- June sees $295bn of 3 month USD funds provided by central banks expiring.

- With the Bank of Japan accounting for 50% of the outstanding amounts of these facilities, USDJPY cross currency basis (and FX) will be a focus for these maturing funds.

- The price differential between the central bank facilities and market-based pricing has shrunk from 200 basis points to a little over 20 basis points now.

- Will banks choose to roll their USD funds with the central banks?

FX Swap Rollover

The mechanics of an FX swap rollover may be thought of as:

- At maturity of an existing FX contract, participants will need to physically deliver (or take delivery of) a foreign currency, typically in exchange for USD.

- Rather than taking delivery, a new FX contract can be entered into, which starts on the day of the maturing contract and matures at a later date in the future.

- In effect, the delivery date of the original contract has been amended to a later point in time.

We have a huge rollover approaching – of nearly $300bn in the markets. This is the amount of central bank FX/liquidity swaps that mature in June 2020 from the original market stresses in March. What will happen to these USD amounts – will they be rolled over?

Dollar Dominance

The FT article below prompted me to revisit the data on the use of Central Bank FX swaps:

Never one to shy away from highlighting the importance of Cross Currency swaps, I loved the following paragraph:

When future financial historians study the Covid-19 shock, they will conclude that the Fed’s intervention in offshore dollar markets via swaps deals with other central banks was one of its most significant policy moves. Not only has the Fed’s action calmed markets, it has shored up the hegemony of the dollar-based global financial system for years to come.

FT.com Fed’s swaps preserve dollar’s reach

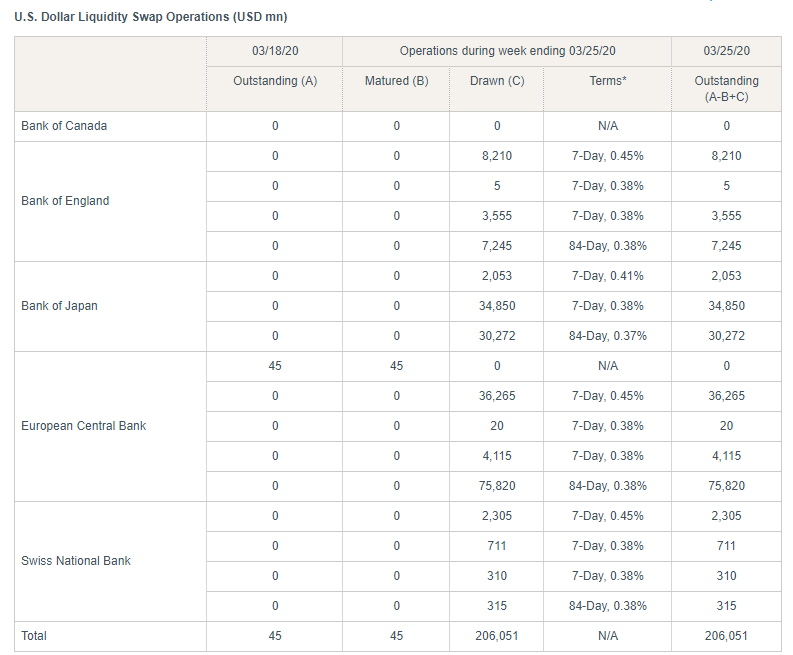

It seems we would be well served to keep an eye on the utilisation of these swap facilities. Recall that they were first used, in context of the COVID-19 shock, on March 18th.

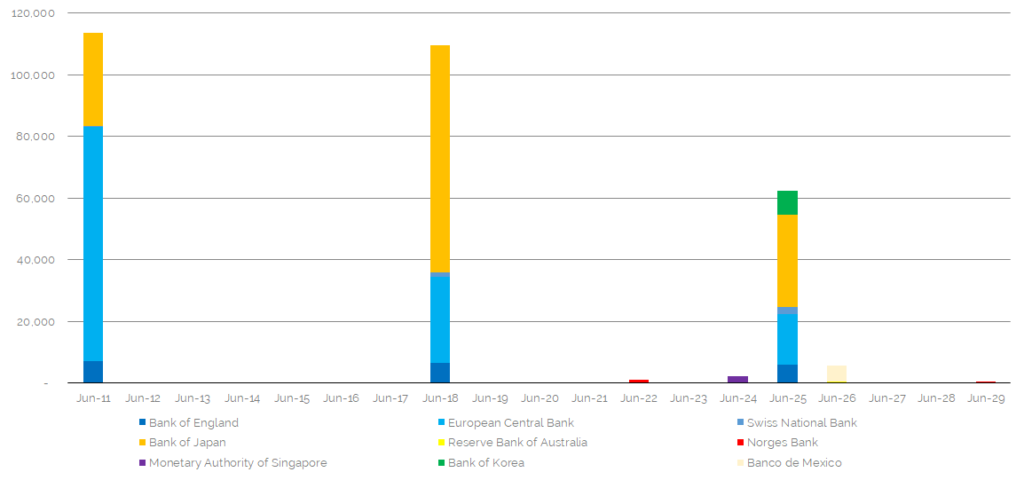

Looking at the Fed website, that means we have around $114bn maturing of the original three month loans (84 days) on 11th June 2020:

Mechanics of Central Bank FX Swaps

To find out more about the details of the swaps themselves and how they work from an operational perspective, please check out previous blogs on the subject:

Utilisation Data

For today’s blog, I am interested to analyse whether these USD funds will be rolled during June – or will they be left to simply expire?

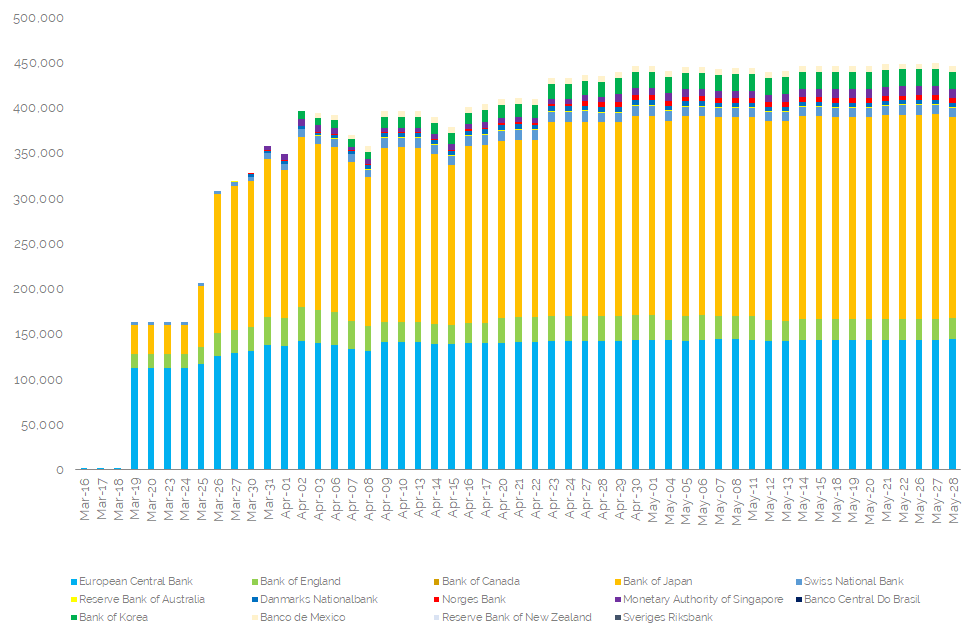

To get an idea, let’s look at the use of the facilities as they stand today. The total Notional Outstanding of all USD swaps (both 7 day and 84 day operations) now stands at $446bn. This is up from $397bn when we last wrote about it on 14th April. So the uptake has slowed considerably, with only $50bn taken in the past six weeks.

Looking at the allocations, as the FT highlighted, Japan is by far the largest user of these swaps:

Showing;

- Bank of Japan has a notional outstanding of $222bn, just slightly shy of the highs of $226bn.

- The Bank of Japan therefore accounts for 50% of the notional outstanding across all USD central bank FX swaps.

- Next up is the ECB, with €145bn outstanding (as high as it has ever been), accounting for 32% of notional.

- The Bank of England (at 5% )and the Bank of Korea(4%) round out the top four.

- Of the others, only Switzerland and Singapore have amounts outstanding greater than $10bn.

Maturing Amounts

A total of $114bn matures on 11th June (25% of the total) and a further $110bn matures on 18th June (another 25% of the total):

- In fact, $295bn of the $439bn outstanding of longer-term swaps matures within the month of June.

- That is 67% of the total maturing within 3 weeks.

- Whilst it is split between different central banks, the ECB operations around June 11th will be closely watched, whilst the BoJ operations around June 18th will move into greater focus.

Will the USD amounts be rolled over? Is the demand for dollars from central banks still there? Will banks want to roll these amounts in private markets, or will they continue to access the central bank facilities?

Market Pricing

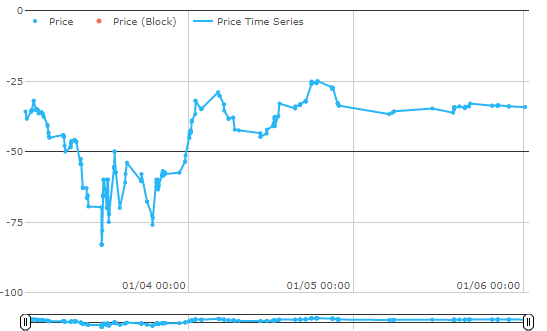

Using SDRView Pro to look at prices of 1y USD-JPY cross currency basis is instructive here:

Showing;

- With Asia by far the largest users of these swaps, USDJPY will likely be the centre of any price action as a result of maturing (and rolling?) USD amounts.

- Looking at the short-end of the curve, 1Y USDJPY cross currency basis has traded in a range of -83 basis points up to -25 basis points since 1st March.

- That -83 print was recorded on 16th March, marking the nadir of the stresses before the Fed facilities really opened their taps (and reduced their pricing to OIS + 25 basis points from +50 previously).

- Volatility is noticeably lower in recent times.

- However, that hasn’t stopped the basis retreating from the -25 high to now be back at -34 basis points.

The key question is how much of the $295bn was actually put to work in the markets, and how much was simply drawn as a hedge/back-stop?

Use of the Facilities

The BIS published a great article looking at the use of these facilities:

Two key take-aways from this BIS research are:

The rapid take-up of central bank dollar liquidity facilities reflected the stigma-free access, as banks did not have to worry about any possible negative signalling from tapping central bank liquidity.

BIS Bulletin No.15

And;

Some market participants report taking advantage of the positive LIBOR basis by borrowing euros unsecured, swapping them into US dollars and lending at rates close to USD LIBOR. Such “arbitrage” would lead to upward pressure on EURIBOR and downward pressure on dollar LIBOR, which indeed was the case in the later stages of this episode.

BIS Bulletin No.15

A stigma free emergency facility, that market participants were even willing to arbitrage to make profit? That will, for sure, ensure smooth monetary policy transmission!

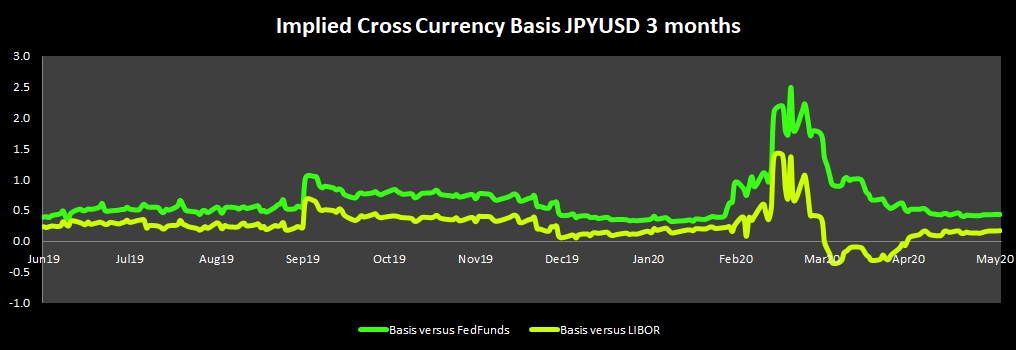

It is fairly reasonable, therefore, to expect the amounts at the 84-day operations maturing this month to be rolled. However, we need to bear in mind the market pricing. The motivation to access stigma free USD funds and lend them out in the private markets to make “profit” was unusually high back in March. The basis has narrowed considerably:

Showing;

- Back in March, implied yields in USD were up to 200 basis points over Fed Funds from the FX markets. It was exceptionally expensive to raise USD via FX swaps.

- Compare this with the Fed Funds + 25 basis point level offered by the central banks. There was a huge motivation to raise funds!

- With implied yields in USD now back to Fed Funds plus 44 basis points, the motivation is drastically lower.

There is no sign that these facilities will be removed any time soon, and they still offer the cheapest possible access to USD funds (in USDJPY). Banks should be motivated to take advantage but is the pricing differential enough?

We’ll find out during June.