- Active Accounts at EU-based CCPs will be required for EU counterparties subject to the clearing obligation.

- An Active Account must regularly clear five trades, posting initial and daily variation margin.

- These measures will be reviewed in a couple of years.

The Clarus blog covered Active Accounts back in December, and followed up with probably the first podcast in the world to cover Active Accounts:

The European Parliament have followed this with an announcement this month that:

- At least one active account at a CCP established in the EU will be necessary.

- This covers both financial and non-financial counterparties subject to the clearing obligation.

- The active account must regularly clear five trades in each of the subcategories of derivatives.

- The account is “active” if it posts initial and daily variation margin (and can be scaled up).

- Further measures can be enacted if necessary in several years (the quoted politician actually states two years).

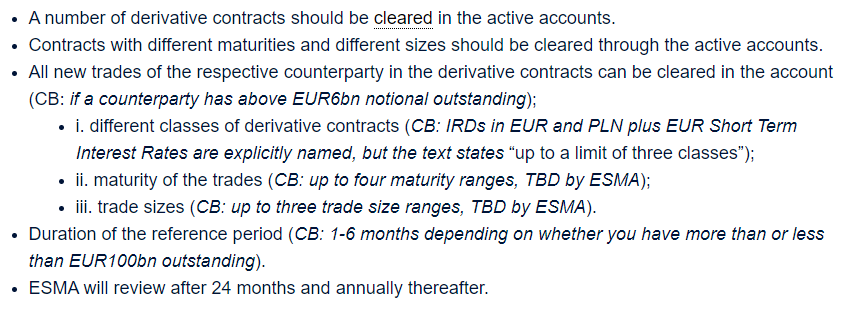

The European Commission then provided the following details:

- ESMA should identify up to three derivative classes (interest rate derivatives in EUR & PLN, STIRs in EUR so far).

- ESMA will then identify up to five subcategories per derivative class, based on size and maturity.

- Five trades per annum should be cleared.

- There will be a scaled-down representativeness requirement for some counterparties (e.g. EU pension funds) to clear only one trade per annum (within each derivative class).

- ESMA will have to report two years after the active account requirement goes live as to the effects of these new rules.

For those of us who thrive on the details this looks to be almost exactly the same as I wrote back in December:

My understanding from reading the texts is that the calibration period will be annual (irrespective of size), but the FT suggests it could be monthly, resulting in 900 trades a year for the very largest derivatives users.

Either way, the commentary is aligned that this is a “scaled-back” plan compared to earlier proposals.

If you are interested in the politics…

I tend to focus on the details rather than the politics, but our readers will also be interested in some of the back-stories circulating. Politico states that as recently as September, ECB staff were lobbying for 30-40% of trades to be moved to the EU for European banks. Apparently, French banks pushed back hard against this, and the French government sided with their banks and against Germany – it is interesting reading at least!

Path Forward

As per the FT (with the aid of data from Clarus CCPView), London dominates euro derivatives clearing:

The latest announcements will likely move Clearing to where it belongs – away from the front pages, away from political intrigue and back into the depths of financial market plumbing. If you read another article about Clearing in the mainstream press it is likely only because something has gone wrong!

European Market Share

This story will now move away from politics and back toward the data. I will continue to monitor market shares across OTC EUR Swaps, EURIBOR futures contracts traded at ICE and Eurex and ESTR liquidity across CME, Eurex and ICE. I only updated the data three weeks ago, so readers will have to wait until the end of the quarter to see an updated STIR dashboard on the blog. Our data clients can of course monitor the data daily.