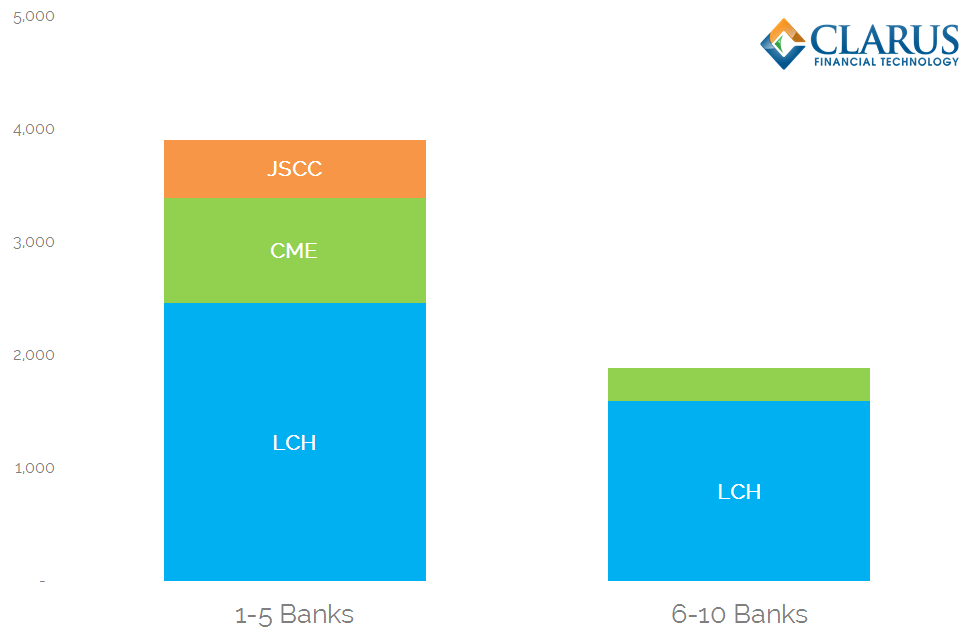

It Costs $20m A Year to Fund IM

As a Top 5 bank, I must post nearly $10bn in IM. But remember that this is split across both Client and House business. In theory, Clients should be giving me the IM related to their clearing business (maybe plus a spread), therefore I should only be concerned about funding my house business.

Let’s assume that it is the same top 5 banks who account for both Total IM requirements and House IM requirements.

Across the industry as a whole, 44% of total Initial Margin requirements are due to House business. So we could expect to fund around $4bn to run our swaps business. How is this split across clearing houses?

Showing;

- As a Top 5 liquidity provider across swaps, I will need access to nearly $4bn in Initial Margin.

- 63% of this will go to LCH.

- 24% to CME.

- How much will that cost me? If I assume a cost of funds at OIS plus 50 basis points (which seems pretty cheap to me?), it’s going to be a drag on my PnL of about $20m each year.

- Is it any rosier at Banks 6-10? My costs are about half of that, but then I expect to trade less than half of the volume that a Top 5 bank would.

- Is it easier to recoup double the costs on double the volume?

- It would help if all of your business was done at a single Clearing House….

It is a shame we can’t take this analysis any further. It would be great to look at the ETD space and the benefits of cross margining – something CME have offered for a very long time. But I am not sure I am comfortable in assuming that the same Top 5 consumers of IRS IM are the same counterparties as the Top 5 consumers of ETD IM? Happy to hear from anyone who thinks otherwise….?

Finally – FX Clearing

I keep a close eye on NDF clearing, and the disclosures have cast a bit more transparency on the workings of LCH’s ForexClear;

![]()

Showing;

- Initial Margin has increased significantly since the previous disclosure. Up from $3bn to $5.6bn.

- There are now 26 Clearing Members.

- ForexClear do not currently split out volumes by House vs Client clearing. It looks like there are now two non-bank members.

- And whilst there are 16 direct members, there are 10 accessing clearing via an FCM.

- In terms of margin, 55% is posted by the top 5. A further 30% of IM is posted by the next 5 largest members.

- Hence, to fund a top 5 liquidity provider at ForexClear requires “only” $622m.

- The cost of this? About $3.1m at 50bp over OIS. And that assumes we fund it for a whole year, where-as most NDF positions are expected to roll off within a month.

- Perhaps CCP Basis in NDFs will never appear in this case….? Discuss….

In Summary

- As a Top 5 liquidity provider in swaps, we estimate you will be posting around $10bn in Initial Margin across the 3 largest CCPs.

- $4bn of this will be down to house positions.

- The cost of funding this for a year (at 50 basis points over OIS) is about $20m.

- As a Top 10 liquidity provider, your costs would halve. But we would also expect you to attract only half of the volume.

- In FX, you would only need to fund about $600m a year as a top 5 liquidity provider. But bear in mind that clearing has a long way to go in FX until 90+% of market volumes are being cleared.

- For a fair comparison, we also need to know how much IM dealers are posting under ISDA SIMM calculations. Then we can fairly calculate the costs of bilateral versus cleared products at a business level.