(Sorry/not sorry for the title)

UK Rates

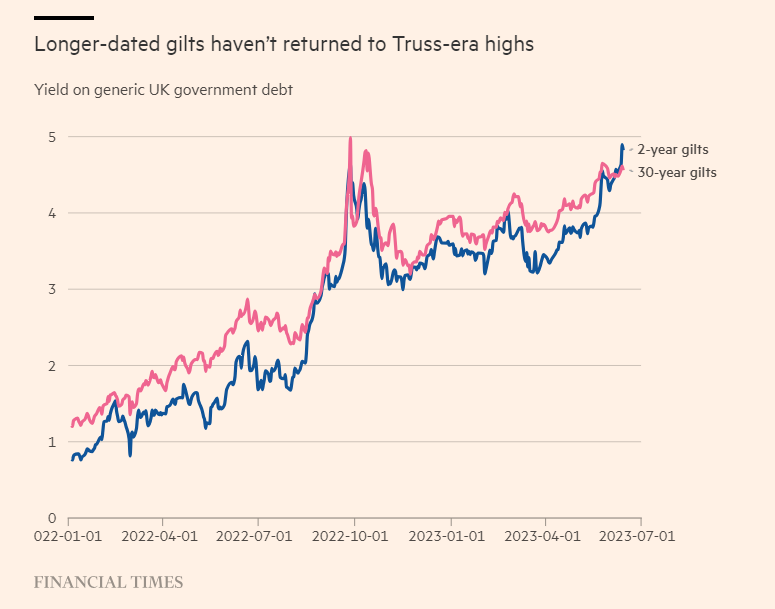

UK rates markets have been interesting ever since the autumn meltdown, and there are now lots of headlines around as yields break the highs last reached in those tumultuous trading days:

The FT Alphaville overview of why June 2023 is not September 2022 is well worth a read –> No, current gilt yields don’t vindicate Liz Truss, please don’t make us explain this again.

When Liz Truss was in office, we were more thankful than ever for transparency in derivatives markets, even if the outsized market moves led to higher swap margins and even a first off-cycle recalibration of margin models.

It was with bated anticipation that I went to check out GBP Swap volumes across our data products in 2023….

Before we get to the data I should first insert a big <<here be a Health Warning>> to our readers. Anyone who subscribes to the “Matt Levine Effect” (full academic paper here!) should note that the last time I flippantly published a “GBP Swaps Review” it took just two weeks before the UK financial markets went absolutely crazy.

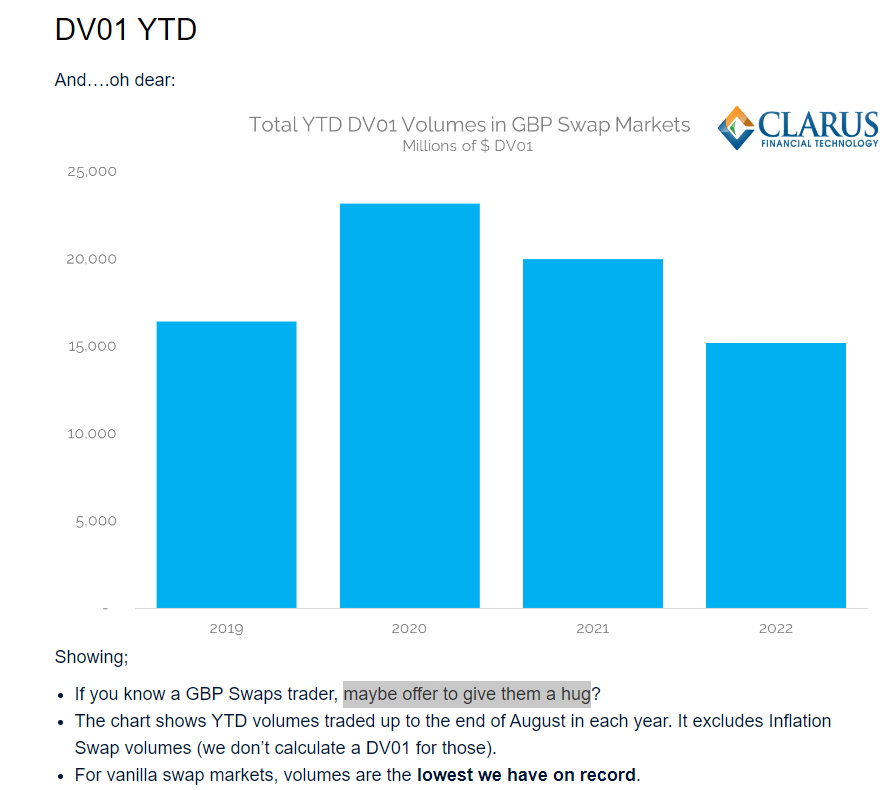

That blog told us that 2022 was a terrible year for GBP Swaps market volumes before September. I even suggested giving your GBP swaps traders a hug!

Read on to see how 2023 is doing so far….

GBP Swap Volumes

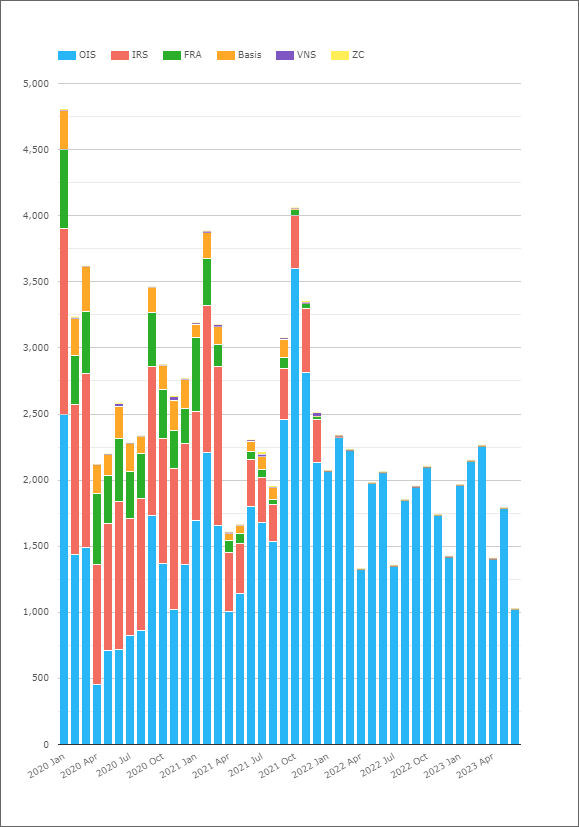

First up, from CCPView we have global swap market volumes for GBP swaps:

Showing;

- DV01 volumes of OTC cleared derivatives in GBP.

- (We show DV01 as the craziness in Q4 last year resulted in a lot of long-end trading, therefore large DV01s but relatively small notionals).

- As we looked at last year, there are fewer products trading in GBP Rates than ever before. This is a SONIA-only market post LIBOR cessation.

- DV01 traded in February and March 2023 was broadly comparable with the same months in 2022, and above the crisis-hit months of Q4 2022.

Lots of activity is currently centred around the short-end amid adjustments over expectations as to how high terminal rates might reach. This has resulted in more short-dated activity in 2023 than other years, with 46% of risk traded in tenors 2Y and shorter:

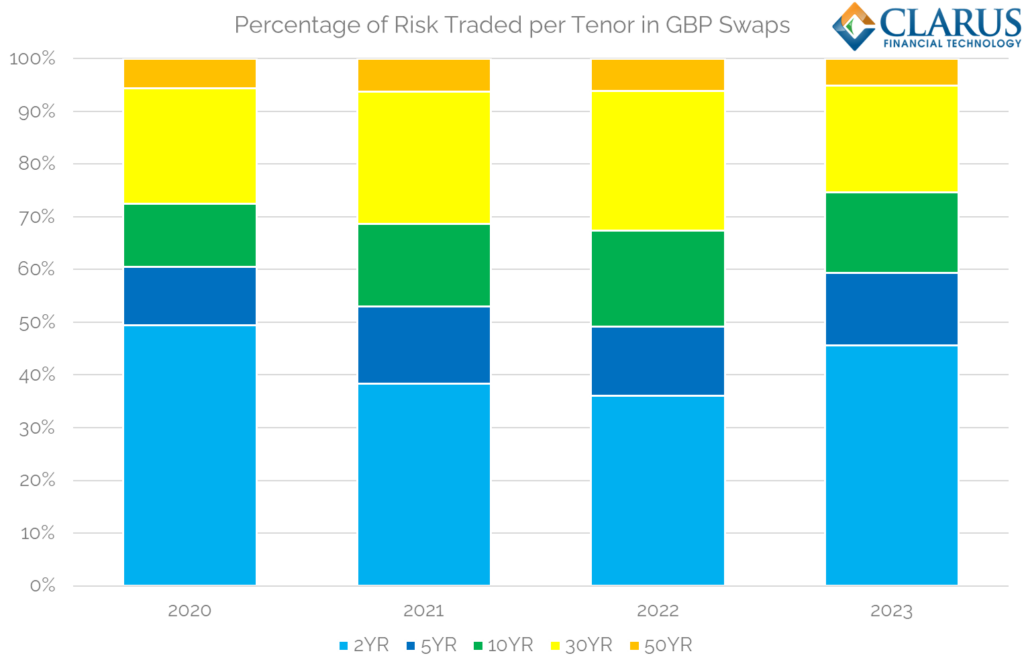

Showing;

- DV01 per tenor traded in the past 3 and a half years in GBP swaps.

- In 2020, as short-end rates plummeted due to the pandemic, 50% of DV01 was traded in the short-end.

- This reverted to 35-40% in 2021 and 2022.

- Even as policy began to “normalise” in 2022, there was less short-end risk traded in 2022 than 2021.

- In 2023, we have so far seen 46% of risk traded in the short-end, a clear increase on previous years.

So Should You Be Hugging Your Swaps Traders?

Probably, yes.

The market reaction to “Trussonomics” last year was larger than expected, and not just because of the LDI-margin-leverage dynamic. As we said at the time, liquidity was plumbing new depths in GBP swap markets. And now, in 2023 we find that:

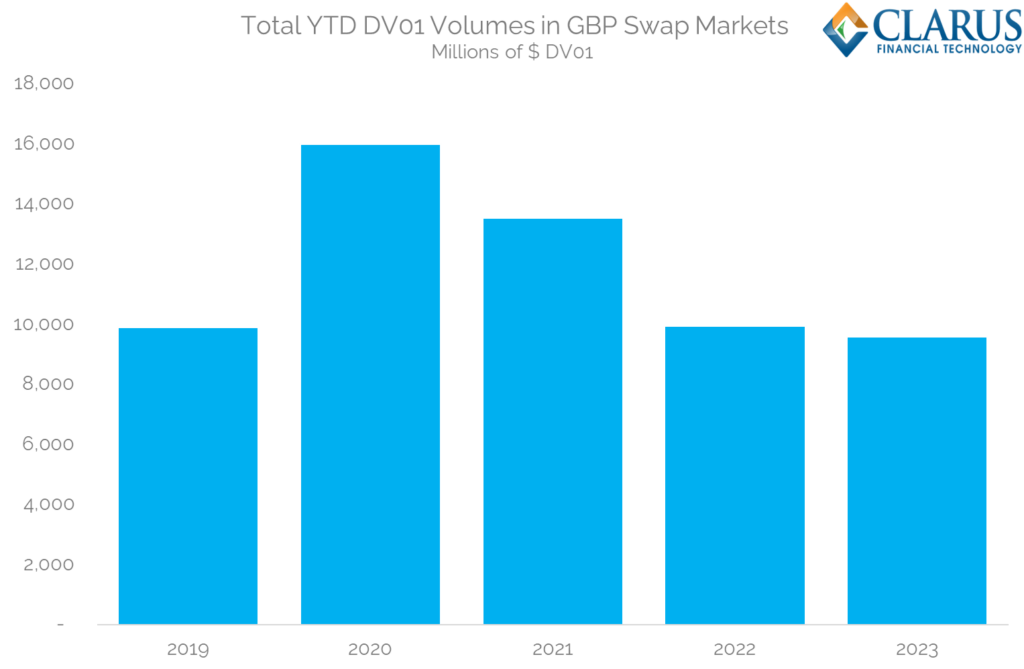

- Year to Date risk in GBP swaps is at all-time lows, for at least the past 5 years.

- The amount of DV01 traded so far this year in GBP OTC cleared derivatives is therefore even lower than in 2022, which itself was lower than any year since 2019.

- It doesn’t look great, does it?

We’ve had plenty of volatility, and plenty of reasons to trade GBP rates this year. And yet it is not coming through in the volumes. Last year, just before the market blew up, I wrote about the decline in GBP volumes:

What is this down to?

It is hard to put a finger on why volumes are reducing in GBP Rates markets. Is it due to:

- LIBOR cessation reducing the number of products to trade?

- Market conditions being less favourable?

- The UK behaving like a banana-republic, increasing volatility/political risk and so lowering “risk appetite” in terms of DV01/notional at risk?

Now in 2023, I am still no closer to working out which of those reasons is the biggest contributor.

One Market Not Suffering…

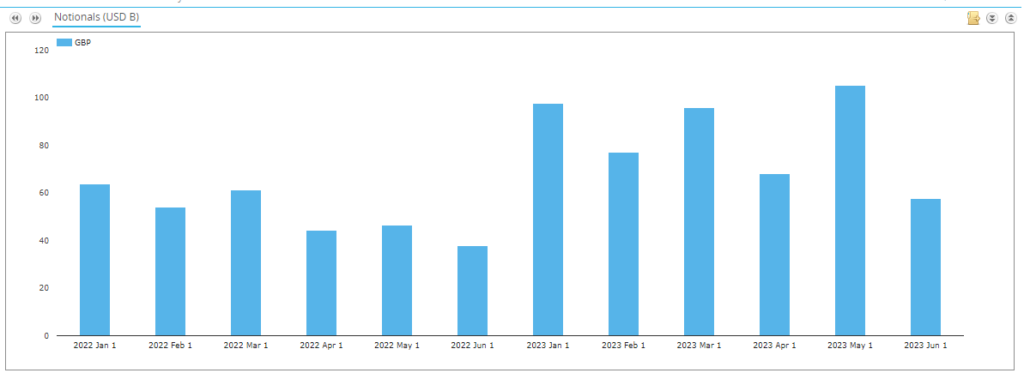

…..(for once) is Cable Cross Currency. I examined volumes to see if maybe cross-border issuance/flows had shrunk for the UK. This would suggest less bond issuance flows for GBP swaps traders to manage. But no, the Cable market is alive and kicking, recording much higher notional volumes this year than the same period in 2022:

Notional amounts traded in 2023 are so far 60% higher than during the same period in 2022. DV01s are only 23% higher, suggesting that a lot of this has been shorter dated activity.

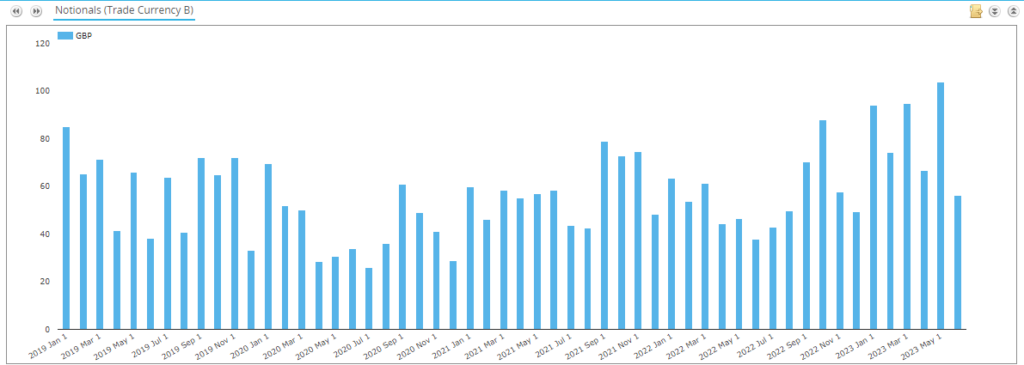

Longer-term volume charts show that May 2023 was an all-time record for GBPUSD XCCY Swaps reported to SDRs for notional traded:

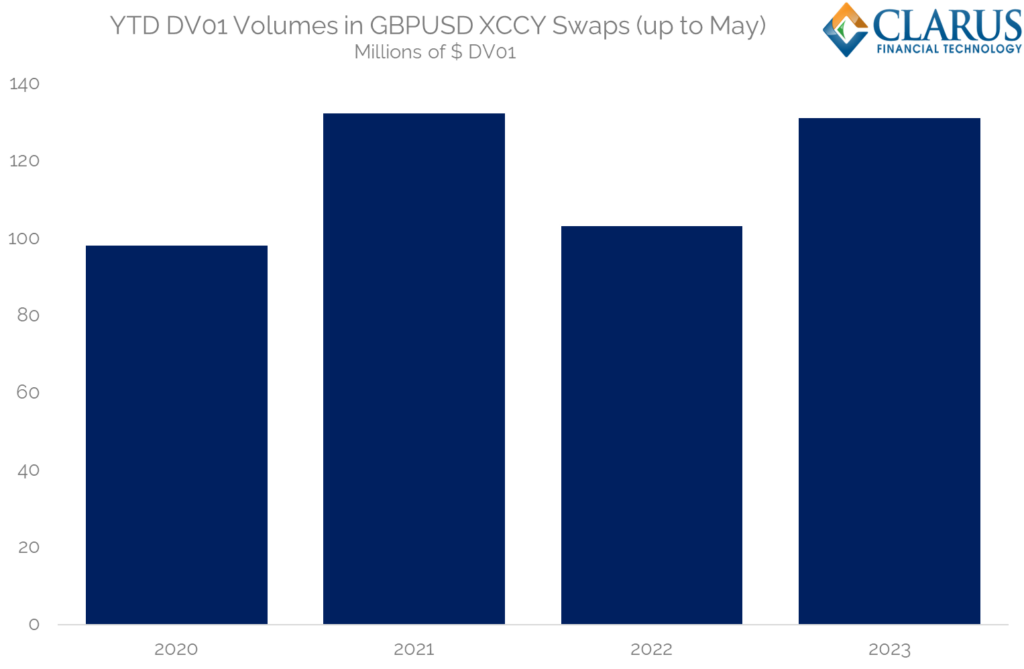

And that total YTD DV01 activity in Cable has matched 2021:

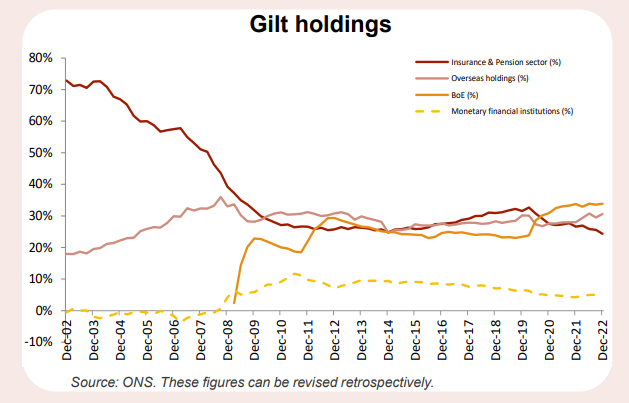

Fortunately, we (probably) shouldn’t worry that all of this XCCY activity is linked to foreign investors fleeing the Gilt market (and hence no longer wanting to hedge their GBP Rates risk). The DMO report that overseas holdings of Gilts have stayed pretty constant (and besides, most of these foreign holdings are not held as XCCY asset swaps, as investors like both the FX and Rates exposure):

In Summary

- If you see a GBP Swaps Trader looking a bit glum, you now know why.

- It’s not been a great year for volumes in GBP swaps, with YTD volumes even worse than in 2022.

- A bright spot lies in Cross Currency swapped volumes, where GBPUSD YTD volumes are impressively higher than last year.