- Managing FRAs and Libor fixings on Swaps is complex.

- Short-end traders must balance their exposure between the Stub and STIR futures.

- Stub risk decays with time and changes with LIBOR fixings each day.

- It must therefore be carefully managed around event risks such as Central Bank meetings.

- IMM roll dates also result in PnL volatility and large changes in risk as a result.

FRAs

What is a Floating Rate Agreement?

A FRA is a contract for difference against, typically, a LIBOR fixing. They normally cash-settle on the fixing date. It’s great for speculative purposes, but is a very difficult product to risk manage outside of a one-for-one hedge.

FRAs Trade. A lot.

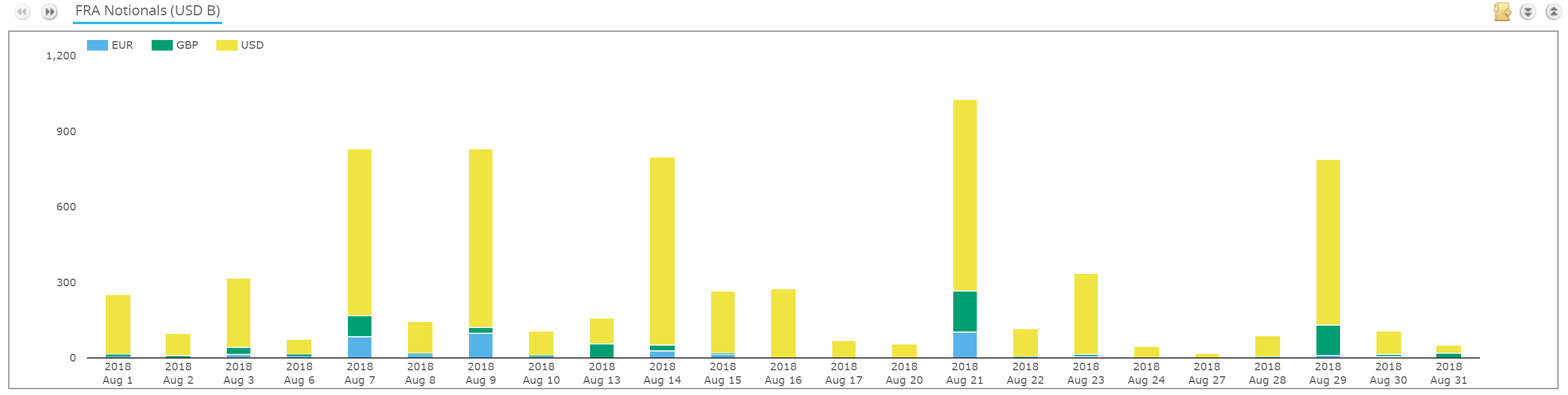

Look at any volumes reported to SDRs or SEFs and you will see a huge volume of FRAs trading. Look at the past month – historically August is a “quiet” month:

Showing:

- $6.9 trillion has traded!

- Nearly $6trn of this was in USD.

- And this is just the notional reported to SDRs. In CCPView, we see $11.3trn cleared globally.

$11trn of 3 month FRAs is equivalent to ~$500bn of 5 year swaps. For reference, $2.5trn was reported to SDRs in USD IRS during August.

So why do FRAs trade so much? Read on to find out.

FRAs Are An Exotic Product

Say What?!

In theory, a FRA is the simplest product that we trade as Interest Rate Derivatives traders. They give us a single period of fixed rate risk until the moment that they expire. It is the point that they expire that they cause us problems.

The expiry of a FRA (and a LIBOR fixing on a swap), in terms of risk management, looks and feels like an auto-exercised option expiry that always expires at-the-money. On a FRA expiry, a swaps trader experiences a change in delta. Until the LIBOR fixings come out, I don’t know what rate my delta has changed at. Nasty, right?

So What Happens at Expiry?

Most swaps traders will look at their “ladder” of fixings on their portfolios. If I have a FRA fixing today and an offsetting fixing tomorrow, I will typically do nothing. Unless there is an event risk in-between (e.g. a central bank meeting). Any difference in the LIBOR fixings will end up being reflected in my PnL as “carry” – the time-decay on my (linear) book.

However, if I have another fixing that is going to add to this FRA expiry, I might want to “hedge” this risk on my book. How would I do that at expiry of the FRA? The only instrument I readily have available is a Short Term Interest Rate future (STIR).

Therefore, when LIBORS are published around 11:30am London, you will typically see a flurry of activity in STIR futures. Yes, some of this can be in reaction to the LIBOR fixings themselves, but mostly this increased volume is due to swaps traders hedging their FRA fixings.

STIRs are a terrible hedge

IMM dated futures don’t really act as a great hedge. We measure the hedge-efficacy of a STIR contract in a simple way – linear interpolation.

The more days that a FRA contract shares with an IMM contract, the higher the correlation should be between where a FRA fixes and where the IMM is trading. Yes, this can be flawed, but it is important to note that it works even if you assume overnight rates only move in discrete 25 basis point increments (e.g. lock-step with central bank policy moves).

For example – a 3 month FRA fixing on 4th September 2018 shares 86% of its’ exposure to overnight rates with the Sep18 STIR that fixes on 13th September 2018. It’s therefore a pretty good hedge.

However, a 3 month FRA fixing on 25th September 2018 shares just 9% of its’ exposure to overnight rates with the Dec18 STIR. It’s therefore a terrible hedge, and that causes a problem because there’s an FOMC meeting on the 26th September. I probably don’t want my delta risk to jump on the 25th September, one day before the Fed announces their latest rate decision!

The Dreaded Stub Risk

What all this means is that I end-up splitting FRAs into their hedgeable and “non-hedgeable” components. For the FRA fixing on 25th September:

What all this means is that I end-up splitting FRAs into their hedgeable and “non-hedgeable” components. For the FRA fixing on 25th September:

- I can hedge 9% of the delta with the Dec18 STIR. Bear in mind that the FRA covered by this STIR covers Fed meeting dates outside of the expiring FRA – namely the Jan meeting in 2019. So it is prudent to only trade a small amount of this future, in case it moves for reasons not associated to my 25th Sep – 25th Dec FRA period.

- I am left with 91% of my risk “un-hedged”. This is what we call the “Stub” risk. It is the period of days that is not covered by a (now expired) Sep18 STIR and the subsequent Dec18 STIR.

Most interest rate curves will assume that futures take precedence over cash – so whilst we may have overlapping instruments at the short-end of our curve (e.g. the FRA fixing today versus the IMM dated FRA or future), it will be the IMM dated contract that will form a node, not the end date of the FRA. Our overnight curve therefore almost always has an implied jump in rates on the IMM date.

This causes PnL volatility.

If I have a known date, where I know there will be PnL volatility, it is prudent to try to minimise my risk associated with that volatility. Traders therefore actively manage this so-called “Stub” risk – the portion of their short-end delta that falls on dates short of the first IMM date.

How to manage Stub Risk?

There is one good thing about Stub Risk. Because FRAs (and fixings on swaps) act like auto-exercised at-the-money options, their delta change is predictable. And the IMM dates don’t change, so we know what portion of any FRA-delta we can attribute to the Stub portion, and which to the next IMM (the same applies for 1 month and 6 month fixings).

We therefore need to predict our delta ladders in the future.

Time Decay + Expired FRAs = New Risk

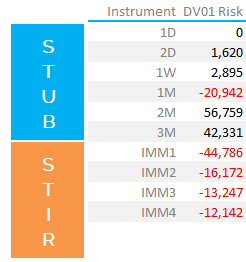

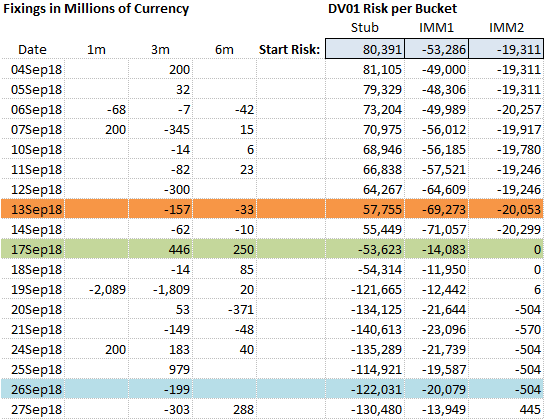

It is instructive to look at a real swaps book. Consider the following portfolio:

Showing;

- The date of each fixing (1st column).

- The notional value of each fixing I have in 1 month, 3 month and 6 month tenors (columns 2 to 4).

- My projected DV01 risk on each date in the future (columns 6, 7 and 8).

- The next ECB meeting date, on 13th Sep, is highlighted in Orange as a potential event risk.

- The next IMM expiry date, the 17th Sep, is highlighted in Green.

- The next Fed meeting date, on 26th Sep is highlighted in Blue and is a key event risk for this portfolio.

For each date in the future, I can see my DV01 risk in each bucket (Stub, IMM1 and IMM2). In the industry parlance:

- I am long futures. I have a “received” Rates position. If Rates go down I make money. The same as being long bonds.

- I am “short the stub”. If Rates go up (or go up faster than the market expects) I make money.

Rate Hikes = Short Stub

With the Fed hiking rates, it is generally beneficial to be “short the stub”. This means that as the fixings come in higher every day, your natural paid position in the Stub will make money.

In the portfolio above, I have a problem. My short Stub position will reverse at the IMM date, which is before the next Fed meeting. Unless I expect a dovish meeting – so dovish that it will move spot LIBORs – I will want to do something about this. What?

Trading FRAs

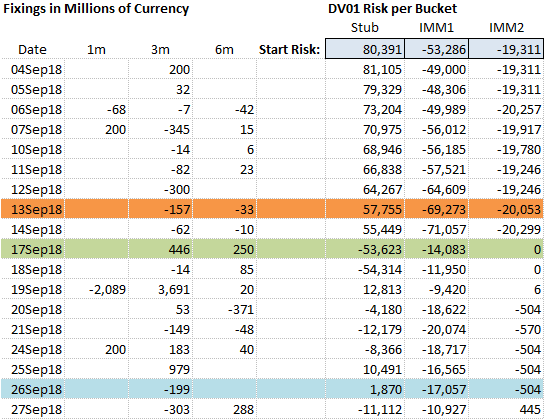

I need to sell some FRAs! And I need to sell some FRAs expiring before 26th Sep. My risk changes the most between the 17th and 20th Sep, so I should be actively trying to sell these FRAs. How?

As a market participant I can do two things – try to get an outright bid on the FRA, or enter a FRA Auction.

FRA Auctions

FRA auctions – run by NEX Reset and TP Match (part of TP-ICAP) – offer buyers and sellers the chance to volume match their different FRA dates at mid-market. So, assuming that I am happy with the mid-market curve published by Nex or ICAP, I can sell a FRA dated 21st Sep, and buy back a different date in the future (let’s say closer to the Dec IMM date).

This means that my portfolio has no change in net delta, but I can change my Stub position before the Fed meeting by altering my fixings ladder. Ideally, I could sell $5.5bn of the “0s3s 21st”. In which case, my position would look like:

- Phew. I’m now as close to neutral as possible on Fed day in the stub (my stub position is just +$1,870 per basis point).

- I can manage the residual risk in the IMM1 bucket as I see fit – probably by selling Dec futures.

FRA Complexity drives Volumes

You should now have a good idea why these FRA auctions are so successful. Managing LIBOR fixings is far from straight forward! Swaps dealers have a constantly changing delta profile at the short-end of the curve, and it consists of a largely unhedgeable Stub portion versus liquid futures. There is an inherent requirement to continuously shuffle this risk as fixings result in a change in delta.

And if LIBOR goes away?

I cannot do a blog these days without mentioning new overnight RFRs and Libor reform!

RFRs offer both good news and bad news for Stub risk management:

- Good news: OIS fixings happen everyday, therefore whilst we still have a fixings ladder, our exposure each day is much much lower. Probably low enough to only hedge once in a while.

- Bad news: Residual LIBOR books will continue to have these big swings in Stub risk – unless perfectly hedged. From the ISDA fall-backs, I think only a compounding in-arrears approach will get rid of this.

Automation and Optimisation via CHARM

If I can blog on it, then we can build it!

Our CHARM risk engine is designed to make your risk transparent, understandable and actionable.

Whether it is auto-hedging fixings day-to-day within defined DV01 parameters, or structuring the portfolio to have particular stub exposures before and after event dates – our software is designed to support and enhance that decision-making process.

Ask us for a CHARM demo today.