- Our analysis shows that more blocks transacted than ever before in March 2020.

- More volume traded as a block on-SEF in March.

- There is no difference in Price Dispersion between block and non-block trades during both normal and stressed market conditions.

- The current 15 minute delay in reporting for block trades has no negative impact on liquidity and does not cause any hedging problems.

- The data therefore suggests that a 48 hour reporting delay for these trades is unnecessary.

The CFTC issued a Proposed Rule back in February entitled “Amendments to the Real-Time Public Reporting Requirements“.

This proposed rule, along with some necessary changes, is asking the market whether it is a good idea to extend the block reporting delay from the current ~15 minutes to 48 hours. Forty-eight hours!

That is quite some change.

Volatile Markets

Since it was issued, we have had an almighty test of market structure, through which our OTC derivatives markets have managed to scale and continue trading in an admirable manner.

I have argued in a previous blog that Transparency Helped Markets Function. So with the closing date of this CFTC consultation extended to 20th May, I thought I would take the opportunity to put some analysis on the performance of block trades during March 2020 out there to help our readers respond to the consultation.

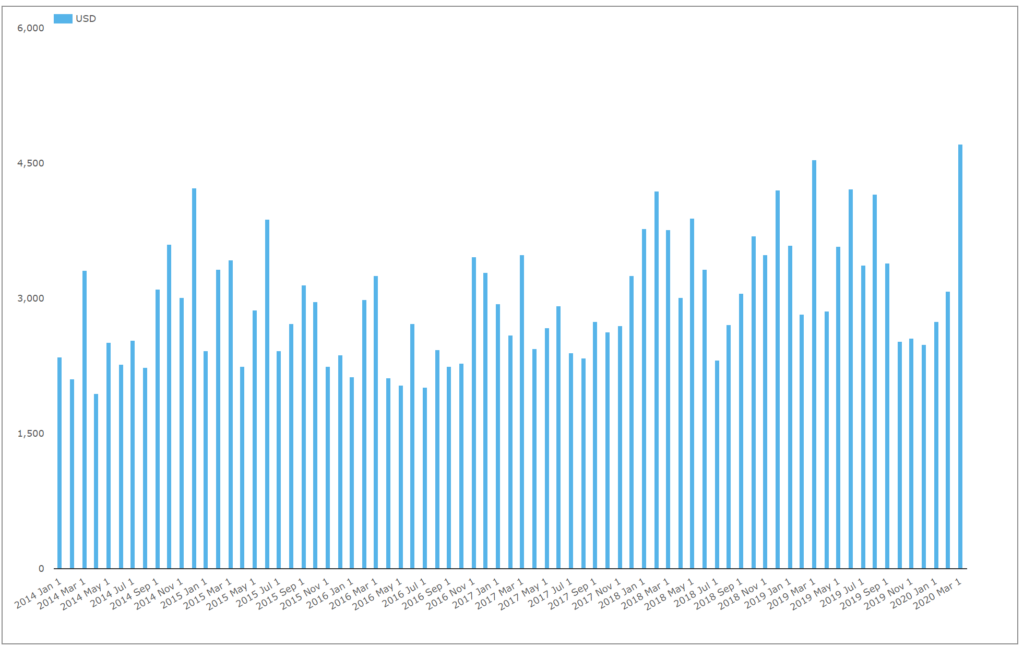

More Blocks Traded in March 2020 Than Ever Before

In March 2020, 4,719 “capped notional” transactions were reported to US SDRs for USD Fixed-Float Swaps:

Showing;

- March 2020 saw an increase in the number of “capped notional” trades reported of nearly 4% compared to the previous record month, March 2019.

- This is surely a good sign for how large amounts of risk can be transacted, even during stressed market conditions.

- It is, however, important to note that the number of capped notional trades transacted each month has generally increased in USD Swaps since reporting began. This is not just a facet of extremely volatile markets causing huge demand for large trades.

A quick note on this blog. I will use “capped notional” and “block” trades interchangeably from here on to make it more readable/accessible to a wider audience. Please note that they are not the same thing, however I believe that the proposed change to a 48-hour delay would apply to both. Original background on capped notional versus block trades can be found in my blog Identifying Customer Block Trades in the SDR Data (with particular reference to “NARL 14-118”).

Most of the trades above are also designated “block” (3,633 are block out of the 4,719 total capped notional transactions). Due to NARL 14-118 we therefore know that these trades were transacted on RFQ platforms, typically Tradeweb or BBG SEF. Unfortunately, we’ve never got to the bottom of whether these are systematically reported as being executed ON- or OFF-SEF.

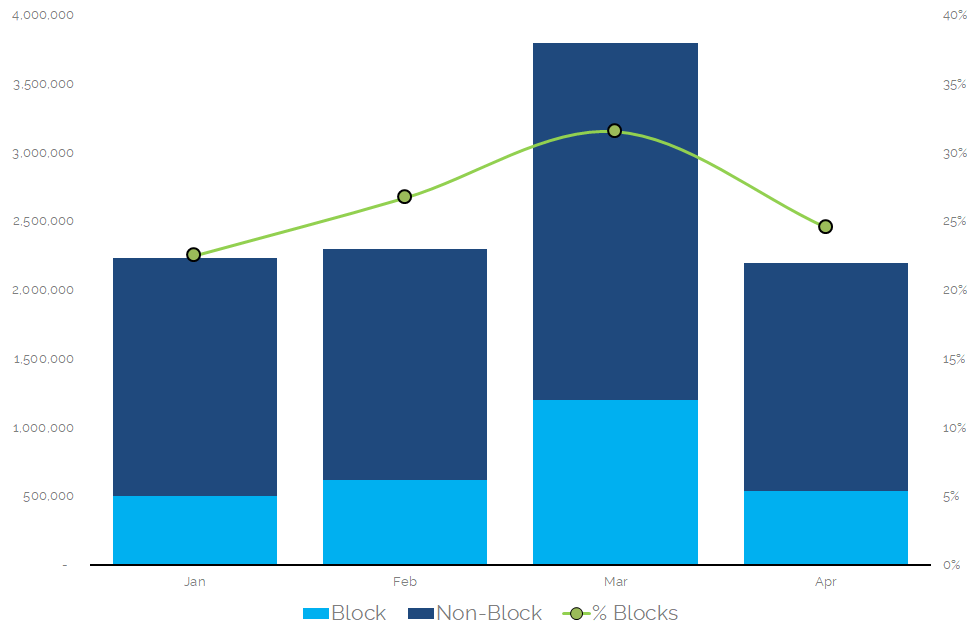

More Volume Traded as a Block on-SEF

SEFs report their total volumes on a T+1 basis. They are also obliged to report how much of this volume was executed as a block. On the D2C platforms (BBG and Tradeweb), we saw more block volumes trade in March 2020 than the rest of 2020:

Showing;

- Notional volumes of USD IRS executed on-SEF in 2020.

- In March, 32% of total volume was executed as a block trade across just two platforms – Tradeweb and BBG.

- Both of these are RFQ D2C SEF platforms.

Interestingly, this block trading volume is reported on a T+1 basis, thanks to “CFTC Part 16” data. I do not see any changes proposed as part of the latest rule-making to this Part 16 data.

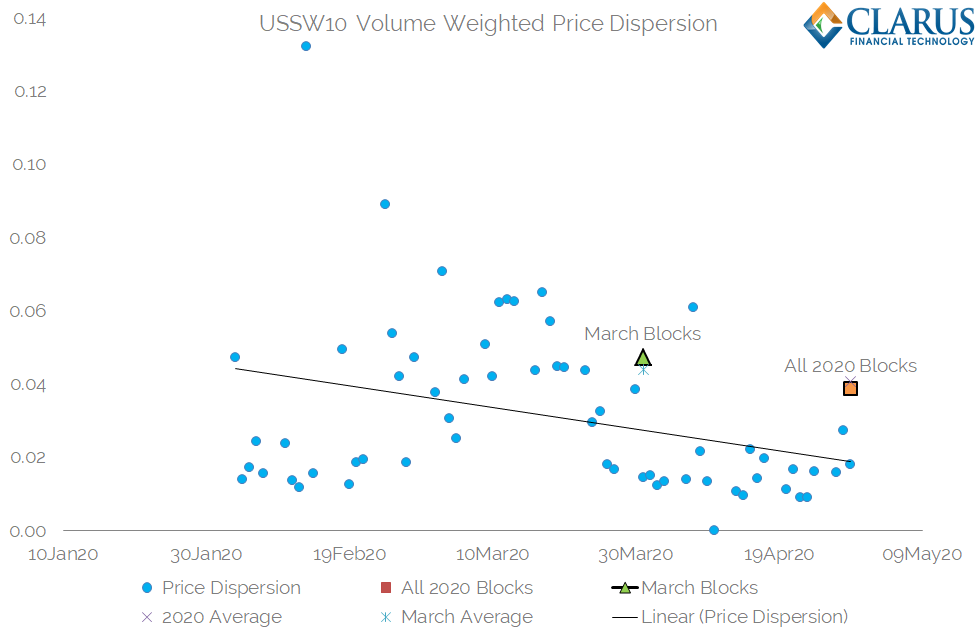

Price Dispersion is the Same for Blocks and non-Block Trades

Following up on our work on liquidity, we are able to calculate Price Dispersion measures for both Block and non-Block trades. This allows us to systematically assess whether block trades are more or less liquid than non-blocks. It also allows us to assess their prices relative to other recently transacted trades, and look at whether block trades actually “move markets”.

From the statistical evidence in 2020, we see that Block Trades have the same Price Dispersion as non-Block Trades:

Showing;

- Daily Price Dispersion for 10 year spot-starting USD IRS executed on-SEF during 2020.

- The average Price Dispersion for all trades during 2020 was 0.041 basis points.

- The average Price Dispersion for Block and Capped Notional Trades in 2020 was 0.039 basis points.

- Similarly, for March 2020 alone, the Price Dispersion for all trades was 0.044 basis points.

- The average Price Dispersion for Block trades in March 2020 was 0.047 basis points.

A quick aside to explain the exact Price Dispersion methodology used to measure liquidity conditions by Clarus:

\( \tag {1} DispVW_{i,t} = \sqrt{\sum\limits_{k=1}^{N_{i,t}}\frac{Vlm_{k,i,t}}{Vlm_{i,t}}(\frac {P_{k,i,t}-\bar{P_{i,t}}}{\bar{P_{i,t}}})^2}\)

where;

\(N_{i,t}\) is the total number of trades executed for contract i on day t, e.g. how many 10y trades occurred on the 23rd March 2020?

\(P_{k,i,t}\) is the execution price of transaction k, i.e. the price of a particular 10y trade on the 23rd March.

\( \bar{P_{i,t}}\) is the average execution price on contract i and day t, e.g. what was the average price of all 10y trades done on 23rd March.

\( Vlm_{k,i,t}\) is the volume of transaction k; e.g. the size of the 10 year trade we are looking at on 23rd March and;

\(Vlm_{i,t}=\sum_{k}Vlm_{k,i,t}\) is the total volume for contract i on day t. e.g. the total volume of 10 year swaps traded on the 23rd March.

In Summary

The current block regime, with volumes disclosed up to the reporting threshold either in close to real time (as for capped notional) or with a 15 minute delay (for Block trades) does not appear to have any effect on the liquidity of block trades.

The lack of Price Dispersion around these Block trades also suggests that hedging these trades within the current transparency regime is not causing anyone any problems.