- In times of stress, CCPs may issue intraday margin calls that can cause liquidity strains in the market.

- A new CPMI paper, “Streamling variation margin in centrally cleared markets” looks at the issues around these intraday margin calls.

- The paper proposes some best practices for CCPs.

- We highlight how Clarus CHARM helps deal with liquidity demands across CCPs.

- Pragmatic solutions include increasing the predictability and transparency over intraday margin calls.

- A longer term solution is to closely replicate end of day settlement runs with intraday timing.

No one wants to be called in default by a CCP during stressed markets as a result of operational complexity/failures – much as ICE & Citi stated regarding March 2020:

So today I follow up on our Clarus blogs (and podcast!) regarding members requirements at CCPs. For example, you can take a look at the International Default Simulation organised by CCP Global, as well as studying Variation Margin in a Crisis and our Quick Take Default Simulation Exercises by CCPs. These pieces of work follow on from a 2019 paper from the CPMI on “Central Counterparty Default Management Auctions“.

This latest paper from the Basel Committee on Payments and Market Infrastructures (CPMI) proposes 8 best practices for CCPs when issuing, managing and processing Variation Margin calls. (For new readers, Variation Margin is called as a result of daily market moves changing the current valuation of a cleared portfolio. Initial Margin calls are related to the potential future exposure of the portfolio and are not discussed here).

Intraday Liquidity

Surprisingly for a paper of this nature, there is not a lengthy introduction that highlights all of the good things that CCPs do for Variation Margin. So I will give you a summary for their end of day runs:

- CCPs multilaterally net payment obligations across all of your counterparties, reducing counterparty credit risk.

- They process all currency obligations in a single settlement cycle, removing herstatt risk and processing all settlements on a payment vs payment basis.

- They remove disputes from settlement obligations, providing third-party valuation and reconciliation of all cleared portfolios.

The CPMI proposals highlight how each of the benefits above can break-down when CCPs call VM intraday. These are largely due to events/processes outside of a CCP’s control, and are not necessarily relevant if we only had a single CCP covering all markets. However, when you get more than 30 CCPs (I count 32 in CCPView) all issuing intraday VM, the interplay and complexity likely leads to an “unnecessary” overall liquidity drain in the market.

So let’s go through the best practices proposed by the CPMI.

Increase Predictability

The CPMI paper looks at CCP practices for intraday Variation Margin – can they do it, when do they do it, how frequently, and is it scheduled or ad hoc?

You can imagine how details like this slip through the cracks when a bank is a Clearing Member across multiple CCPs. Do intraday calls (“ITD” in the paper) fall into a Must, Could or Should when prioritising go-live? Are they “BAU” events even though they do not happen very often? How do you build to consume ad-hoc calls? How do resource constrained businesses ensure they have enough headroom to deal with 30+ CCPs all making intraday margin calls on the same day?

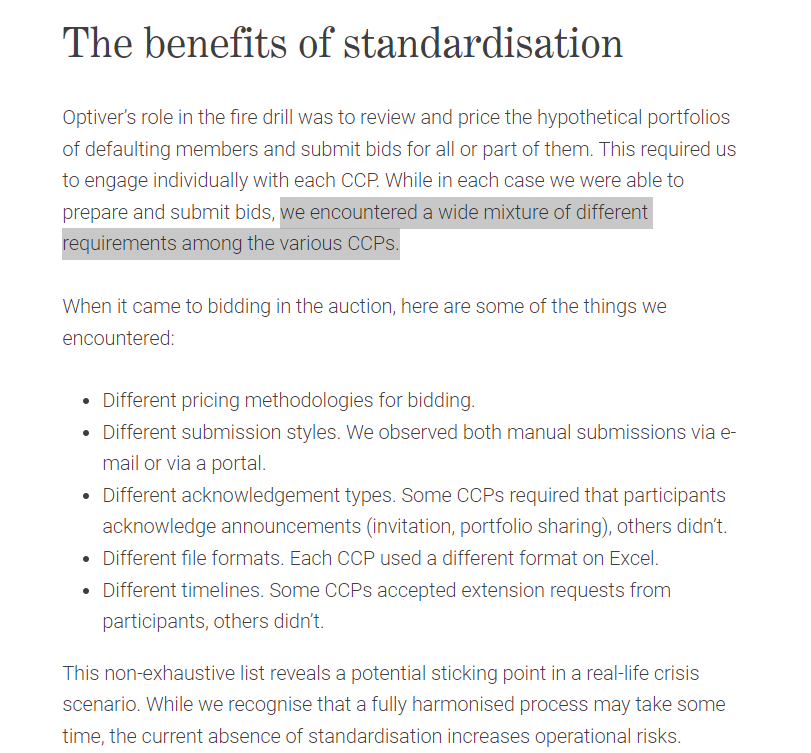

The paper doesn’t talk too much about “survivors curse” (aggressive & early intraday calls exacerbating market moves), so I think this is more to do with the operational backbone – how can it be simplified and standardised. As Optiver said in their blog regarding global Firedrills (CIDS):

Clarus clients appreciate that our Firedrill tool already standardises the bidding process for Swaps portfolios. In response to the CPMI paper, we also highlight that Clarus CHARM:

- Monitors intraday requirements from CCPs, (using intraday market data from CCPs and sourced independently).

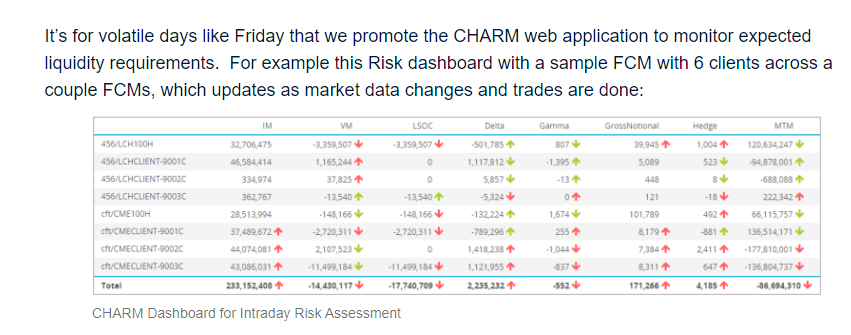

- Runs portfolio analytics to predict liquidity requirements and help size suitable liquidity buffers:

In another US Election year it is important to have access to the right tools to manage event risks.

Time

The paper states that there is little consistency across CCPs regarding notice periods for the settlement of intraday margin calls. An intraday call will have to be settled anywhere from 10 to 150 minutes, depending on the CCP. We will just point out that time is likely the most valuable commodity during a crisis, so anything CCPs can do to make life easier/less stressful for their Clearing Members should be adopted.

Offsetting and Netting

The paper suggest that most CCPs are doing the maximum amount of netting already. This includes within products (coupons vs VM), across house and client accounts (where allowed) and IM vs VM. However, the paper highlights that;

- Clients do not pay ITD VM – which will create a huge liquidity drain on clearing members as clients tend to have the most directional positions.

- CCPs could also be returning excess VM intraday, not just making calls.

- The give-up/allocation process for clearing can affect VM calculations – effectively stating that this needs to be more efficient so that ITD calculations are not done in the middle of a give-up process.

VM Pass Through

It is recommended that, where possible, Variation Margin from out-of-the-money members is directly passed through to in-the-money members intraday. This sounds obvious, but may not be possible in practice:

- If a portfolio is multi-currency, intraday VM may only be called in a single currency. That amount is then returned and the individual currencies collected at the next EOD settlement run.

- This is because members and CCPs cannot settle 20+ currencies 24 hours a day and at short (10 minutes?!) notice.

- It should not be the job of CCPs to translate a net VM currency for one Clearing Member (e.g. GBP) into a different net VM currency (e.g. USD) for another Clearing Member.

- This sounds like a particularly tricky one to solve without a multi-currency, multi-session settlement session intraday.

- Effectively, redesigning CLS for FX for multiple currency VM calls each day. A huge undertaking.

Allow excess collateral to offset VM

This suggestion seems obvious – anything that a member has already deposited with the CCP over and above its previous IM and VM settlement obligations should be used to net against any intraday VM calls. However, it is often not that straight-forward as the “excess” will likely not be in cash, and may be in the wrong currency. It is again putting an element of liquidity risk onto CCPs in stressed markets – a trade-off that market participants are typically uncomfortable with because the risk is mutualised.

Transparency

Many of the proposed practices suggest that there is a bit of a divide between CCPs saying “it is obvious when we will make intraday calls” to Clearing members and clients saying “we don’t know when the calls will be, what they will be and how to reconcile the calls”. Again, this all speaks to increasing standardisation – it is maybe unrealistic to expect Clearing members to continually monitor changing thresholds, timing and notice periods across 30 or more CCPs.

In Summary

The paper strikes a good balance between:

- Pragmatic Solutions: CCPs need to make it 100% clear when and how intraday calls will be made.

- Long Term Solutions: We need global settlement cycles across all currencies every two hours to completely remove the chance of excess liquidity drain in times of crisis.

The comments are now open for everyone to suggest blockchain as the solution to all these problems. In the meantime, we highlight how Clarus CHARM monitors and predicts these liquidity needs.